How to Choose Your First Investment: A Decision Framework

Last updated: January 2026

You’ve learned the theory.

You understand compound interest and why time matters. You know saving versus investing. You’ve studied stocks and bonds. You know about index funds, ETFs, and diversification.

Now comes the paralyzing moment: Which one do I actually buy?

You open your brokerage account. You see thousands of options. Stocks, bonds, ETFs, mutual funds, REITs, options, crypto, real estate—the choices are endless. Your analysis paralysis kicks in. You start second-guessing everything.

“What if I choose wrong?” “What if I miss the perfect investment?” “What if I buy at the top right before a crash?” “What if there’s something better?”

And so you do nothing. You wait for the “perfect” investment. You research endlessly. Weeks turn into months. You miss out on years of wealth-building growth.

Here’s the truth: Your first investment doesn’t have to be perfect. It just has to be started.

The difference between choosing a “good enough” investment and waiting forever for the “perfect” one? That’s decades of compound growth. That’s hundreds of thousands of dollars.

In this guide, you’ll learn the exact decision-making framework successful investors use, how to evaluate investments rationally instead of emotionally, which investment types match your specific situation, how to avoid common beginner mistakes, and most importantly—how to stop overthinking and start investing today.

By the end, you’ll have a clear roadmap to choose your first investment with confidence.

Let’s get you started.

Table of Contents

- The Biggest Beginner Mistake: Analysis Paralysis

- The Investment Decision Framework (Step-by-Step)

- Step 1: Know Your Numbers (Financial Foundation)

- Step 2: Define Your Goal (What Are You Investing For?)

- Step 3: Determine Your Timeline (When Do You Need the Money?)

- Step 4: Assess Your Risk Tolerance (Can You Handle Volatility?)

- Step 5: Choose Your Investment Type (Stocks, Bonds, or Both?)

- Step 6: Select Your Vehicle (Individual Stocks vs ETFs vs Mutual Funds)

- Investment Options for Different Goals

- Red Flags: Investments to Avoid

- The First Investment Action Plan

- Frequently Asked Questions

- Your Investment Decision Made

The Biggest Beginner Mistake: Analysis Paralysis

Before we build your decision framework, let’s talk about what stops most people from investing at all.

The Paralysis Trap

You know you SHOULD invest. You know compound interest works. You’ve saved money. Everything points to “invest now.”

But then…

You start researching. You read articles. You watch YouTube videos. You compare options. You read reviews. You check ratings. You look for “expert picks.” You wonder if NOW is the right time to invest or if you should wait for a crash.

Days pass. Weeks pass. Months pass.

By the time you finally make a decision, you’ve lost months or YEARS of growth. And ironically, you probably would have gotten similar results with ANY reasonable choice you made back then.

The Opportunity Cost is Real

Scenario: $10,000 Investment Starting Today

Option A: Invest immediately in a simple S&P 500 index fund

- Year 1: $11,000 (10% return)

- Year 5: $16,105

- Year 10: $25,937

Option B: Spend 6 months researching, then invest the same $10,000

- Year 0-0.5: $0 growth (researching)

- Year 0.5-1.5: $11,000 (10% return)

- Year 5.5: $16,105

- Year 10.5: $25,937

- Net loss from waiting: $2,594 in compound growth

And you probably chose a WORSE investment than just the simple index fund after all that research.

The Perfect Investment Doesn’t Exist

Here’s what you need to understand: There is no perfect investment.

Every investment has:

- Pros and cons

- Risk and reward trade-offs

- Times it outperforms and times it underperforms

- Uncertainty about the future

Waiting for perfection is like refusing to eat until you find the perfect meal. You’ll starve.

A “good enough” investment started today beats a “perfect” investment started in six months.

