The Power of Dividend Investing for Beginners: Build Passive Income (2026)

Last updated: January 2026

Imagine opening your brokerage app and seeing this: “$127.43 deposited – Quarterly Dividend Payment.” You didn’t work for it. You didn’t trade anything. You simply owned shares of companies, and they paid you for being a shareholder.

That’s dividend investing—one of the most powerful wealth-building strategies available, yet surprisingly misunderstood by most beginners. While everyone chases stock price appreciation, dividend investors quietly build streams of passive income that grow year after year, eventually creating financial freedom.

Dividend investing isn’t about getting rich overnight. It’s about building a portfolio of quality companies that pay you regularly, reinvesting those payments to buy more shares, and watching the snowball effect of compound interest turn modest investments into substantial income streams over decades.

The best part? You don’t need to be wealthy to start. With as little as $100, you can begin building a dividend portfolio today that could pay you thousands—even tens of thousands—of dollars annually in the future.

In this guide, you’ll learn exactly what dividend investing is, why it’s so powerful, how to calculate dividend yields, which dividend stocks and ETFs are best for beginners, how to build a dividend portfolio from scratch, and the critical mistakes that destroy dividend strategies. By the end, you’ll have a complete roadmap to start generating passive income through dividends.

Let’s unlock the power of getting paid to own stocks.

What Are Dividends? (Clear Definition)

A dividend is a cash payment that a company distributes to its shareholders from its profits, typically paid quarterly (every 3 months), as a reward for owning the company’s stock.

In simple terms: When you own shares of a dividend-paying company, they send you money regularly just for being a shareholder.

How Dividends Work

The Process:

- You buy shares of a dividend-paying company

- Example: Buy 100 shares of Company XYZ

- Company earns profits

- They make money from their business

- Board decides to share profits with shareholders

- They declare a dividend payment

- You receive cash payment

- Money appears in your brokerage account

- Usually quarterly (4 times per year)

- You can spend it or reinvest it

- Take the cash or buy more shares

Real Example

You own 100 shares of Coca-Cola:

- Coca-Cola pays $0.46 per share quarterly

- You own 100 shares

- You receive: $46 every quarter

- Annual income: $184 just for owning the stock

You didn’t sell anything. You still own your 100 shares. But you got paid $184 for holding them.

That’s dividend income.

Key Dividend Terms

Dividend Per Share: Amount paid per share you own

- Example: $0.50 per share

Dividend Yield: Annual dividend divided by stock price (as percentage)

- Example: $2 annual dividend ÷ $50 stock price = 4% yield

Ex-Dividend Date: Date you must own stock by to receive upcoming dividend

- Buy before this date = you get the dividend

- Buy after = you don’t

Payment Date: When dividend money actually hits your account

Dividend Frequency: How often paid

- Most common: Quarterly (4x/year)

- Some: Monthly, semi-annually, annually

Why Dividend Investing is Powerful for Wealth Building

Dividend investing offers unique advantages that other strategies don’t:

1. Passive Income That Grows Over Time

Unlike wages, dividend income requires no additional work:

Salary:

- Stop working = income stops

- To increase income = work more hours or get raise

Dividends:

- Stop working = dividends continue

- Income grows as companies increase dividends and you buy more shares

- Completely passive

Example:

- Year 1: $500 in annual dividends

- Year 5: $1,200 (companies raised dividends + you bought more shares)

- Year 10: $3,000

- Year 20: $10,000+

- All passive. All growing.

