What Is Dollar-Cost Averaging and Why It Works for Beginners

Last updated: December 2025

What if there was an investment strategy so simple that you could set it up once and let it run automatically? A strategy that doesn’t require you to predict market movements, doesn’t cause sleepless nights during market crashes, and historically produces better results than trying to time the market?

That strategy exists, and it’s called dollar-cost averaging, or DCA.

Dollar-cost averaging is one of the most powerful yet underrated investment strategies available to beginners. It’s the approach Warren Buffett recommends for most investors, it’s built into every successful retirement plan, and it’s probably the single best way to remove emotion from your investment decisions.

If you’ve ever felt paralyzed wondering when to invest, worried about buying at the “wrong” time, or stressed about market volatility, dollar-cost averaging is your solution. This strategy takes the guesswork out of investing and replaces anxiety with a simple, systematic approach that works in any market condition.

In this guide, you’ll learn exactly what dollar-cost averaging is, how it works, why it’s so effective, and how to implement it in your own investment plan. By the end, you’ll have a proven strategy that successful investors have used for decades to build substantial wealth.

Let’s remove the emotion and complexity from investing, once and for all.

1. What is Dollar-Cost Averaging? (Simple Definition)

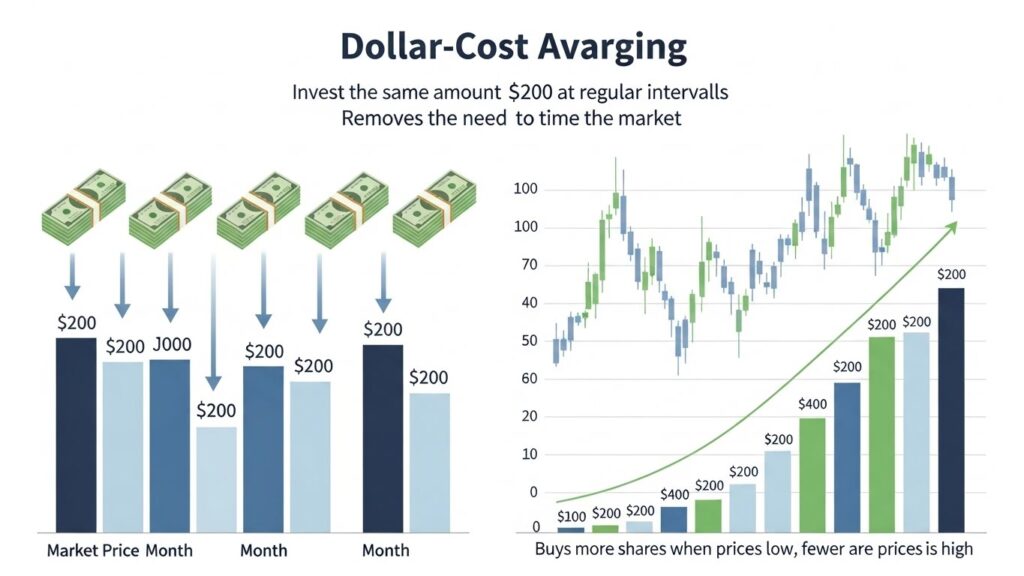

Dollar-cost averaging (DCA) is an investment strategy where you invest a fixed amount of money at regular intervals, regardless of market conditions or share prices.

In simple terms: you invest the same amount of money on the same schedule, no matter what.

Example:

- Every month, on the 1st

- You invest exactly $200

- Into the same investment (like an S&P 500 index fund)

- Whether the market is up, down, or sideways

That’s it. That’s dollar-cost averaging.

The Key Principle

Instead of trying to time the market (buying when it’s low and selling when it’s high), you invest consistently over time. Sometimes you’ll buy when prices are high. Sometimes you’ll buy when prices are low. Over time, your average purchase price smooths out.

