Emergency Fund 101: How Much Do You Really Need?

Last updated: January 2026

Imagine this: Your car breaks down and the repair costs $1,200. Or you lose your job unexpectedly. Or a medical emergency hits and you have a $2,000 deductible to pay. Without an emergency fund, these situations force you into debt, derail your financial progress, and create enormous stress.

Now imagine having $10,000 sitting safely in a savings account. The car breaks down? Annoying, but manageable. Job loss? You have 3-4 months to find something new without panic. Medical emergency? You pay it and move on. That’s the power of an emergency fund.

An emergency fund is the foundation of financial security. It’s the difference between a temporary setback and a financial catastrophe. It’s what allows you to invest confidently, knowing you won’t be forced to sell investments at the worst possible time. Yet most people either don’t have one or have built it incorrectly.

In this guide, you’ll learn exactly what an emergency fund is, why it’s non-negotiable, how much you actually need based on your specific situation, where to keep it, how to build it from zero, and the common mistakes that leave people financially vulnerable despite having savings.

Let’s build your financial safety net, once and for all.

What is an Emergency Fund? (Clear Definition)

An emergency fund is money set aside in a safe, easily accessible account specifically for unexpected expenses or financial emergencies. It’s separate from your checking account, investment accounts, or money saved for specific goals.

In simple terms: A financial cushion that protects you when life throws unexpected problems your way.

Key Characteristics:

Purpose: Cover unexpected expenses without going into debt or disrupting your financial plans

Accessibility: Available within 1-3 days when needed (high liquidity)

Safety: Protected from loss (FDIC-insured savings account, not investments)

Separation: Kept separate from money used for daily expenses or planned purchases

Size: Typically 3-6 months of essential living expenses

What Qualifies as an Emergency:

True emergencies:

- Job loss or income reduction

- Major medical expenses not covered by insurance

- Urgent car repairs needed for work

- Critical home repairs (broken furnace, roof leak, etc.)

- Emergency travel (family emergency in another state)

NOT emergencies:

- Sales or deals you don’t want to miss

- Planned expenses (holiday shopping, annual insurance)

- Non-essential purchases (new TV, vacation)

- Predictable costs (car registration, property taxes)

The emergency fund is for the unexpected, not the inconvenient.

Why You Absolutely Need an Emergency Fund

An emergency fund isn’t optional—it’s the foundation your entire financial life is built on. Here’s why:

1. Prevents Debt Spiral

Without emergency fund:

- Car breaks down → put $1,200 on credit card at 18% interest

- Can only make minimum payments → takes years to pay off

- Total paid with interest: $2,000+

- Meanwhile, more emergencies happen → more debt

- Debt compounds faster than you can pay it off

With emergency fund:

- Car breaks down → pay $1,200 from savings

- No interest, no debt

- Gradually rebuild emergency fund

- Financial progress continues

2. Protects Your Investments

The scenario: Market drops 20% and you lose your job.

Without emergency fund:

- Need money for rent and food

- Forced to sell investments at 20% loss

- Lock in losses permanently

- Miss the eventual recovery

- Lose years of progress

With emergency fund:

- Use emergency fund for 3-6 months of expenses

- Keep investments untouched

- Let them recover and grow

- Find new job without panic-selling

Historical example: During the 2020 COVID crash, people with emergency funds kept their investments and recovered within months. Those without sold at the bottom and missed the fastest recovery in history.

3. Reduces Financial Stress and Anxiety

Studies show: Financial stress is the #1 cause of stress for Americans, affecting:

- Physical health (sleep, blood pressure, immune system)

- Mental health (anxiety, depression)

- Relationships (money fights are a top cause of divorce)

- Work performance (distraction, reduced productivity)

With an emergency fund:

- Sleep better knowing you’re protected

- Handle unexpected expenses calmly

- Make better financial decisions (not panic-driven)

- Focus on long-term goals instead of short-term survival

4. Enables Confident Investing

You should only invest money you won’t need for 5+ years. But how can you be confident about that without an emergency fund?

Without emergency fund:

- “What if I need this money next month?”