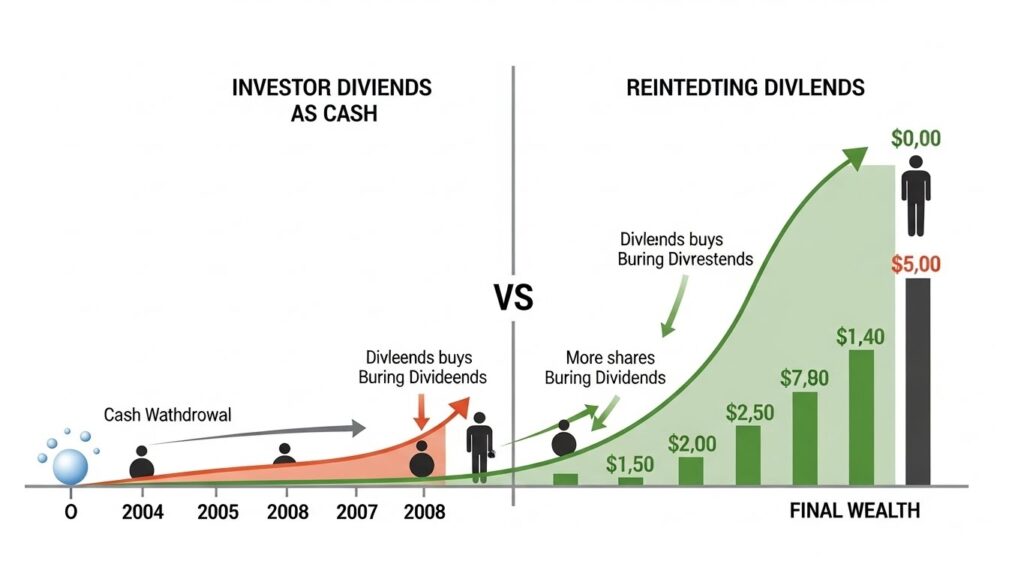

2. Compound Growth Through Reinvestment

The snowball effect:

Without reinvestment:

- Invest $10,000 at 4% yield

- Receive $400/year

- After 20 years: Still receive $400/year (assuming no dividend growth)

With reinvestment (DRIP):

- Invest $10,000 at 4% yield

- Reinvest all dividends to buy more shares

- Each new share pays more dividends

- After 20 years with 5% dividend growth: Receiving $2,000+/year

- Portfolio value: $35,000+

The difference: $1,600/year in passive income!

3. Forced Discipline and Reduced Emotional Decisions

Dividends keep you invested:

Scenario: Market crashes 30%

Growth stock investor:

- Sees portfolio drop from $50,000 to $35,000

- Panics: “I’m losing money!”

- Tempted to sell at bottom

Dividend investor:

- Sees portfolio drop from $50,000 to $35,000

- Checks dividends: Still receiving $2,000/year

- Thinks: “My income didn’t change. Actually, dividends now buy more shares at lower prices!”

- Stays invested

Dividends provide psychological comfort during volatility.

4. Historical Outperformance

Data shows:

- S&P 500 dividend-paying stocks have historically outperformed non-dividend payers

- Dividend growth stocks tend to be higher quality, more stable companies

- Companies that consistently raise dividends (“Dividend Aristocrats”) beat the market long-term

Reason: Companies that pay dividends are typically:

- Profitable (can’t fake profits when paying cash)

- Mature and stable

- Well-managed (disciplined capital allocation)

5. Income During Retirement Without Selling

The traditional retirement approach:

- Save $1 million

- Withdraw 4% annually ($40,000)

- Gradually deplete principal over 30 years

Dividend approach:

- Build portfolio yielding 4-5%

- $1 million portfolio = $40,000-50,000/year in dividends

- Never sell shares, never deplete principal

- Pass remaining portfolio to heirs

Dividends provide income without liquidating your wealth.

6. Tax Advantages (Qualified Dividends)

In the U.S.:

- Most dividends are “qualified dividends”

- Taxed at capital gains rates (0%, 15%, or 20%)

- Often lower than ordinary income tax rates (10-37%)

This means more money stays in your pocket compared to regular income.

Understanding Dividend Yield and What It Means

Dividend yield is the most important metric in dividend investing. Here’s how to understand it:

The Formula

Dividend Yield = (Annual Dividend Per Share ÷ Current Stock Price) × 100

Example:

- Stock price: $100

- Annual dividend: $4 per share

- Yield: ($4 ÷ $100) × 100 = 4%

This means: For every $100 invested, you receive $4 annually in dividends.

