How to Build Emergency Fund: The Complete Step-by-Step Guide

Last updated: February 2026

It’s 2 AM and your phone rings.

Your car broke down. The transmission is shot. The repair bill is $5,000.

Your heart sinks. You have $800 in savings. You have no emergency fund.

Now you’re facing a choice: Credit card debt, family loan, or financial stress?

This is the moment emergency funds exist for.

An emergency fund isn’t boring or unnecessary. It’s the difference between a temporary setback and a financial disaster. It’s the safety net that keeps you from derailing your entire wealth-building plan.

But here’s what most people don’t understand: Having an emergency fund is useless if you don’t know HOW to build one.

You know you SHOULD have one. You know you NEED one. But how much? Where do you keep it? How fast should you build it? What counts as an emergency?

These questions paralyze most people, so they never build one at all.

In this guide, you’ll learn exactly what an emergency fund is, why it’s essential before investing, how much you actually need (the real answer, not vague), where to keep your emergency fund, how to build it step-by-step, how to avoid common mistakes, what counts as emergency vs what doesn’t, and how to maintain it once built.

By the end, you’ll have a concrete plan to build your safety net.

Let’s protect your wealth.

What is an Emergency Fund? (And Why It Matters)

An emergency fund is money set aside specifically for unexpected expenses, kept in an easily accessible account, separate from your regular spending money.

In simpler terms: Cash for unexpected bad things.

Why It Exists

Life happens:

- Car breaks down ($2,000-$8,000)

- Medical emergency ($1,000-$10,000+)

- Job loss (months of expenses)

- Home repair ($500-$5,000+)

- Family emergency (unpredictable cost)

Without emergency fund:

- You go into debt

- You derail wealth building

- You stress about finances

- You panic make bad decisions

With emergency fund:

- You cover unexpected costs

- You stay debt-free

- You keep wealth building on track

- You stay calm

The Real Impact

Scenario: Job loss without emergency fund

- Lose job

- No income coming

- Bills still due

- Can’t pay mortgage/rent

- Go into debt

- Takes years to recover

- Wealth building delayed 5+ years

Scenario: Job loss with 6-month emergency fund

- Lose job

- Bills covered for 6 months

- Time to find new job without panic

- No debt incurred

- Resume wealth building

- Crisis becomes temporary inconvenience

Difference: Years of delayed wealth building.

Why Emergency Funds Come BEFORE Investing

Critical rule: Build emergency fund BEFORE aggressive investing.

The Logic

If you invest without emergency fund:

- Emergency happens

- You need money fast

- You must sell investments

- Stock market is down 30% (Murphy’s Law)

- You lock in losses

- You can’t recover

If you have emergency fund:

- Emergency happens

- You use emergency fund

- Investments stay invested

- They keep growing

- You recover from emergency

The Priority Order

1. Minimum emergency fund ($1,000) — Start here 2. Pay off high-interest debt — Credit cards, payday loans 3. Build full emergency fund (3-6 months) — Get to goal 4. Then invest aggressively — Now you’re protected

Do NOT: Skip emergency fund to invest. This backfires.

Real Example

You with $10,000:

Wrong approach:

- Invest all $10,000 in stocks

- Emergency happens (medical bill $3,000)

- Market is down 25%

- You must sell $4,000 of investments to get $3,000

- You lock in losses

- You’re down to $7,000 and still have emergency

Right approach:

- Keep $3,000 in emergency fund

- Invest $7,000 in stocks

- Emergency happens

- You use emergency fund ($3,000)

- Investments stay invested and keep growing

- You’re protected

Difference: Hundreds or thousands in losses avoided.

How Much Do You Actually Need?

This is where most advice gets vague. Let me be specific.

The Standard Answer

Financial experts recommend: 3-6 months of expenses

But what does that mean?