- Keep everything in savings → lose to inflation

- Miss out on compound growth

With emergency fund:

- Know emergencies are covered

- Invest confidently for long-term growth

- Don’t panic during market drops

- Build real wealth over time

5. Provides Flexibility and Opportunity

Emergency funds aren’t just defensive—they’re offensive too:

Career opportunities:

- Can take a lower-paying job with better long-term prospects

- Can negotiate from position of strength (not desperate)

- Can take time to find the RIGHT job, not just ANY job

- Can invest in skills/certifications while between jobs

Life opportunities:

- Can help family members in crisis

- Can relocate for better opportunities

- Can say no to toxic situations (bad job, bad roommate)

- Have freedom to make life-improving changes

How Much Should You Have in Your Emergency Fund?

The standard advice is “3-6 months of expenses,” but your specific situation matters. Let’s break it down:

Calculate Your Monthly Essential Expenses

First, determine what you actually need per month for essentials only:

Include:

- Housing (rent/mortgage, utilities, property tax, insurance)

- Food (groceries, not restaurants)

- Transportation (car payment, insurance, gas, public transit)

- Insurance (health, life, disability)

- Minimum debt payments (student loans, credit cards)

- Essential bills (phone, internet for work)

- Basic healthcare costs

Don’t include:

- Entertainment subscriptions

- Dining out

- Vacations

- Shopping

- Gym memberships

- Non-essential subscriptions

- Savings and investment contributions

Example calculation:

- Rent: $1,200

- Utilities: $150

- Food: $400

- Car payment: $300

- Car insurance: $100

- Gas: $150

- Health insurance: $200

- Phone: $50

- Internet: $60

- Minimum debt payments: $200 Total: $2,810/month in essentials

The 3-6 Month Rule Explained:

3 months minimum ($8,430 in example above):

Choose 3 months if you:

- Have stable employment (government, tenured positions)

- Have dual incomes (partner also works)

- Have minimal dependents

- Live in low cost-of-living area

- Have strong family support system

- Work in high-demand field with quick re-employment

6 months recommended ($16,860 in example above):

Choose 6 months if you:

- Single income household

- Self-employed or commission-based income

- Work in volatile industry (tech layoffs, seasonal work)

- Have dependents (children, elderly parents)

- Live in high cost-of-living area

- Have health concerns or chronic conditions

- Limited family support

Beyond 6 months (up to 12 months):

Choose 9-12 months if you:

- Highly specialized career (hard to find new position)

- Older worker (age discrimination in job market)

- Live in area with limited job opportunities

- Planning to start a business soon

- Pregnant or planning pregnancy

- Have high-needs dependents

- Simply sleep better with more cushion

Special Situations:

Variable income (freelance, commission, gig economy):

- Target: 6-12 months

- You need more buffer due to income unpredictability

- Calculate based on average lean months, not average overall

High-interest debt:

- Target: $1,000-2,000 mini fund first

- Focus on paying off debt

- Then build full 3-6 month fund

Starting from zero:

- Target: $1,000 starter fund immediately

- Then build to 3 months

- Finally reach 6 months

Quick Reference Table:

| Situation | Recommended Fund |

|---|---|

| Stable job, dual income, no dependents | 3 months |

| Average stability, some risk factors | 4-5 months |

| Single income, dependents, or variable income | 6 months |

| High risk job, self-employed, or health issues | 9-12 months |

| Starting from zero | $1,000 first, then build to full amount |

Where Should You Keep Your Emergency Fund?

Your emergency fund needs to be safe and accessible, but should also earn some interest. Here are your options:

Best Option: High-Yield Savings Account

What it is: An FDIC-insured savings account that pays significantly more interest than traditional bank accounts.

Current rates (as of late 2024): 4-5% APY (rates vary with economy)

Pros:

- FDIC insured (safe up to $250,000)

- Easy access (transfer to checking in 1-3 days)

- Earns decent interest (beats inflation or comes close)

- No risk of loss

Cons:

- Not instant access (1-3 day transfer)

- Interest rates fluctuate with Fed policy

The FDIC provides deposit insurance that protects your money in case of bank failure, making high-yield savings accounts one of the safest places for emergency funds.

Best providers:

- Marcus by Goldman Sachs

- Ally Bank

- American Express Personal Savings

- Capital One 360

- Discover Online Savings

Ideal for: Most people. This is the default choice.