What Different Yields Mean

0-2% Yield (Low):

- Examples: Growth tech stocks, Amazon, Tesla

- Meaning: Company prioritizes growth over dividends

- Good for: Capital appreciation, not income

2-4% Yield (Moderate):

- Examples: Many blue-chip stocks, diversified dividend ETFs

- Meaning: Balanced approach—some growth, steady income

- Good for: Most dividend investors, core holdings

4-6% Yield (High):

- Examples: Utilities, REITs, some mature companies

- Meaning: Focus on income, slower growth

- Good for: Income-focused investors, retirees

6%+ Yield (Very High):

- Warning: Often too good to be true

- Risks: Dividend cut likely, struggling business, unsustainable payout

- Exceptions: Some REITs, MLPs legitimately yield 6-8%

The Dividend Trap

High yield doesn’t always mean good investment:

Scenario 1: Healthy 4% Yield

- Stock price: $100

- Dividend: $4/year

- Company profitable, dividend sustainable

Scenario 2: Dangerous 10% Yield

- Stock WAS $100, now $40 (dropped 60%)

- Dividend still $4/year (for now)

- Yield: $4 ÷ $40 = 10%

- But dividend likely to be cut soon

- High yield due to falling stock price = TRAP

Rule: Don’t chase yields above 6-7% without deep research.

Dividend Growth Matters More Than Current Yield

Would you rather:

Option A: 6% yield, 0% growth

- Start: $10,000 investment = $600/year income

- Year 10: Still $600/year income

- Total 10-year income: $6,000

Option B: 3% yield, 8% annual dividend growth

- Start: $10,000 investment = $300/year income

- Year 5: $441/year

- Year 10: $648/year

- Total 10-year income: $4,345

But Year 11+: Option B pays MORE and grows forever

Dividend growth > high initial yield

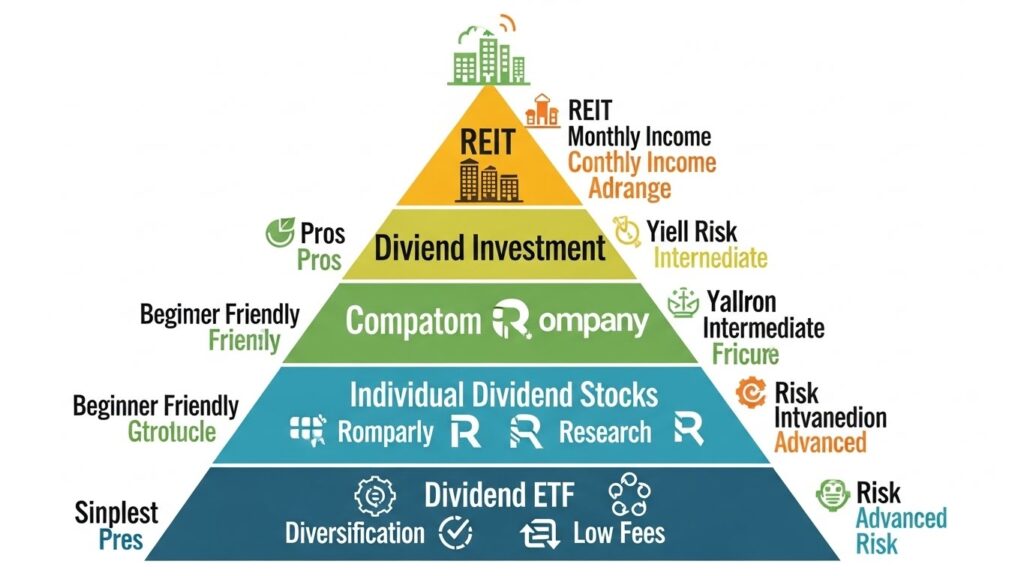

Types of Dividend Investments for Beginners

You can access dividends through various investments:

1. Individual Dividend Stocks

What they are: Shares of specific companies that pay dividends

Examples:

- Johnson & Johnson (JNJ)

- Coca-Cola (KO)

- Procter & Gamble (PG)

- Microsoft (MSFT)

- AT&T (T)

Pros:

- Choose specific companies you like

- Highest potential returns

- Can target high dividend growers

Cons:

- Requires research and monitoring

- Less diversification

- Company-specific risk (dividend cuts possible)

Best for: Investors willing to research 10-20 stocks

2. Dividend-Focused ETFs

What they are: ETFs that hold many dividend-paying stocks

Examples:

- Vanguard Dividend Appreciation (VIG) – dividend growers

- Vanguard High Dividend Yield (VYM) – high yields

- Schwab U.S. Dividend Equity (SCHD) – quality dividends

- SPDR S&P Dividend ETF (SDY) – dividend aristocrats

Pros:

- Instant diversification (50-400 stocks)

- Low fees (0.06-0.30%)

- Professional selection

- Automatic rebalancing

Cons:

- Less control

- Might include companies you don’t want

- Slightly lower yields than picking best individual stocks

Best for: Most beginners—easy, diversified, low-cost

3. Dividend-Focused Mutual Funds

What they are: Actively managed funds focusing on dividend stocks

Examples:

- Vanguard Dividend Growth Fund (VDIGX)

- T. Rowe Price Dividend Growth (PRDGX)

Pros:

- Professional active management

- Dividend growth focus

Cons:

- Higher fees (0.25-1.00%)

- Tax inefficiency

- Often underperform dividend ETFs

Best for: Investors who prefer active management (though ETFs usually better)

4. REITs (Real Estate Investment Trusts)

What they are: Companies that own income-producing real estate and must pay 90% of income as dividends

Examples:

- Realty Income (O) – “The Monthly Dividend Company”

- VICI Properties (VICI) – Gaming/hospitality real estate

- Vanguard Real Estate ETF (VNQ) – diversified REIT exposure

Pros:

- Very high yields (4-8%+)

- Monthly dividends (some)

- Real estate exposure without buying property

Cons:

- Dividends taxed as ordinary income (not qualified)

- Sensitive to interest rates

- Less growth potential

Best for: Income-focused investors, portfolio diversification (5-10% allocation)

The Best Dividend Stocks and ETFs for Beginners

Here are proven, beginner-friendly dividend investments:

Top Dividend ETFs (Start Here)

1. Schwab U.S. Dividend Equity ETF (SCHD)

- Yield: ~3.5%

- Expense Ratio: 0.06%

- Holdings: ~100 quality dividend stocks

- Why it’s great: Focuses on dividend growth + quality + value

- Best for: Core dividend holding

2. Vanguard Dividend Appreciation ETF (VIG)

- Yield: ~2%

- Expense Ratio: 0.06%

- Holdings: ~300 dividend growth stocks

- Why it’s great: 10+ years of consecutive dividend increases

- Best for: Long-term dividend growth

3. Vanguard High Dividend Yield ETF (VYM)

- Yield: ~3%

- Expense Ratio: 0.06%

- Holdings: ~450 high-yielding stocks

- Why it’s great: Broad diversification, higher income

- Best for: Income focus with diversification

4. SPDR S&P Dividend ETF (SDY)

- Yield: ~2.5%

- Expense Ratio: 0.35%

- Holdings: Dividend Aristocrats (20+ years of increases)

- Why it’s great: Only companies with long dividend track records

- Best for: Quality and reliability focus

Individual Dividend Stocks (If You Want Specific Companies)

The S&P Dividend Aristocrats are companies that have increased dividends

for 25+ consecutive years, representing quality and reliability.

Dividend Aristocrats (25+ years of increases):

Johnson & Johnson (JNJ)

- Yield: ~3%

- Sector: Healthcare

- 60+ years of dividend increases

- Rock-solid, recession-resistant

Coca-Cola (KO)

- Yield: ~3%

- Sector: Consumer Staples

- 60+ years of dividend increases

- Warren Buffett favorite

Procter & Gamble (PG)

- Yield: ~2.5%

- Sector: Consumer Staples

- 65+ years of dividend increases

- Essential products (Tide, Pampers, Gillette)

3M Company (MMM)

- Yield: ~6%

- Sector: Industrials

- 65+ years of dividend increases

- Diversified industrial giant

High-Growth Dividend Stocks:

Microsoft (MSFT)

- Yield: ~0.8%

- Lower yield BUT: 15%+ annual dividend growth

- Plus significant stock price appreciation

- Best of both worlds

Visa (V)

- Yield: ~0.7%

- 10%+ annual dividend growth

- Dominant payment processor

- Growth + rising income

REITs for Monthly Income:

Realty Income (O)

- Yield: ~5.5%

- Pays monthly (not quarterly!)

- 600+ consecutive monthly dividends

- “The Monthly Dividend Company”

How to Build a Dividend Portfolio from Scratch

Step-by-step process to start from zero:

Step 1: Determine Your Goal

Ask yourself:

- Time horizon: When do I need income? (5 years? 20 years? Retirement?)

- Income need: How much monthly/annual income do I want eventually?

- Risk tolerance: Can I handle some volatility for higher growth?