Why It’s Called “Dollar-Cost Averaging”

You’re averaging out the cost per share over time by investing fixed dollar amounts. When prices are high, your fixed investment buys fewer shares. When prices are low, the same investment buys more shares. This naturally creates a lower average cost per share than if you had invested randomly or tried to time the market.

2. How Dollar-Cost Averaging Actually Works

Let’s break down the mechanics with a clear example.

Scenario: You have $1,200 to invest over one year

Option 1: Invest it all at once (lump sum)

- January: Invest $1,200 when share price is $100

- You buy: 12 shares

- Done

Option 2: Dollar-cost averaging

- Invest $100 per month for 12 months

- Buy shares regardless of price

Here’s what happens month by month:

| Month | Investment | Share Price | Shares Bought | Total Shares |

|---|---|---|---|---|

| Jan | $100 | $100 | 1.00 | 1.00 |

| Feb | $100 | $90 | 1.11 | 2.11 |

| Mar | $100 | $80 | 1.25 | 3.36 |

| Apr | $100 | $85 | 1.18 | 4.54 |

| May | $100 | $95 | 1.05 | 5.59 |

| Jun | $100 | $105 | 0.95 | 6.54 |

| Jul | $100 | $110 | 0.91 | 7.45 |

| Aug | $100 | $100 | 1.00 | 8.45 |

| Sep | $100 | $95 | 1.05 | 9.50 |

| Oct | $100 | $90 | 1.11 | 10.61 |

| Nov | $100 | $85 | 1.18 | 11.79 |

| Dec | $100 | $100 | 1.00 | 12.79 |

Results:

- Total invested: $1,200 (same as lump sum)

- Shares owned: 12.79 shares (more than lump sum!)

- Average cost per share: $93.80 (lower than the $100 lump sum price)

Notice what happened:

- When prices dropped (Feb-Mar, Oct-Nov), you bought more shares

- When prices rose (Jun-Jul), you bought fewer shares

- You ended up with more shares at a lower average cost

- You never had to predict which months would be cheap

That’s the magic of dollar-cost averaging—it automatically buys more when things are cheap and less when they’re expensive.

3. Why DCA is Perfect for Beginners

Dollar-cost averaging is especially powerful for new investors. Here’s why:

3.1 – Removes the Timing Problem

The #1 question new investors ask: “When should I invest?”

With DCA, the answer is simple: now, and then consistently.

You don’t need to:

- Analyze charts

- Read market predictions

- Wait for the “perfect” moment

- Worry about buying at the top

You just invest on your schedule. Done.

3.2 – Reduces Emotional Decisions

Markets go up and down. This causes fear and greed, which destroy investment returns.

Fear says: “The market is crashing! Sell everything!”

Greed says: “The market is soaring! Buy more now!”

Both emotions lead to poor decisions. DCA removes emotion from the equation. You invest the same amount whether you’re feeling optimistic, pessimistic, or anywhere in between.

3.3 – Makes Large Investments Less Scary

If you have $10,000 to invest, putting it all in at once can be terrifying. What if the market crashes tomorrow?

With DCA, you might invest $833 per month for 12 months instead. Each investment feels smaller and less risky, even though you’re deploying the same total amount.

3.4 – Builds Consistent Habits

The most important factor in building wealth isn’t picking the right stocks or timing the market—it’s consistent investing over time.

DCA forces you to invest regularly, which is exactly what builds wealth. It’s not exciting, but it works.

3.5 – Works with Any Budget

You don’t need thousands of dollars to start. With DCA, you can begin with:

- $50 per month

- $100 per month

- $500 per month

- Whatever fits your budget

The amount matters less than the consistency.

3.6 – Automatically Buys the Dip

When everyone else is panicking and selling during market drops, your DCA strategy is automatically buying at lower prices. You’re following Warren Buffett’s advice to “be fearful when others are greedy and greedy when others are fearful”—without even thinking about it.