The Real Calculation

Step 1: Calculate your monthly expenses

Add up ALL monthly costs:

- Rent/mortgage

- Utilities

- Food

- Insurance

- Transportation

- Phone

- Subscriptions

- Everything else

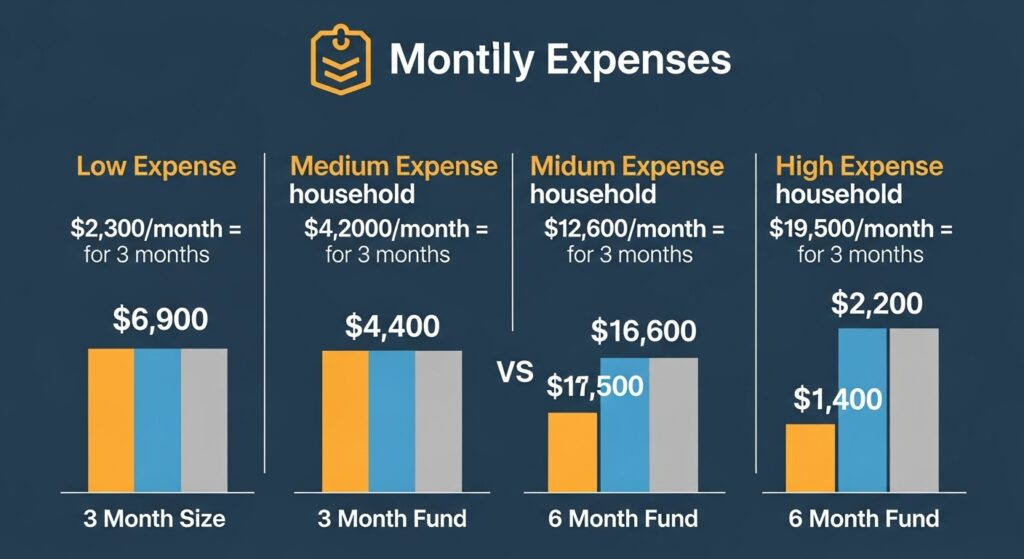

Example:

- Rent: $1,200

- Utilities: $150

- Food: $400

- Insurance: $200

- Transportation: $150

- Other: $200

- Total monthly: $2,300

Step 2: Multiply by 3-6 months

Conservative (3 months):

- $2,300 × 3 = $6,900

Recommended (6 months):

- $2,300 × 6 = $13,800

Step 3: Pick your target

Who should aim for 3 months:

- Stable, secure job

- Dual income household

- Low expenses

- Young and flexible

Who should aim for 6 months:

- Self-employed

- Single income household

- Higher expenses

- Multiple dependents

- Industry at risk of layoffs

- Older (recovery harder if job lost)

Real Numbers by Income Level

$50,000/year income:

- Monthly expenses: ~$2,500-$3,000

- 3-month fund: $7,500-$9,000

- 6-month fund: $15,000-$18,000

$75,000/year income:

- Monthly expenses: ~$3,500-$4,500

- 3-month fund: $10,500-$13,500

- 6-month fund: $21,000-$27,000

$100,000/year income:

- Monthly expenses: ~$5,000-$6,500

- 3-month fund: $15,000-$19,500

- 6-month fund: $30,000-$39,000

The Honest Truth

Most people have ZERO emergency fund.

Starting with $1,000 is better than perfect $6,900. Having $5,000 is better than having zero. Progress beats perfection.