This determines your strategy:

Goal: Income NOW (near retirement):

- Focus: High-yield dividend stocks/ETFs (4-5% yield)

- Strategy: VYM, SCHD, high-yield individuals, REITs

Goal: Income in 20+ years:

- Focus: Dividend growth stocks/ETFs (2-3% yield growing 8-10%/year)

- Strategy: VIG, dividend aristocrats, Microsoft, Visa

Goal: Balanced (income + growth):

- Focus: Mix of both

- Strategy: 50% SCHD, 30% VIG, 20% REITs

Step 2: Choose Your Core Holdings

For most beginners, start simple:

Option 1: One-Fund Approach

- 100% SCHD or VIG

- Perfect for beginners

- Instant diversification

Option 2: Two-Fund Approach

- 70% SCHD (quality dividends)

- 30% VNQ (REIT exposure for higher yield)

Option 3: Three-Fund Dividend Portfolio

- 50% SCHD (core quality dividends)

- 30% VIG (dividend growth)

- 20% VNQ (REITs for income)

Start with Option 1 or 2. Keep it simple.

Step 3: Determine How Much to Invest

Calculate based on income:

- Save 15-20% of income for all investing

- Allocate portion to dividends based on goals

Example:

- Income: $60,000/year

- Save 15% = $9,000/year ($750/month)

- Allocation: 60% dividend focus = $450/month to dividend portfolio

Or start with whatever you have:

- $100/month

- $500 one-time

- Whatever works—just start!

Step 4: Open the Right Account

Account types:

For retirement (tax-advantaged):

- Roth IRA (best for dividends—tax-free growth!)

- Traditional IRA

- 401(k) (if available in plan)

For non-retirement income:

- Taxable brokerage account

- Note: Qualified dividends get favorable tax treatment

Best brokers for dividend investing:

- Fidelity (great dividend research tools)

- Charles Schwab (SCHD is their ETF)

- Vanguard (dividend-focused company)

Step 5: Make Your First Purchase

How to buy:

If using ETFs:

- Log into brokerage

- Search ticker (e.g., “SCHD”)

- Click “Buy”

- Enter amount ($500) or shares (calculate: $500 ÷ share price)

- Market order (during market hours) or limit order

- Confirm

If fractional shares available:

- Just enter dollar amount ($100, $500, etc.)

- Broker calculates fractional shares

Step 6: Set Up Automatic Dividend Reinvestment (DRIP)

CRITICAL STEP:

- Go to account settings

- Find “Dividend Reinvestment” or “DRIP”

- Turn ON for all holdings

- Now all dividends automatically buy more shares

This is how compound growth happens!

Step 7: Add Consistently

Dollar-cost averaging into your dividend portfolio:

- Invest same amount each month

- $100, $200, $500—whatever you can afford

- Automated if possible

Example:

- $300/month into SCHD

- Automatic purchase on 1st of month

- DRIP enabled

- Hands-off wealth building

The Power of Dividend Reinvestment (DRIP)

DRIP (Dividend Reinvestment Plan) is the secret weapon of dividend investing:

What is DRIP?

Instead of receiving dividend cash, it automatically buys more shares:

Without DRIP:

- Own 100 shares

- Receive $50 dividend

- $50 sits in cash in account

- Still own 100 shares

With DRIP:

- Own 100 shares

- Receive $50 dividend

- Automatically buys 0.5 more shares (if share price is $100)

- Now own 100.5 shares

- Next dividend pays on 100.5 shares

- Snowball begins

The Compound Effect

Example: $10,000 invested in 4% yielding stock for 30 years

Without DRIP (taking cash):

- Receive $400/year in cash

- After 30 years: $12,000 in cash received

- Still own original investment (hopefully grown)

With DRIP (reinvesting):

- All dividends buy more shares

- More shares pay more dividends

- After 30 years with 5% dividend growth: Portfolio worth $45,000+

- Difference: $33,000+ from reinvesting!

Real Example: Johnson & Johnson

Scenario:

- 2005: Invest $10,000 in JNJ

- Enable DRIP

- Never add another dollar

Result by 2025:

- With DRIP: Portfolio worth ~$58,000

- Without DRIP: ~$38,000 + $8,000 cash = $46,000

- DRIP advantage: $12,000 (26% more!)

How to Enable DRIP

Most brokers:

- Account Settings → Dividend Reinvestment

- Toggle ON for each holding

- Done

Some brokers:

- Automatic for all holdings

- Can’t disable (which is good—forces discipline!)