4. Dollar-Cost Averaging vs Lump Sum Investing

Let’s address the elephant in the room: studies show that lump sum investing (investing all your money at once) statistically outperforms DCA about 66% of the time.

So why use DCA?

The Reality for Most People

Those studies assume you have a large lump sum sitting in cash right now. For most people, that’s not reality. Instead:

- You get paid monthly or biweekly

- You have a set amount you can invest from each paycheck

- You don’t have $50,000 sitting around waiting to be invested

For these situations, DCA isn’t a choice—it’s how you naturally invest.

The Psychology Factor

Even when people do have a lump sum, the psychological barrier is real. Studies don’t account for:

- The regret you’d feel if you invested $50,000 and the market crashed the next day

- The paralysis that prevents people from investing at all

- The emotional stress of watching a large investment fluctuate

DCA removes these barriers. Better to invest consistently through DCA than to sit in cash paralyzed by fear.

When Lump Sum Makes Sense

If you have a large sum and can handle the emotional aspect, lump sum investing is statistically optimal because:

- Markets trend upward over time

- More time in the market usually beats timing the market

- You capture more compound growth immediately

When DCA Makes Sense

DCA is better when:

- You’re investing from regular income (most people)

- You have a lump sum but can’t handle the emotional stress of investing it all at once

- Markets are at all-time highs and you’re nervous

- You’re a beginner still learning about investing

- You want to sleep well at night

Bottom line: The best strategy is the one you’ll actually follow. If DCA keeps you investing consistently, it’s the right choice.

5. Real Examples: DCA in Bull Markets, Bear Markets, and Volatile Markets

Let’s look at how DCA performs in different market conditions using real historical examples.

Example 1: Bull Market (2019)

Scenario: You invest $500/month throughout 2019 in an S&P 500 index fund

- January 2019: S&P 500 at ~2,600

- December 2019: S&P 500 at ~3,200

- Market gain: 23% increase

Results:

- Total invested: $6,000

- Portfolio value: ~$6,800

- Gain: ~13%

You didn’t capture the full 23% gain because you were gradually entering the market, but you still profited significantly without any market timing.

Example 2: Bear Market (2008 Financial Crisis)

Scenario: You invest $500/month through the 2008-2009 crash

- January 2008: S&P 500 at ~1,400

- March 2009: S&P 500 bottoms at ~700 (50% crash!)

- December 2009: S&P 500 recovers to ~1,100

What happened:

- Early 2008: You bought shares at higher prices

- Mid-2008 to early 2009: You bought shares at incredibly low prices

- Late 2009: Your average cost was much lower than the starting price

Results by 2012 (when market recovered):

- Those shares bought during the crash multiplied in value

- Your average cost per share was far below the 2008 starting price

- You massively outperformed someone who stopped investing during the crash

Key lesson: DCA shines brightest during crashes. While others panic and sell, you’re automatically buying at discount prices.

Example 3: Volatile Market (2020-2021)

Scenario: You invest $500/month during COVID volatility

- February 2020: S&P 500 at ~3,400

- March 2020: Crashes to ~2,200 (35% drop!)

- August 2020: Recovers to ~3,500

- December 2021: Reaches ~4,700

What DCA did:

- March-April 2020: Your $500/month bought shares at massive discounts

- Rest of 2020-2021: Those discounted shares soared in value

- You never had to predict the bottom

- You never had to decide when the recovery would start

Results:

- Total invested over 24 months: $12,000

- Portfolio value by end of 2021: ~$16,500+

- Gain: ~37%+

This happened automatically, while millions of investors were paralyzed wondering when to buy.

The Pattern Across All Scenarios

Regardless of market conditions:

- Bull markets: DCA keeps you invested and participating in gains

- Bear markets: DCA accumulates shares at low prices

- Volatile markets: DCA smooths out the ups and downs

- All markets: DCA keeps you consistent, which is what actually matters

6. How to Start Dollar-Cost Averaging Today

Ready to implement DCA? Here’s your step-by-step action plan.