Alternative: Money Market Account

What it is: Similar to high-yield savings but may offer check-writing or debit card access.

Current rates: 4-5% APY (similar to high-yield savings)

Pros:

- FDIC insured

- Slightly faster access (some allow checks/debit)

- Competitive interest rates

Cons:

- May have higher minimum balance requirements

- Some limit monthly transactions

- Slightly more complex

Ideal for: People who want faster access or prefer traditional banking features.

Starter Option: Regular Savings Account

What it is: Traditional savings account at your current bank.

Current rates: 0.01-0.50% APY (very low)

Pros:

- Convenient (same bank as checking)

- Easy transfers

- Familiar

Cons:

- Terrible interest rates (loses to inflation)

- Leaving money on the table

Ideal for: Your initial $1,000 starter fund while you research better options, then move to high-yield savings.

NOT Recommended Options:

Checking Account:

- ❌ No separation from daily spending

- ❌ Too tempting to use for non-emergencies

- ❌ No meaningful interest

Stocks/Index Funds:

- ❌ Can lose 20-50% in market crashes

- ❌ Might need emergency fund exactly when market is down

- ❌ Defeats the purpose of “safe” money

CDs (Certificates of Deposit):

- ❌ Money locked up for months/years

- ❌ Early withdrawal penalties

- ❌ Not accessible for actual emergencies

Crypto:

- ❌ Extremely volatile (can lose 70%+ in weeks)

- ❌ Not FDIC insured

- ❌ Completely inappropriate for emergency funds

Under your mattress:

- ❌ No interest (loses to inflation)

- ❌ Risk of theft or loss

- ❌ Not FDIC protected

The Right Strategy:

For your first $1,000: Use whatever savings account you have now (just start!)

Once you have $1,000: Open a high-yield savings account and transfer it

As you build to 3-6 months: Keep everything in that high-yield savings account

When fully funded: Keep it there and forget about it unless there’s an actual emergency

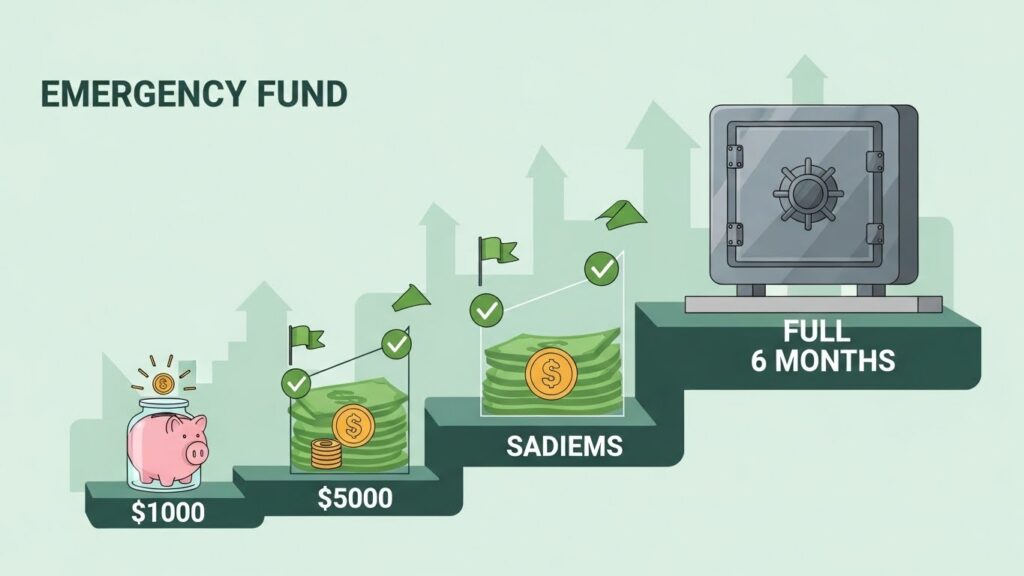

How to Build Your Emergency Fund from Zero

Building an emergency fund feels overwhelming when you’re starting from nothing. Here’s a realistic, step-by-step approach:

Phase 1: The Mini Emergency Fund ($1,000)

Goal: Get $1,000 in savings as quickly as possible.