Where to Keep Your Emergency Fund

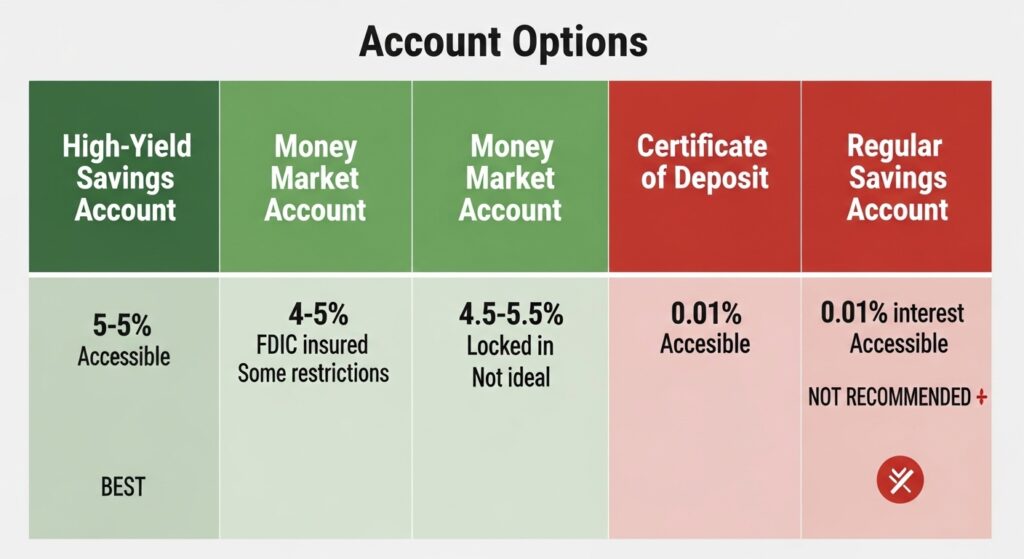

Critical rule: NOT in stocks. NOT in long-term investments. In CASH or CASH EQUIVALENT.

Option 1: High-Yield Savings Account (BEST)

What it is: Savings account with competitive interest rate

Interest rate: 4-5% annually (2026 rates)

Why it’s best:

- Completely safe (FDIC insured)

- Earns interest (beats inflation slightly)

- Accessible (withdraw anytime)

- No risk whatsoever

- No fees if you find right bank

Banks offering high-yield savings:

- Marcus by Goldman Sachs

- Ally Bank

- American Express Personal Savings

- Discover Bank

The Federal Deposit Insurance Corporation provides information about account protection and which banks offer FDIC insurance for your emergency fund safety.

Example: $10,000 at 4.5% = $450/year interest (better than 0%)

Option 2: Money Market Account

What it is: Hybrid between checking and savings

Interest rate: 4-5% annually

Pros:

- FDIC insured

- Earns interest

- Check-writing available

- More accessible than savings

Cons:

- May require higher minimum

- Limited check-writing

Option 3: Certificate of Deposit (CD)

What it is: Fixed-term savings with guaranteed rate

Interest rate: 4-5.5% annually

Pros:

- FDIC insured

- Highest interest rates

- Guaranteed return

Cons:

- Money locked in for term (3, 6, 12 months)

- Penalty if withdraw early

- Not ideal for emergency (need to access NOW)

Use for: Part of emergency fund after you exceed 3-month goal

Option 4: Regular Savings Account (NOT IDEAL)

What it is: Standard bank savings account

Interest rate: 0.01% – 0.05% (pathetic)

Pros:

- Accessible

- FDIC insured

Cons:

- Almost zero interest

- Losing money to inflation

- Only use if no other option

❌ Where NOT to Keep Emergency Fund

❌ Checking account — Too tempting to spend

❌ Stocks/investments — Not accessible, too risky

❌ Crypto — Way too volatile

❌ Under your mattress — No interest, not safe

❌ Tied up in long-term CD — Can’t access in emergency

Keep it LIQUID and SAFE.

The Complete Step-by-Step Building Plan

Exact plan to build your emergency fund.