Step 1: Decide How Much You Can Invest

Look at your monthly income and expenses.

Determine a realistic amount you can invest consistently without causing financial stress.

Examples:

- $50 per month

- $100 per month

- $200 per month

- 10% of each paycheck

Important: Choose an amount you can maintain long-term. Consistency matters more than the amount.

Step 2: Choose Your Investment

For beginners, the simplest approach is a broad market index fund or ETF:

Best options:

- S&P 500 index fund (VOO, SPY, IVV)

- Total stock market fund (VTI, ITOT)

- Target-date retirement fund

These give you instant diversification across hundreds or thousands of companies.

Step 3: Select Your Investment Platform

Choose a brokerage with:

- No account minimums

- Commission-free trading

- Automatic investment features

Good options:

- Vanguard

- Fidelity

- Charles Schwab

- Robinhood

- M1 Finance

Step 4: Set Up Automatic Investing

This is the crucial step that makes DCA work effortlessly.

In your brokerage account:

- Find “automatic investment” or “recurring investment” settings

- Choose your investment (the fund/ETF)

- Set your amount (e.g., $200)

- Set your frequency (e.g., monthly on the 1st)

- Link your bank account

- Turn on automatic dividend reinvestment

That’s it. Now your DCA strategy runs on autopilot.

Step 5: Set It and Forget It

The hardest part of DCA: doing nothing.

- Don’t check your account daily

- Don’t stop investing when markets drop

- Don’t increase investments when markets soar

- Just let it run

Check quarterly at most. Trust the process.

7. Common Mistakes to Avoid with DCA

Even simple strategies can be sabotaged. Avoid these errors:

Mistake 1: Stopping During Market Crashes

The error: Markets drop 20%, and you panic and stop your automatic investments.

Why it’s wrong: Market crashes are when DCA works best! You’re buying shares at discounted prices that will likely recover.

What to do: Keep investing through downturns. Better yet, don’t even look at your account during crashes.

Mistake 2: Increasing Investments During Bull Markets

The error: Markets are up 30%, you feel confident, and you double your investment amount.

Why it’s wrong: You’re buying more when prices are high (the opposite of what you want). Plus, you might not sustain the higher amount, breaking your consistency.

What to do: Stick to your predetermined amount regardless of market conditions.

Mistake 3: Trying to Time Individual Purchases

The error: Your automatic investment is set for the 1st, but markets dropped on the 28th, so you manually invest early to “catch the dip.”

Why it’s wrong: You’re defeating the purpose of DCA, which is to remove timing decisions. Plus, you might miss the automation next month.

What to do: Pick a date and stick to it. Don’t micromanage.

Mistake 4: Checking Your Account Too Often

The error: You check your investment balance daily or weekly.

Why it’s wrong: Short-term volatility will stress you out and tempt you to make emotional decisions.

What to do: Check quarterly or even just annually. Focus on your contribution consistency, not short-term performance.

Mistake 5: Choosing Too High of an Amount

The error: You commit to $500/month when you can realistically only sustain $300/month.

Why it’s wrong: After a few months, you’ll need to skip contributions or stop entirely, breaking the consistency that makes DCA work.

What to do: Start conservative. You can always increase later. Consistency beats amount.

Mistake 6: Not Reinvesting Dividends

The error: You take dividend payments as cash instead of reinvesting them.

Why it’s wrong: Dividends are part of your returns. Not reinvesting them means missing out on compound growth.

What to do: Turn on automatic dividend reinvestment (DRIP) in your account settings.

8. Frequently Asked Questions

What is dollar-cost averaging in simple terms?

Dollar-cost averaging means investing the same amount of money at regular intervals (like $200 every month) regardless of whether markets are up or down. This strategy removes the need to time the market and automatically buys more shares when prices are low and fewer when prices are high.