Why $1,000? It covers most common small emergencies (minor car repair, urgent doctor visit, emergency plane ticket).

Timeline: 1-3 months

How to do it:

Week 1-2: Find the money

- Review last month’s spending

- Cut all non-essentials temporarily (streaming, dining out, coffee shops)

- Identify one-time income opportunities

Week 3-8: Intense savings mode

- Save 50% or more of every paycheck

- Sell items you don’t need

- Pick up overtime or side gig if possible

- Use any tax refund, bonus, or gift money

Quick wins to reach $1,000 faster:

- $200: Cancel unused subscriptions for 2 months

- $300: Pack lunch instead of eating out for 6 weeks

- $200: Sell unused items (clothes, electronics, furniture)

- $200: Skip non-essential purchases (new clothes, gadgets)

- $100: One side gig (delivery, freelance task, babysitting)

Total: $1,000 in 2 months

Phase 2: Build to 3 Months ($8,000-10,000)

Goal: Reach 3 months of essential expenses.

Timeline: 6-12 months

How to do it:

Systematic approach:

- Save 15-20% of every paycheck

- Automate transfers to savings on payday

- Maintain reduced spending in some areas

- Put windfalls toward emergency fund (tax refund, bonus, gifts)

Monthly savings examples:

- Income $3,000/month → save $450-600/month → 3 months funded in 15-18 months

- Income $5,000/month → save $750-1,000/month → 3 months funded in 8-12 months

- Income $7,000/month → save $1,050-1,400/month → 3 months funded in 6-8 months

Strategies to accelerate:

- The 50/50 rule: Split every bonus, tax refund, or raise 50/50 between emergency fund and fun

- The automatic increase: Increase savings by 1% of income each month

- The side income dedic ation: 100% of side hustle income goes to emergency fund

- The expense challenge: Challenge yourself to cut one expense category by 50% for 3 months

Phase 3: Complete to 6 Months ($16,000-20,000)

Goal: Reach full 6 months of essential expenses.

Timeline: 12-24 months total (from zero)

How to do it:

Maintenance mode:

- Continue saving 10-15% of income

- Less intense than Phases 1 and 2

- Allow some lifestyle improvements

- Celebrate milestones ($5K, $10K, $15K, $20K)

At this point:

- Life feels much more stable

- Financial stress significantly reduced

- Can start investing more aggressively

- Have true financial security

Real-Life Examples:

Example 1: Sarah (Income: $3,500/month, Essential expenses: $2,200)

- Month 1-2: Aggressive saving, reached $1,000

- Month 3-14: Saved $400/month, reached $6,600 (3 months)

- Month 15-26: Saved $300/month, reached $13,200 (6 months)

- Total time: 26 months from zero to fully funded

Example 2: Mike (Income: $5,500/month, Essential expenses: $3,000)

- Month 1: Intense focus, reached $1,000

- Month 2-10: Saved $800/month, reached $9,000 (3 months)

- Month 11-20: Saved $700/month, reached $18,000 (6 months)

- Total time: 20 months from zero to fully funded

Example 3: Lisa (Income: $2,800/month, Essential expenses: $2,000)

- Month 1-3: Saved $300/month + sold items, reached $1,000

- Month 4-20: Saved $250/month, reached $6,000 (3 months)

- Month 21-44: Saved $200/month, reached $12,000 (6 months)

- Total time: 44 months from zero to fully funded

The point: It takes time, but it’s absolutely doable at any income level with consistency and discipline.

When to Use Your Emergency Fund (and When Not To)

Knowing when to tap your emergency fund is just as important as building it.

USE Your Emergency Fund For:

1. Job Loss or Income Reduction

- Lost your job unexpectedly

- Hours cut significantly

- Business income dried up

- Laid off or furloughed

Why it qualifies: This is THE primary purpose of an emergency fund—surviving income disruption without going into debt.

2. Major Medical Expenses

- Emergency room visit

- Unexpected surgery

- High deductible or out-of-pocket max

- Critical prescription not covered by insurance

Why it qualifies: Health emergencies can’t wait and costs are often substantial.