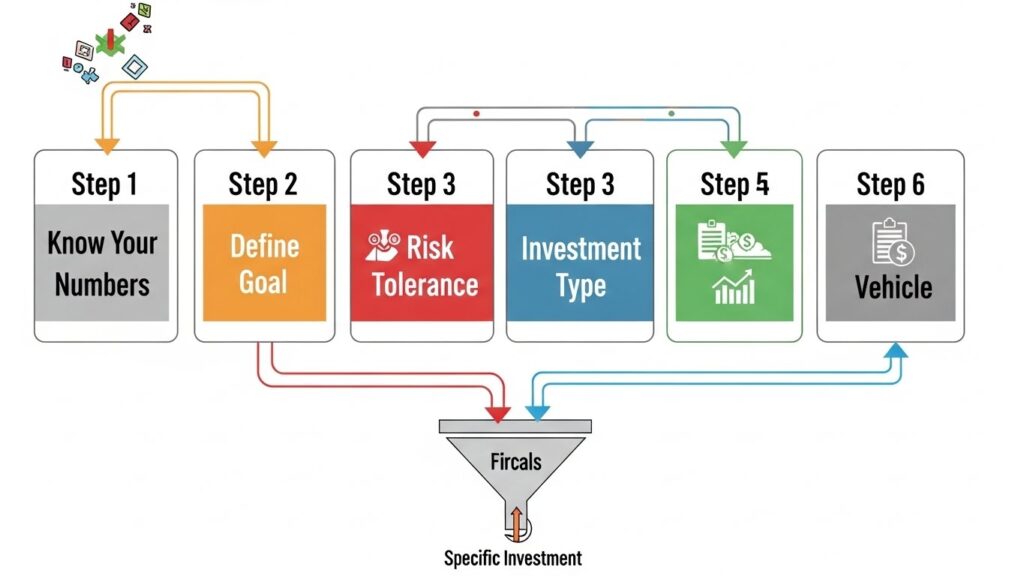

The Investment Decision Framework (Step-by-Step)

Instead of getting lost in infinite options, use this framework. It narrows down thousands of choices to a few specific options that match YOUR situation.

The Framework has 6 steps:

- Know Your Numbers (Financial Foundation)

- Define Your Goal (What Are You Investing For?)

- Determine Your Timeline (When Do You Need the Money?)

- Assess Your Risk Tolerance (Can You Handle Volatility?)

- Choose Your Investment Type (Stocks, Bonds, or Both?)

- Select Your Vehicle (How to Buy It)

Follow these steps in order. Each one eliminates bad options and narrows your choices.

Step 1: Know Your Numbers (Financial Foundation)

Before you invest a single dollar, make sure your financial foundation is solid.

The Foundation Checklist

Do you have an emergency fund?

- 3-6 months of expenses in a savings account

- Not invested (too risky for emergency money)

- Liquid and accessible

- If NO: Build this first before investing

Do you have high-interest debt?

- Credit card debt? (Usually 18-24% interest)

- Car loans? (Usually 5-8% interest)

- Personal loans? (Usually 8-15% interest)

- If YES to credit cards: Pay these down before investing

- If YES to other debt: You can invest while paying off (interest rates are lower)

Do you have retirement accounts available?

- Employer 401(k)? (Start here if employer matches!)

- Ability to open Roth IRA? (Tax-advantaged growth)

- These should be your FIRST investments

Do you have stable income?

- Steady job or business?

- Can you continue investing monthly?

- If income is unstable: Be more conservative

Why This Matters

If you invest $10,000 while carrying $10,000 in credit card debt at 20% interest:

- You’re paying 20% to the credit card

- You’re earning 10% on the investment

- Net: You’re losing 10% annually

It makes zero sense mathematically.

Focus on:

- Emergency fund ($1,000-3,000 minimum to start)

- Pay off high-interest debt

- Then invest aggressively

Step 2: Define Your Goal (What Are You Investing For?)

Different goals need different strategies.