Is dollar-cost averaging better than lump sum investing?

Statistically, lump sum investing outperforms DCA about 66% of the time because markets generally trend upward. However, DCA is better for most people because it removes emotional barriers, works with regular income, and ensures consistent investing. The best strategy is the one you’ll actually follow.

How much should I invest with dollar-cost averaging?

Invest an amount you can sustain consistently long-term. This might be $50, $100, $500, or more per month depending on your income and expenses. Start conservatively—you can always increase later. Consistency matters far more than the amount.

Should I keep dollar-cost averaging during a market crash?

Absolutely yes! Market crashes are when DCA is most valuable. When you continue investing during crashes, you’re buying shares at discounted prices that will likely recover and grow. Some of your best returns will come from shares purchased during downturns.

How long should I use dollar-cost averaging?

For most people, DCA should be a lifelong strategy. As long as you’re earning income and building wealth, continue investing consistently. The power of DCA comes from decades of consistent contributions, not months or years.

Can I use dollar-cost averaging with individual stocks?

You can, but it’s not recommended for beginners. DCA works best with diversified investments like index funds or ETFs. Individual stocks carry more risk and volatility, which can undermine the benefits of DCA if the company struggles or fails.

Final Thoughts: The Strategy That Actually Works

Dollar-cost averaging isn’t sexy. It won’t make you rich overnight.

It won’t give you exciting stories about timing the market perfectly or finding the next big stock.

But here’s what it will do:

It will make you wealthy over time.

DCA is the strategy used by:

- Successful retirement savers in 401(k) plans

- Investors who sleep well at night

- People who build multi-million dollar portfolios from regular paychecks

- Anyone who wants consistent results without constant stress

The Simple Truth

You don’t need to:

- Predict market movements

- Spend hours analyzing stocks

- Feel anxious about “missing the bottom”

- Make perfect decisions

You just need to:

- Choose an amount you can invest consistently

- Set up automatic investments

- Let it run for decades

- Live your life

That’s it. That’s the strategy that works.

Your Action Plan This Week

Stop overthinking. Start doing:

Today:

- Decide your monthly investment amount

- Choose a broad market index fund

This week:

- Open a brokerage account (if you don’t have one)

- Set up automatic monthly investments

- Turn on dividend reinvestment

Forever:

- Let it run

- Add more when you can

- Trust the process

Twenty years from now, you’ll look back at the day you started dollar-cost averaging as one of the best financial decisions you ever made.

The market will have good years and bad years. You’ll invest through recessions and recoveries. Through bull markets and bear markets. Through volatility and calm.

But through it all, you’ll be consistently building wealth without stress, anxiety, or complexity.

That’s the power of dollar-cost averaging. That’s how ordinary people build extraordinary wealth.

Start today.

Your future self will thank you.

BONUS

If you want to see a practical example of how beginners can start investing with a small budget,

this video explains the process step by step in a simple and realistic way.

CONCLUSION

Dollar-Cost Averaging is one of the smartest strategies for anyone who wants to invest without emotional stress. By focusing on consistency instead of timing, this approach helps beginners build wealth steadily and confidently.

You do not need to predict the market. You do not need large amounts of money.

You only need discipline, patience, and time.

Start small, stay consistent, and let Dollar-Cost Averaging work for you.

INTERESTING TOPICS

Ready to begin?

Check out our guide on how to start investing with $100 to take your first step today!

Want to understand why consistent investing works?

Read about compound interest and see the math behind long-term wealth building.

Want more financial insights delivered to you? Subscribe to our newsletter

and get weekly articles with practical strategies to grow your wealth sent straight to your inbox.

Obs: Sign up for our newsletter and receive a free Finance For Beginner eBook.

Disclaimer: This article is for educational purposes only. Dollar-cost averaging does not guarantee profits or protect against losses in declining markets. Consider your financial situation and risk tolerance before investing.

—— End of Article ——