3. Urgent Home Repairs

- Broken furnace in winter

- Major roof leak

- Burst pipe flooding

- Broken water heater

Why it qualifies: These affect safety, habitability, or will cause much greater damage if not fixed immediately.

4. Critical Car Repairs (if car needed for work)

- Transmission failure

- Engine problems

- Major brake issues

Why it qualifies: If you need your car to get to work and earn income, this is legitimate.

5. Emergency Travel

- Family member hospitalized far away

- Funeral expenses

- Crisis requiring immediate presence

Why it qualifies: True family emergencies are unexpected and time-sensitive.

DO NOT Use Your Emergency Fund For:

1. Planned Expenses You Forgot About

- Annual insurance premium

- Car registration

- Holiday shopping

- Property taxes

Why it doesn’t qualify: These are predictable. Budget for them separately.

2. Wants Disguised as Needs

- “My laptop is slow” (not broken)

- “My clothes are old” (not unwearable)

- “My phone is two generations old” (still works)

Why it doesn’t qualify: These are wants, not needs. Save separately for upgrades.

3. Sales or Deals

- “This sale only happens once a year!”

- “I’m saving money by buying now!”

- “This is such a good investment!”

Why it doesn’t qualify: True emergencies don’t come with discount codes.

4. Non-Essential Home Projects

- Kitchen remodel

- Landscaping

- Cosmetic repairs

- Room additions

Why it doesn’t qualify: These improve quality of life but aren’t urgent. Save separately.

5. Vacations or Entertainment

- “I really need a break”

- “This trip is once-in-a-lifetime”

- Concert or event tickets

Why it doesn’t qualify: Mental health breaks are important, but plan and save for them separately.

The Decision Framework:

Ask yourself three questions:

- Is this unexpected? (If you could have predicted it, it’s not an emergency)

- Is this urgent? (Does it need to happen now, or can it wait?)

- What happens if I don’t address this immediately? (Serious consequences = emergency)

If all three answers are yes → use emergency fund

If any answer is no → find another way to pay

How to Rebuild After Using Your Emergency Fund

You had to tap your emergency fund. That’s exactly what it was there for—good job! Now, how do you rebuild it?

Step 1: Assess the Damage

Calculate:

- Emergency fund before: $________

- Amount used: $________

- Current balance: $________

- Amount needed to replenish: $________

Example:

- Had: $12,000

- Used: $4,000 for job loss expenses

- Current: $8,000

- Need to rebuild: $4,000

Step 2: Prioritize Replenishment

Rebuilding priority depends on why you used it:

If you used it for job loss:

- Priority: HIGH (your income is unstable)

- Target: Get back to 3 months minimum ASAP

- Approach: Save aggressively from new job income

If you used it for one-time emergency:

- Priority: MODERATE (emergency resolved)

- Target: Rebuild steadily over 6-12 months

- Approach: Resume normal savings rate

Step 3: Create Rebuild Plan

Set a timeline:

- Small amount used ($500-2,000): Rebuild in 2-4 months

- Moderate amount ($2,000-5,000): Rebuild in 6-10 months

- Large amount ($5,000-10,000+): Rebuild in 12-18 months

Calculate monthly savings needed:

- Amount to rebuild ÷ months = monthly savings target

- Example: $4,000 ÷ 8 months = $500/month

Step 4: Find the Money

Income sources:

- Redirect any funds that were going to other goals temporarily

- Reduce investment contributions slightly (keep 401k match minimum)

- Take on temporary side work

- Sell items you no longer need

Expense reductions:

- Cut discretionary spending by 20-30%

- Pause subscriptions temporarily

- Reduce dining out

- Delay planned purchases

Step 5: Prevent Future Depletion

Analyze what happened:

- Was this truly unpredictable?

- Could better planning have prevented it?

- Do I need insurance I don’t have? (health, disability, car)

- Should my emergency fund be larger?

Adjust if needed:

- Increase emergency fund target if you’re in higher-risk situation

- Get appropriate insurance to reduce future emergency costs

- Create “sinking funds” for predictable large expenses

Example: If you used emergency fund for car repair, start a separate “car maintenance fund” with $100/month so next repair doesn’t touch emergency fund.

Common Emergency Fund Mistakes

Avoid these errors that leave people financially vulnerable:

Mistake 1: Not Having One at All

The error: “I’ll start saving once I pay off debt / get a raise / feel more comfortable.”