Common Investment Goals

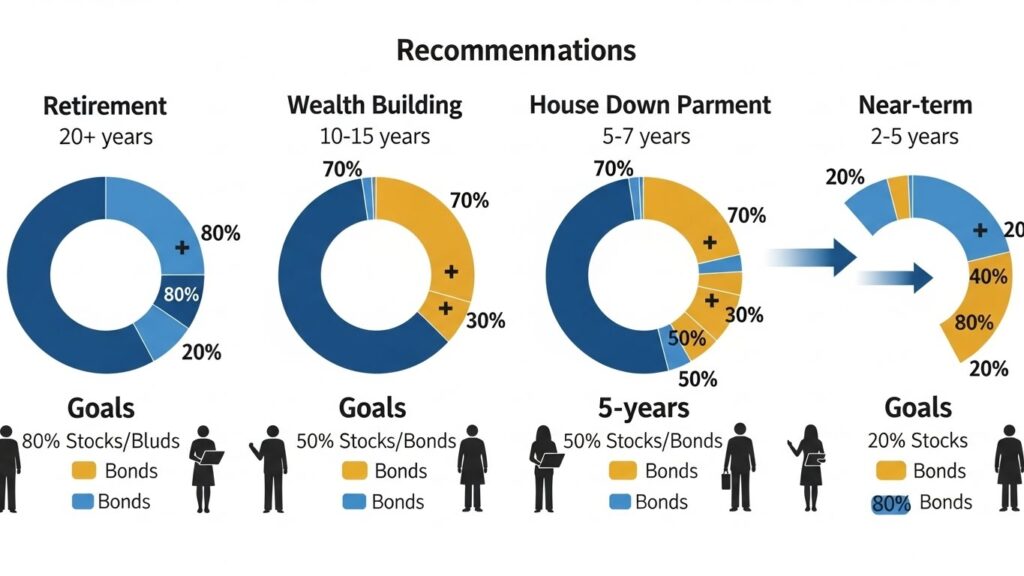

Goal 1: Retirement (20+ years away)

- Strategy: Aggressive (more stocks, less bonds)

- Vehicle: 401(k), Roth IRA, then taxable account

- Focus: Maximum long-term growth

- Example: 80% stocks / 20% bonds

Goal 2: Wealth Building (10-20 years)

- Strategy: Balanced (stocks and bonds mix)

- Vehicle: Index funds, ETFs, diversified portfolio

- Focus: Growth with some stability

- Example: 70% stocks / 30% bonds

Goal 3: Down Payment on House (5-10 years)

- Strategy: Moderate (some stocks, some bonds)

- Vehicle: Mix of stocks and bonds, not too risky

- Focus: Steady growth, avoid big crashes near goal

- Example: 60% stocks / 40% bonds

Goal 4: Major Purchase (2-5 years)

- Strategy: Conservative (mostly bonds)

- Vehicle: Bonds, bond funds, short-term CDs

- Focus: Capital preservation

- Example: 30% stocks / 70% bonds

Goal 5: Short-term Income (need money this year)

- Strategy: Ultra-safe (mostly cash, some bonds)

- Vehicle: High-yield savings, short-term bonds

- Focus: Liquidity and safety

- Example: 0% stocks / 100% bonds + cash

Key Questions

What are you investing FOR? Write it down. Be specific. “Build retirement wealth” is vague. “Have $500,000 for retirement in 30 years” is clear.

When will you need this money? This determines your timeline (next step).

Can you afford to lose money and wait? If you can’t wait years, choose conservative. If you can wait decades, choose aggressive.

Step 3: Determine Your Timeline (When Do You Need the Money?)

Timeline is one of the most important determinants of investment choice.