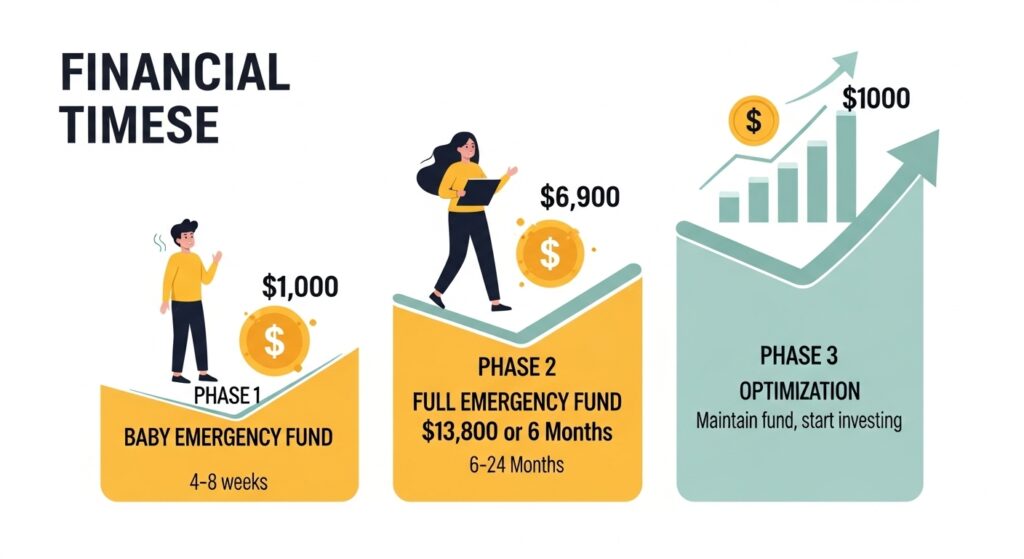

Phase 1: Baby Emergency Fund ($1,000)

Why start with $1,000:

- Covers most common emergencies

- Builds confidence

- Gives psychological boost

- Takes weeks, not months

How to build:

- Set goal: Save $1,000

- Timeline: 4-8 weeks (doable!)

- Method: Cut expenses or side income

- Place: High-yield savings account

Example:

- Current: $200 saved

- Target: $1,000

- Gap: $800

- Monthly goal: $200/month

- Timeline: 4 months

Once you hit $1,000: Celebrate! You’re protected from most emergencies.

Phase 2: Full Emergency Fund (3-6 months)

After baby fund is built:

Decision: 3 months or 6 months?

- Secure job? → 3 months ($6,900 example)

- Self-employed? → 6 months ($13,800 example)

How to build:

- Continue monthly savings

- Direct percentage of income to fund

- Example: 10% of paycheck goes to emergency fund

- Don’t touch baby fund (already safe)

Timeline:

- $1,000 baby fund already done

- Building to $6,900 (3-month goal)

- Need $5,900 more

- At $200/month: 30 months

- At $400/month: 15 months

- At $600/month: 10 months

Speed depends on income and discipline.

Phase 3: Optimization (After Fund Built)

Once you have 3-6 month fund:

Option A: Keep building to 6 months (if only at 3)

- Continue saving monthly

- Grow fund gradually

Option B: Start investing (if at 6 months)

- Emergency fund is complete

- Now invest additional money

- Dollar-cost averaging into diversified portfolio

Option C: Split approach (hybrid)

- 6 months in savings account

- Additional savings go to investments

- Best of both worlds

How Fast Should You Build It?

It depends on your situation.

Timeline by Situation

Urgent (Build in 3-6 months):

- You have zero emergency fund

- You just started job

- You’re terrified of emergency

- Action: Aggressive saving, side income

Normal (Build in 6-12 months):

- You have some savings

- Stable job

- Normal expenses

- Action: Steady monthly savings

Comfortable (Build in 12-24 months):

- You already have $3,000+

- Multiple income streams

- Can contribute slowly

- Action: Consistent monthly savings

The Math by Monthly Contribution

$1,000 baby fund target:

- $100/month: 10 months

- $200/month: 5 months

- $300/month: 3-4 months

$6,900 full fund target (3 months):

- $200/month: 35 months (3 years)

- $300/month: 23 months (2 years)

- $500/month: 14 months (1 year)

- $700/month: 10 months

$13,800 full fund target (6 months):

- $500/month: 28 months (2+ years)

- $700/month: 20 months

- $1,000/month: 14 months

Real talk: Even at $200/month, you can build full emergency fund in 3-4 years. That’s acceptable.