Why it’s dangerous: Emergencies don’t wait for convenient timing. Without any fund, the next emergency creates debt, starting a vicious cycle.

The fix: Start with just $1,000. That small buffer prevents most issues from becoming catastrophes.

Mistake 2: Keeping It Too Accessible

The error: Emergency fund in checking account or easily transferred with one click.

Why it’s dangerous: Too tempting to use for non-emergencies. “I’ll just borrow $500 for this thing and pay it back” rarely works as planned.

The fix: Keep in separate high-yield savings at different bank. Transfers take 1-3 days, creating barrier for impulse decisions but still accessible for real emergencies.

Mistake 3: Investing Your Emergency Fund

The error: “Savings accounts earn nothing. I’ll put my emergency fund in stocks/crypto/index funds to earn more.”

Why it’s dangerous: You need emergency fund exactly when markets crash (job loss during recession). Your $10,000 might be worth $7,000 when you desperately need it.

The fix: Investing is for long-term money. Emergency fund is for safety, not growth. Keep it in FDIC-insured savings.

Mistake 4: Building Too Small of a Fund

The error: “$1,000 is enough. That covers most things.”

Why it’s dangerous: Job loss (the biggest emergency) isn’t covered by $1,000. You’ll still face crisis when income stops.

The fix: $1,000 is a starter only. Build to full 3-6 months of essential expenses based on your situation.

Mistake 5: Never Using It for Legitimate Emergencies

The error: “My emergency fund is sacred. I’ll figure out another way” even for true emergencies.

Why it’s dangerous: You go into debt to avoid using your emergency fund, defeating its entire purpose. Credit card debt at 18% while emergency fund earns 4% makes no sense.

The fix: That’s literally what it’s for! Use it for real emergencies, then rebuild. Don’t let perfect be the enemy of good.

Mistake 6: Stopping Once You Reach Your Goal

The error: Hit $15,000 target, completely stop emergency fund contributions.

Why it’s dangerous: Lifestyle inflation eats into your cushion, or your expenses increase but fund doesn’t grow with them.

The fix: Review emergency fund annually. If expenses increased, increase fund. Periodically add small amounts to account for inflation.

Mistake 7: Using Low-Interest Account

The error: Keeping $20,000 in account earning 0.01% when high-yield savings offers 4-5%.

Why it’s costly:

- $20,000 at 0.01% = $2/year

- $20,000 at 4.00% = $800/year

- Lost: $798/year = $7,980 over decade

The fix: Takes 15 minutes to open high-yield savings. That $800/year is free money.

Frequently Asked Questions – FAQ 👈

How much should I have in my emergency fund?

Most people should have 3-6 months of essential living expenses saved in an easily accessible account. Calculate your monthly costs for housing, food, transportation, insurance, and minimum debt payments, then multiply by 3-6 depending on job stability, income sources, and dependents. Start with $1,000 as a mini emergency fund, then build to 3 months, then reach 6 months for full protection.

Should I build an emergency fund or pay off debt first?

Start with a $1,000-2,000 mini emergency fund first, then aggressively pay off high-interest debt (credit cards over 15%), then build your full 3-6 month emergency fund. This prevents new debt from emergencies while tackling existing debt. Exception: always get your full employer 401(k) match before focusing entirely on debt—it’s free money with immediate 100% return.

Where is the best place to keep an emergency fund?

Keep your emergency fund in a high-yield savings account at an FDIC-insured online bank earning 4-5% interest. This provides safety, accessibility within 1-3 days, and decent interest that fights inflation. Do NOT invest emergency funds in stocks, crypto, or other volatile assets. Do NOT keep it in checking (too tempting to spend) or under your mattress (no interest, no FDIC protection).

Can I invest my emergency fund to earn more?

No. Your emergency fund should never be invested in stocks, bonds, index funds, crypto, or anything with market risk. Emergency funds exist to be available exactly when you need them—often during market crashes or recessions when investments are down 20-50%. Investments are for long-term money you won’t need for 5+ years. Emergency funds are for safety and immediate access.

How long does it take to build an emergency fund?