Timeline Categories

Long-Term (10+ years)

- Retirement (20+ years away)

- Wealth building with decades

- Strategy: Aggressive, high stock allocation

- Why: Time to recover from crashes, compound growth matters most

- Best vehicles: Stock index funds, individual growth stocks

Medium-Term (5-10 years)

- Down payment on house

- Major life goals

- Strategy: Balanced, 60/40 or 70/30

- Why: Need some protection but growth still important

- Best vehicles: Mixed ETFs, balanced funds

Short-Term (2-5 years)

- Car purchase

- Vacation savings

- Strategy: Conservative, mostly bonds

- Why: Can’t afford big crash right before you need it

- Best vehicles: Bond funds, short-term bonds, CDs

Very Short-Term (under 2 years)

- Down payment for house (coming soon)

- Emergency situation

- Strategy: Ultra-safe, no stocks

- Why: You’ll need the money soon, can’t recover from crash

- Best vehicles: High-yield savings, money market, Treasury bills

The Time Rule

Safe Rule of Thumb:

- 10+ years until you need money? Can take stock risk

- 5-10 years? Reduce stock exposure significantly

- Under 5 years? Mostly bonds and cash

- Under 2 years? 100% safe, no stock market exposure

This prevents the tragic scenario: You invested in stocks, market crashed 30%, and NOW you need the money for your house down payment. You lock in losses.

Step 4: Assess Your Risk Tolerance (Can You Handle Volatility?)

Risk tolerance is psychological. It’s how much portfolio swings stress you out.

The Real Risk Tolerance Test

Imagine your portfolio drops 30% in a market crash. What do you do?

A) Panic and sell everything (Low risk tolerance)

- You can’t handle volatility

- You need mostly bonds

- Conservative allocation

B) Stress but stay invested (Medium risk tolerance)

- You can handle some swings

- You need balanced portfolio

- Moderate allocation

C) Stay calm and buy more (High risk tolerance)

- You love opportunities

- You can handle aggressive portfolio

- You see crashes as buying opportunities

D) Check price once a year (Very high risk tolerance)

- You’re not emotional about money

- Maximum stocks okay

- Aggressive allocation

Why This Matters

The BEST investment is the one you’ll actually stick with.

A perfect aggressive portfolio you panic-sell in a crash is WORSE than a boring balanced portfolio you hold forever.

Because growth doesn’t work if you’re not invested.

Finding Your TRUE Risk Tolerance

Answer honestly:

- In a market crash, would you lose sleep?

- Would you want to sell and “get to safety”?

- Or would you see it as a buying opportunity?

- How much volatility stresses you out?

Be honest. Not what you THINK you should tolerate, but what you ACTUALLY would tolerate.

Step 5: Choose Your Investment Type (Stocks, Bonds, or Both?)

Based on your goal, timeline, and risk tolerance, decide your asset allocation.

The Simple Framework

Timeline 10+ years + High risk tolerance → Aggressive: 80-90% stocks, 10-20% bonds

Timeline 5-10 years + Medium risk tolerance → Balanced: 60-70% stocks, 30-40% bonds

Timeline 2-5 years + Low risk tolerance → Conservative: 30-50% stocks, 50-70% bonds

Timeline under 2 years + Very low risk tolerance → Ultra-safe: 0-10% stocks, 90-100% bonds/cash

How to Choose Between Stocks and Bonds

Choose MORE STOCKS if:

- You have 10+ year timeline

- You have high risk tolerance

- Market crashes won’t make you panic-sell

- You can buy during crashes with dollar-cost averaging

- You want maximum long-term growth

Choose MORE BONDS if:

- You have short-term goals (under 5 years)

- You have low risk tolerance

- Market crashes stress you out

- You need stable income

- You’re near retirement

Choose BOTH (balanced) if:

- Most people fit here

- You want growth without extreme volatility

- You want to sleep at night

- You have moderate timeline and risk tolerance

Step 6: Select Your Vehicle (How to Buy It)

Now you know WHAT to buy (stocks/bonds mix). Next: HOW to buy it.