Cost: Usually $0 (free)

Fractional shares: Most brokers now allow DRIP to buy fractional shares (if dividend is $23 and share price is $100, you get 0.23 shares)

How Much Money Do You Need to Live Off Dividends?

This is the dream: Replace your salary with dividend income. Here’s the math:

The 4% Rule Applied to Dividends

To replace income with dividends:

Annual income needed ÷ 0.04 = Portfolio size

Examples:

Need $40,000/year:

- $40,000 ÷ 0.04 = $1,000,000 portfolio at 4% yield

Need $60,000/year:

- $60,000 ÷ 0.04 = $1,500,000 portfolio

Need $30,000/year:

- $30,000 ÷ 0.04 = $750,000 portfolio

More Aggressive: 5% Yield

With higher-yielding dividend portfolio (REITs, high-yield stocks):

Need $40,000/year:

- $40,000 ÷ 0.05 = $800,000 portfolio

Need $30,000/year:

- $30,000 ÷ 0.05 = $600,000 portfolio

How Long to Get There?

Scenario: Want $40,000/year dividend income (need $1M portfolio at 4% yield)

Investing $1,000/month at 8% total return:

- Year 10: $183,000

- Year 20: $589,000

- Year 25: $947,000

- Year 27: $1,074,000 ✅ GOAL REACHED!

At this point:

- $1,074,000 × 4% yield = $42,960/year in dividends

- $3,580/month passive income

- Never sell a share

The Dividend Growth Advantage

Key insight: You don’t need to hit exact number if dividends grow

Example:

- Reach $800,000 portfolio yielding 3.5% = $28,000/year

- But dividends grow 7%/year

- Year 5: $39,200/year

- Year 7: $44,900/year

- Reached $40k+ goal through dividend growth alone!

Common Dividend Investing Mistakes to Avoid

Mistake 1: Chasing High Yields

The error: “This stock yields 12%! I’m buying!”

Why it’s dangerous:

- Usually signals distressed company

- Dividend likely unsustainable

- High yield often from falling stock price

- Dividend cut coming = lose income AND stock value crashes further

Red flags:

- Yields above 8-10% (except some REITs/MLPs)

- Payout ratio over 80% (paying out 80%+ of earnings)

- Declining revenue/profits

The fix: Focus on sustainable yields (2-5%) with growth potential

Mistake 2: Ignoring Dividend Growth

The error: Buying 6% yield with 0% growth vs 3% yield with 10% growth

Why it’s wrong:

- Year 1: 6% looks better

- Year 7: The 3% stock now yields 5.9% (on your original cost) and growing

- Year 10: The 3% stock yields 7.8% and still growing

- The 6% stock: Still yields 6%

The fix: Prioritize dividend growth rate, not just current yield

Mistake 3: Not Diversifying

The error: “I love AT&T dividends, so 100% of portfolio in AT&T”

Why it’s risky:

- Company-specific risk

- If AT&T cuts dividend (they did), entire income stream hit

- No diversification across sectors

The fix: At minimum 10-15 different stocks, or just use dividend ETF

Mistake 4: Forgetting About Taxes

The error: Holding dividend stocks in wrong account type

Tax-smart approach:

- REITs, high-yield stocks: Hold in Roth IRA (dividends taxed as ordinary income)

- Qualified dividend stocks: Can hold in taxable (favorable tax rate)

- Growth stocks: Taxable account (no dividends to be taxed annually)

The IRS provides detailed guidance on dividend taxation and qualified dividend requirements for investors.

The fix: Use Roth IRA for dividend investing when possible

Mistake 5: Taking Dividends as Cash Too Early

The error: Age 30, taking dividend cash to spend instead of reinvesting

Why it’s costly:

- Miss decades of compound growth

- That $500/year in dividends could become $5,000/year by retirement if reinvested

The fix: Reinvest ALL dividends (DRIP) until you actually need the income

Mistake 6: Ignoring the Underlying Business

The error: “It pays dividends, so it’s a good investment”

Why it’s wrong:

- Dividend doesn’t mean business is healthy

- Some companies pay unsustainable dividends to attract investors

- Need to evaluate if business can sustain and grow the dividend

The fix: Check payout ratio, revenue trends, competitive position

Your Dividend Investing Action Plan

Ready to start? Here’s your step-by-step plan:

This Week

Day 1: Decide your strategy

- Income now vs growth for later?