What Counts As an Emergency?

Clear guidelines on what IS emergency.

✅ REAL Emergencies

Medical:

- Unexpected surgery

- Emergency room visit

- Urgent care

- Prescription medications

- Dental emergency

Job/Income:

- Job loss (covered by fund)

- Unexpected furlough

- Business failure

- Disability/injury preventing work

Home:

- Major home repair (furnace, roof, plumbing)

- Sudden appliance failure (water heater)

- Structural damage

- Urgent safety issue

Car:

- Engine failure

- Transmission issue

- Accident (after insurance)

- Urgent safety repair

Family:

- Death in family (travel costs)

- Family emergency (helping relative)

- Unexpected dependent needs

What Does NOT Count As Emergency

These are NOT emergencies. Don’t use fund for these.

❌ FAKE Emergencies

Wants, not needs:

- ❌ New phone (old one still works)

- ❌ Vacation (fun but not emergency)

- ❌ New car (current one works)

- ❌ Designer clothes

- ❌ Concert tickets

- ❌ Gaming computer

Planned expenses:

- ❌ Annual car insurance

- ❌ Holiday gifts

- ❌ Back-to-school shopping

- ❌ Wedding (you’re planning it)

- ❌ Predictable expenses

Impulse purchases:

- ❌ Retail therapy

- ❌ Food cravings

- ❌ Subscription you want

- ❌ Upgrade you feel like getting

Debt payments:

- ❌ Credit card payment (use regular income)

- ❌ Loan payment (use regular income)

- ❌ Don’t use emergency fund for normal debt

Financial mistakes:

- ❌ Investment loss

- ❌ Bad decision

- ❌ Expensive habit

Rule of thumb: If you can plan for it or avoid it, it’s not emergency.

Maintaining Your Emergency Fund

Once built, how to maintain it.

Rule 1: Don’t Touch It Unless REAL Emergency

The hardest rule to follow.

Temptations you’ll face:

- “I can use it for this investment!”

- “I’ll rebuild it later”

- “This is kind of an emergency”

- “I need just $500 of it”

Don’t. Do. This.

The moment you tap it for non-emergency, it stops being emergency fund and becomes available money. You’ll keep tapping it.

Keep it sacred.

Rule 2: Replenish After Using

If you use emergency fund:

- Acknowledge the emergency was real

- Access funds you need

- Don’t feel guilty (that’s why it exists!)

- Rebuild it ASAP

Example:

- Medical emergency costs $3,000

- You had $6,900 fund

- Now have $3,900

- Rebuild to $6,900 at $300/month

- Takes 10 months to replenish

Rule 3: Review Annually

Once per year:

- Check balance

- Verify it’s still adequate

- Adjust if income changed

- Move to better rate if available

Example:

- Built 3-month fund when earning $50K

- Now earning $75K

- Expenses higher

- May need to bump to 6 months

- Update goal

Rule 4: Keep It Accessible

Verify anytime:

- Emergency fund account accessible

- Can withdraw in 1-2 business days

- Not locked in long-term CD

- Not in illiquid investments

Test it: Once per year, verify you can access it within 24-48 hours.

Common Mistakes to Avoid

Learn from others’ mistakes.

❌ Mistake 1: No Emergency Fund at All

The cost:

- Emergency happens

- Go into debt

- Years of financial stress

- Derails wealth building

Solution: Start with $1,000 today. Right now.

❌ Mistake 2: Fund Too Small

The problem:

- $500 emergency fund

- Car repair costs $2,000

- Still need to go into debt

- Fund was almost useless

Solution: Aim for at least 3 months expenses. Real protection.

❌ Mistake 3: Money in Wrong Place

The problem:

- Keep emergency fund in stocks

- Emergency happens

- Market is down 30%

- Lose money getting your money

- Defeat the purpose

Solution: High-yield savings account. Safe, accessible, earning interest.