Investment Vehicles Compared

Individual Stocks

- Pros: Full control, potential high returns, interesting

- Cons: Requires research, requires discipline, higher risk

- Best for: Experienced investors, long-term holders

- For beginners: Not recommended as first investment

Index Funds / ETFs

- Pros: Diversified, low-cost, simple, passive

- Cons: Less exciting, limited control

- Best for: Beginners, long-term investors, lazy portfolios

- For beginners: HIGHLY RECOMMENDED

Mutual Funds

- Pros: Professional management, diversified

- Cons: Higher fees, tax inefficient, underperform

- Best for: People who want active management

- For beginners: ETFs better

Bonds (Individual or ETFs)

- Pros: Predictable income, lower volatility

- Cons: Lower returns, complex if individual

- Best for: Conservative investors

- For beginners: Bond ETFs easiest

REITs

- Pros: Real estate exposure, monthly income possible

- Cons: Higher volatility, tax complexity

- Best for: Experienced investors

- For beginners: Avoid for now

Target-Date Funds

- Pros: Auto-adjusts allocation as you age, simple

- Cons: One-size-fits-all approach

- Best for: Lazy investors, 401(k) default

- For beginners: Good starting point

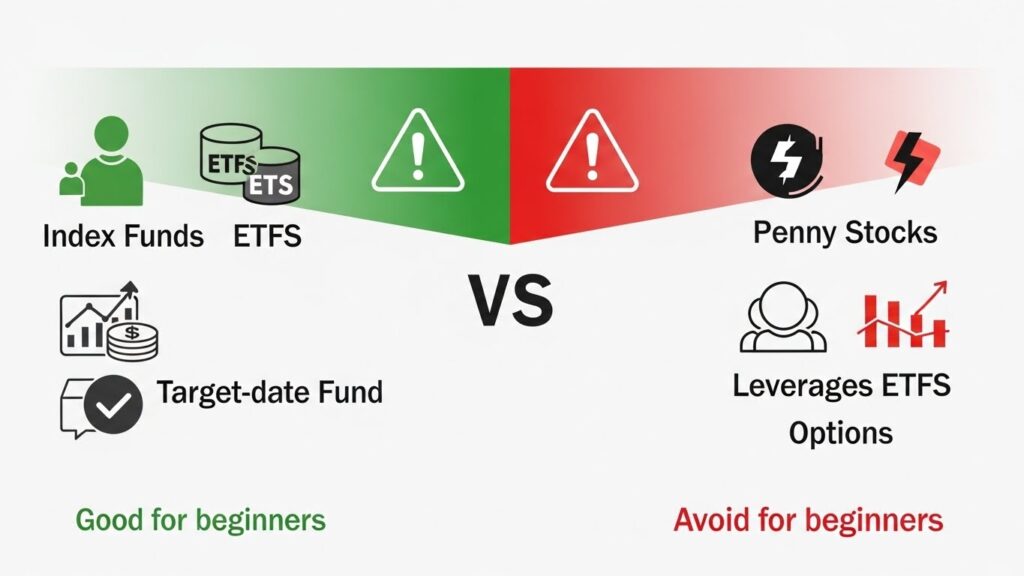

The Beginner-Friendly Choice

For your FIRST investment, choose:

✅ Index Fund or ETF

- Simple: One investment covers hundreds of companies

- Cheap: Expense ratio 0.03-0.20% annually

- Effective: Beats most professionals

- Passive: Set and forget

- Best vehicles: VTI, VOO, VTSAX (for stocks) | BND, AGG, VBTLX (for bonds)

For detailed information about different investment account types and their tax advantages, the SEC provides comprehensive beginner resources.

This is NOT boring. This is SMART.

The most successful long-term investors often use simple index funds. It’s not lack of sophistication; it’s the opposite—understanding that simplicity beats complexity.

Investment Options for Different Goals

If Your Goal is Retirement (20+ years)

Allocation: 80% stocks / 20% bonds

Best first investment:

- Max out employer 401(k) first (free money matching)

- Then Roth IRA (tax-free growth)

- Then taxable account

Learn more about retirement account contribution limits, eligibility requirements, and strategic investing through official IRS resources.