- Choose 1-2 dividend ETFs to start (SCHD, VIG, VYM)

Day 2: Open or use existing brokerage account

- Fidelity, Schwab, or Vanguard

- Roth IRA if possible (tax-free dividends!)

Day 3: Fund account and make first purchase

- Start with $100, $500, $1,000—whatever you have

- Buy your chosen dividend ETF(s)

Day 4: Enable DRIP

- Turn on automatic dividend reinvestment

- Critical for compound growth

Day 5: Set up automatic monthly investments

- $100, $200, $500/month

- Same day each month

- Automate it!

This Month

Week 2: Track your first dividends

- Check when your ETF pays (usually quarterly)

- Watch for first dividend payment

- Verify DRIP activated (dividend buys more shares automatically)

Week 3: Learn more

- Research individual dividend stocks (if interested)

- Read about dividend aristocrats

- Understand payout ratios

Week 4: Increase contributions if possible

- Review budget

- Find extra $50-100/month

- Redirect to dividend portfolio

This Year

Quarter 1: Build consistency

- Invest every month without fail

- Don’t check account obsessively (quarterly is enough)

- Stay invested through any volatility

Quarter 2: First dividend reinvestments happening

- See DRIP in action

- Fractional shares accumulating

- Compound effect beginning

Quarter 3: Consider adding second holding

- If started with one ETF, maybe add another

- Or add individual dividend stock (5-10% of portfolio)

- Maintain diversification

Quarter 4: Annual review

- Calculate total dividends received

- Check dividend growth rate

- Project next year’s income

- Increase monthly contribution if possible

Long-Term (5-10 Years)

Year 5:

- Built substantial position ($15,000-30,000)

- Receiving $500-1,500/year in dividends

- Snowball accelerating

Year 10:

- Portfolio $40,000-80,000

- Receiving $1,500-4,000/year in dividends

- Compound effect obvious

Year 20:

- Portfolio $150,000-300,000+

- Receiving $6,000-15,000/year in dividends

- Significant passive income stream

Year 30:

- Portfolio $400,000-800,000+

- Receiving $16,000-40,000/year in dividends

- Potentially financial independence

Frequently Asked Questions – FAQ

What is dividend investing?

Dividend investing is a strategy where you buy stocks or ETFs of companies that regularly pay dividends—cash payments to shareholders from company profits. Instead of only profiting from stock price appreciation, dividend investors receive regular income (usually quarterly) while still owning their shares. This creates a passive income stream that can grow over time through reinvestment and dividend increases.

How much money do I need to start dividend investing?

You can start dividend investing with as little as $100 by buying dividend-focused ETFs like SCHD or VIG through brokerages that offer fractional shares. Many brokers now have $0 minimums. A practical starting amount is $500-1,000 to build a small position in 1-2 dividend ETFs, then add $100-500 monthly through automatic investments. The key is starting now and investing consistently, not waiting until you have thousands.

Are dividends better than growth stocks?

Neither is inherently “better”—they serve different purposes. Dividend stocks provide immediate income and tend to be less volatile, making them ideal for investors seeking passive income or approaching retirement. Growth stocks offer potentially higher returns through price appreciation but no income and higher volatility. Most investors benefit from both: growth stocks in early accumulation years, gradually shifting toward dividends as income becomes more important.

How are dividends taxed?

In the U.S., most dividends from stocks held over 60 days are “qualified dividends” taxed at favorable capital gains rates (0%, 15%, or 20% depending on income), lower than ordinary income rates. REIT dividends are taxed as ordinary income. Dividends in retirement accounts (Roth IRA, traditional IRA, 401k) grow tax-deferred or tax-free. Holding dividend investments in a Roth IRA is ideal for tax-free dividend growth.

What is a good dividend yield for beginners?

For beginners, a dividend yield between 2-5% is ideal. Yields of 2-3% typically come from dividend growth stocks that increase payouts consistently (like Microsoft, Visa, dividend aristocrats). Yields of 3-5% come from mature, stable companies with slower growth (utilities, consumer staples). Avoid chasing yields above 6-7% as they often indicate unsustainable dividends or distressed companies. Focus on sustainable, growing dividends rather than highest current yield.