❌ Mistake 4: Keep Tapping It for Non-Emergency

The problem:

- “Need new phone”

- Tap emergency fund

- “Rebuild it later”

- Never rebuild

- Then real emergency hits, no fund

Solution: Strict definition of emergency. Don’t tap it.

❌ Mistake 5: Never Building Beyond 1-2 Months

The problem:

- $2,000 fund

- Job loss (3 months to find new job)

- Fund gone in 2 months

- Still unemployed, no money

- Financial crisis

Solution: Build to full 3-6 months. Takes time but critical.

❌ Mistake 6: Ignoring It After Building

The problem:

- Build $10,000 fund in 2020

- Never check it again

- Inflation happens

- $10,000 is now worth less

- Needs adjustment

Solution: Review annually, adjust as needed.

Frequently Asked Questions – FAQ 👈

Q: Should I build emergency fund or pay off debt first?

A: Build $1,000 baby fund first. Then pay off high-interest debt (credit cards). Then build full emergency fund. Then invest. Order matters.

Q: What if I don’t have extra money to save?

A: Everyone has money to redirect. Cut one subscription ($15/month = $180/year toward fund). Pack lunch instead of buying ($10/day = $2,000/year). Small changes add up.

Q: Can I invest my emergency fund to make it grow?

A: No. Emergency fund is NOT investment. Keep it safe and accessible. Invest money AFTER emergency fund is full. Separate purposes.

Q: How often should I add to emergency fund?

A: Every paycheck. Automatic transfer from checking to savings account. Same day you get paid. Automation removes the decision.

Q: What if I use emergency fund but don’t refill it?

A: You’re vulnerable again. Rebuild it to priority #1. Don’t invest extra money until replenished.

Q: Is 6 months really necessary?

A: For most people, 3 months is adequate. 6 months if self-employed, at risk of job loss, or multiple dependents.

Q: Should emergency fund earn interest?

A: Yes. High-yield savings at 4-5% beats inflation. Every bit helps.

Q: What about emergency line of credit instead?

A: Bad idea. Relies on credit being available when you need it. During crisis, credit dries up. Cash emergency fund is certain.

🎥 BONUS

Want to see real examples of emergency fund calculations and step-by-step building process?

This video shows people building funds from zero and managing them:

FINAL THOUGTS: Your Emergency Fund is Your Foundation

Here’s what most people don’t realize: Your emergency fund isn’t boring or unnecessary. It’s actually your MOST IMPORTANT financial tool.

Why? Because it protects everything else.

Without it, one bad emergency derails your entire wealth-building plan. You go into debt. You have to sell investments at losses. You stress about finances. You give up on your goals.

With it, emergencies become temporary inconveniences instead of financial disasters.

The wealthy all have emergency funds. Not because they’re paranoid. But because they understand that protection comes first, growth comes second.

Your path to wealth doesn’t start with investing. It starts with this: A fully-funded emergency fund.

Once you have that, THEN you invest aggressively. THEN you build serious wealth. THEN you sleep peacefully knowing you’re protected.

Your action this week:

- Calculate your monthly expenses

- Multiply by 3 (goal: 3-month fund)

- Open high-yield savings account

- Set up automatic transfer ($200/month minimum)

- Stop checking it unless real emergency

That’s it. You just started building your financial fortress.

The Consumer Financial Protection Bureau provides guidance on savings accounts, managing finances during emergencies, and building financial security.

INTERESTING TOPICS

Ready to learn how to invest aggressively once your emergency fund is complete?

Want to understand how market crashes won’t derail you because you have this fund?

Need to discover how to avoid get-rich-quick schemes and focus on real wealth building instead?

Want more financial insights delivered to you? Subscribe to our newsletter

and get weekly articles with practical strategies to grow your wealth sent straight to your inbox.

Obs: Sign up for our newsletter and receive a free Finance For Beginner eBook.

Disclaimer: This article is for educational purposes only. Diversification does not guarantee profits or protect against all losses. Consider your financial situation, risk tolerance, and investment timeline before making investment decisions.

—— End of Article ——