Building a full 6-month emergency fund typically takes 12-24 months from zero, depending on income and expenses. Most people can save $1,000 in 1-3 months with focused effort, reach 3 months of expenses in 6-12 months, and complete the full 6 months in 12-24 months. Higher income or aggressive saving shortens this timeline; lower income or higher expenses extends it. The key is consistency, not speed.

What counts as an emergency for using my emergency fund?

True emergencies are unexpected, urgent situations with serious consequences if not addressed immediately: job loss, major medical expenses, critical home repairs (broken furnace, roof leak), essential car repairs for work transportation, or emergency family travel. NOT emergencies: planned expenses, sales and deals, wants disguised as needs, vacations, or non-urgent purchases. Ask: Is it unexpected? Is it urgent? What happens if I wait? If all three indicate crisis, it’s an emergency.

BONUS

Want to see emergency fund strategies in action?

This video shows exactly how much you need and how to build it step by step:

FINAL THOUGHTS: Your Financial Foundation Starts Here

Here’s the uncomfortable truth: you can’t build wealth without first building security.

You can’t invest confidently when you’re one car repair away from financial disaster. You can’t pursue opportunities when you’re trapped by financial fear. You can’t make good decisions when every choice feels like a potential catastrophe.

The emergency fund is what changes everything.

It’s not the sexiest financial topic. Nobody brags about their emergency fund at parties. It won’t make you rich. It just sits there, earning modest interest, doing apparently nothing.

Until the day it saves you.

That day when your car dies, your emergency fund covers it. No debt. No crisis. Just a minor inconvenience that you</parameter> <parameter name=”new_str”>That day when your car dies, your emergency fund covers it. No debt. No crisis. Just a minor inconvenience that you handle and move on from.

That day when you lose your job, your emergency fund gives you 6 months to find the RIGHT opportunity, not just ANY job out of desperation.

That day when a medical emergency hits, your emergency fund means you focus on health, not money.

That’s what financial security feels like.

The Simple Truth

Building an emergency fund isn’t about getting rich. It’s about:

- Sleeping soundly knowing you’re protected

- Making decisions from strength, not desperation

- Breaking the cycle of debt that traps so many people

- Creating the foundation for everything else you want financially

Once you have your emergency fund:

- Investing becomes exciting instead of scary

- Financial goals become achievable instead of fantasy

- Life’s inevitable problems become manageable instead of catastrophic

- You move from survival mode to building mode

Your Action Plan This Week

Don’t overthink this. Take action:

Today:

- Calculate your monthly essential expenses

- Determine your emergency fund target (3-6 months)

- Open a high-yield savings account if you don’t have one

This week:

- Transfer whatever you can to start ($50, $100, $500—anything!)

- Set up automatic transfer from checking on payday

- Name your savings account “Emergency Fund – Do Not Touch”

This month:

- Review spending and find $200-500 to accelerate savings

- Sell unused items and add proceeds to fund

- Hit your first milestone ($1,000)

This year:

- Build systematically to 3 months saved

- Continue to 6 months if your situation requires it

- Breathe easier knowing you’re financially secure

Twenty years from now, you won’t remember which month you hit $5,000 or how long it took to reach $15,000.

But you’ll remember the peace of mind. The security. The confidence. The freedom from financial fear.

You’ll remember the emergencies that didn’t destroy you because you were prepared. The opportunities you could seize because you weren’t desperate. The dignity of handling life’s problems without begging or borrowing.

That’s what an emergency fund gives you.

Start building yours today.

INTERESTING TOPICS

Ready to start investing after building your emergency fund?

Learn how to begin with just $100 and grow your wealth.

Want to understand the best investment strategy?

Discover index funds, the simple approach that beats most professionals.

Need to know when to save versus invest?

Read about the difference between saving and investing and how both build your financial future.

Want more financial insights delivered to you? Subscribe to our newsletter

and get weekly articles with practical strategies to grow your wealth sent straight to your inbox.

Obs: Sign up for our newsletter and receive a free Finance For Beginner eBook.

Disclaimer: This article is for educational purposes only. Diversification does not guarantee profits or protect against all losses. Consider your financial situation, risk tolerance, and investment timeline before making investment decisions.

—— End of Article ——