How do I reinvest dividends automatically?

Enable DRIP (Dividend Reinvestment Plan) in your brokerage account settings. Most brokers offer this free feature that automatically uses your dividend payments to purchase additional shares (including fractional shares) of the same stock or ETF. To enable: log into your broker, go to account settings, find “Dividend Reinvestment” or “DRIP,” and toggle it ON for each holding. This allows compound growth without any action needed from you.

Can you live off dividend income?

Yes, you can live off dividend income once your portfolio is large enough. Using the 4% rule, you need 25 times your annual expenses invested in dividend-paying stocks. For example, to generate $40,000/year in dividends, you need a $1,000,000 portfolio yielding 4%. This is achievable through consistent investing over 25-30 years. With a 5% yielding portfolio, you’d need $800,000. The key is starting early, investing consistently through dollar-cost averaging, and reinvesting all dividends until you need the income.

BONUS

Want to see dividend investing in action?

This video shows exactly how to build passive income through dividend stocks and ETFs:

FINAL THOUGHTS: Building Your Passive Income Machine

Here’s what most people misunderstand about dividend investing: it’s not about getting rich quickly. It’s about building a machine that pays you forever.

Every dividend stock or ETF you buy is like installing a small engine in your financial machine. Each engine produces a little bit of cash. Alone, one engine doesn’t change your life—$50 per year won’t pay your bills.

But here’s the magic: every dividend payment buys you more engines. Those new engines produce more cash, which buys even more engines.

This is compound interest in its purest form. This is the snowball effect. This is how modest investments become financial freedom.

The Math Is Simple

Start with $500/month invested in dividend stocks at 4% yield with 7% dividend growth:

- Year 5: Receiving $1,500/year in dividends ($125/month)

- Year 10: Receiving $4,200/year in dividends ($350/month)

- Year 15: Receiving $8,000/year in dividends ($667/month)

- Year 20: Receiving $13,500/year in dividends ($1,125/month)

- Year 25: Receiving $21,000/year in dividends ($1,750/month)

- Year 30: Receiving $31,000/year in dividends ($2,583/month)

All from investing $500/month consistently and reinvesting dividends.

That’s not speculation. That’s not luck. That’s mathematics combined with the power of owning quality businesses that share profits with shareholders.

The Simple Truth

You don’t need to:

- Pick the next Amazon or Tesla

- Time the market perfectly

- Trade constantly

- Be a financial genius

You need to:

- Buy quality dividend stocks or ETFs (SCHD, VIG, dividend aristocrats)

- Invest consistently ($100-500/month through dollar-cost averaging)

- Reinvest all dividends (enable DRIP and forget it)

- Give it time (decades for the compound effect)

- Stay the course (don’t sell during downturns)

That’s it. That’s the entire strategy that’s created millions of financially independent dividend investors.

Your Action This Week

Stop reading. Start doing.

Monday: Decide your goal—income now or growth for later

Tuesday: Open brokerage account (if don’t have) or use existing

Wednesday: Buy your first dividend ETF (SCHD or VIG)—even $100

Thursday: Enable DRIP for automatic dividend reinvestment

Friday: Set up automatic monthly investment

Done. Your passive income machine is now running.

Every month, you’ll add fuel. Every quarter, you’ll receive dividends that buy more shares. Every year, companies will increase their dividends. Every decade, your income will multiply.

Thirty years from now, you’ll open your account and see thousands—maybe tens of thousands—of dollars in annual dividend income. Money that arrives in your account without any work from you. Money from companies you bought decades ago. Money that keeps growing.

That’s the power of dividend investing. Start building your machine today.

INTERESTING TOPICS

Want to understand why dividend reinvestment is so powerful?

Learn about compound interest and how time creates wealth.

Ready to invest consistently in dividends?

Master dollar-cost averaging, the strategy that builds wealth automatically.

Need to know which investment vehicles to use?

Discover ETFs and why they’re perfect for dividend investing.

Want more financial insights delivered to you? Subscribe to our newsletter

and get weekly articles with practical strategies to grow your wealth sent straight to your inbox.

Disclaimer: This article is for educational purposes only. Diversification does not guarantee profits or protect against all losses. Consider your financial situation, risk tolerance, and investment timeline before making investment decisions.

—— End of Article ——