Specific picks:

- VTI or VOO (total market or S&P 500 index)

- Dividend growth stocks (optional, for income focus)

- BND for bonds portion

Why: Maximum time for wealth building through compound interest, can weather crashes

If Your Goal is Wealth Building (10-15 years)

Allocation: 70% stocks / 30% bonds

Best first investment:

- Roth IRA (limit $7,000/year, tax-free)

- Then taxable brokerage account

Specific picks:

- VTI (overall market)

- AGG or BND (bonds)

- Or 70/30 portfolio in single target-date fund

Why: Good balance of growth and stability, sustainable long-term

If Your Goal is House Down Payment (5-7 years)

Allocation: 50% stocks / 50% bonds

Best first investment:

- 529 plan (if for education)

- High-yield savings (for safety)

- Conservative index portfolio

Specific picks:

- 60/40 ETF portfolio

- Mix of stock and bond ETFs

- Or balanced target-date fund

Why: Can’t afford big crash right before purchase, need stability with some diversification

If Your Goal is Near-Term (2-5 years)

Allocation: 20% stocks / 80% bonds

Best first investment:

- High-yield savings account

- Short-term bond funds

- Treasury bills

Specific picks:

- Avoid stocks

- BND or AGG (bond ETFs)

- Treasury bonds

- High-yield savings (not investment, but safe)

Why: Money needed soon, crashes are unacceptable

Red Flags: Investments to Avoid as Your First Investment

AVOID These as Your First Pick

1. Individual Stocks (Especially Trendy Ones)

- “Get rich quick” tech stocks

- Crypto

- Meme stocks

- Penny stocks

- Why avoid: High risk, requires extensive research, easy to panic-sell

2. Leveraged or Inverse ETFs

- 3x leveraged stock ETFs

- Inverse (short) ETFs

- Why avoid: Designed for short-term trading, not investing, decay over time

3. Options and Derivatives

- Call options, put options

- Spreads

- Why avoid: Requires expertise, high risk of total loss

4. Actively Managed Mutual Funds

- High fees (1%+ annually)

- Underperform passive index funds

- Why avoid: Expensive and ineffective

5. Penny Stocks

- Under $5 stocks

- Low-volume trading

- Why avoid: High fraud risk, manipulation, illiquid

6. Cryptocurrencies

- Bitcoin, Ethereum, altcoins

- Why avoid: Extremely volatile, speculative, not correlated to anything, not suitable for beginners building wealth

7. Anything You Don’t Understand

- “Exotic” investments

- Structured products

- Derivatives

- Why avoid: If you can’t explain it, don’t buy it

The First Investment Action Plan

Week 1: Decision Making

Day 1: Assess Your Financial Foundation

- Do you have emergency fund? (Yes/No)

- Do you have high-interest debt? (Yes/No)

- What’s your main goal? (Write it down)

Day 2: Determine Your Timeline

- When will you need this money?

- 10+ years? 5-10 years? 2-5 years? Under 2 years?

Day 3: Assess Risk Tolerance

- Market drops 30%, what do you do?

- How much volatility can you handle?

- Aggressive, moderate, or conservative?

Day 4: Choose Your Allocation

- Based on timeline and risk tolerance

- What % stocks vs bonds?

- Write it down

Day 5: Choose Your Vehicle

- Decide: ETF, index fund, or target-date fund?

- Decide: Roth IRA, 401(k), or taxable account?

- Research lowest-cost options

Week 2: Take Action

Day 1: Open Account

- Brokerage account (Fidelity, Schwab, Vanguard)

- Or 401(k) / Roth IRA (if eligible)

Day 2: Fund Account

- Link bank account

- Transfer money ($100, $1,000, whatever you have)

Day 3: Make Your Purchase

- Search for your chosen index fund

- Buy your chosen allocation

- Enable dollar-cost averaging (monthly investing)

Day 4: Enable Automatic Investing

- Set up monthly investment (same day each month)

- $100, $200, $500—whatever you can afford

- Automate it

Day 5: Set and Forget

- Don’t check daily

- Quarterly is fine

- Trust the compound interest

Your Investment Decision Made

You now have a decision framework. You know your numbers. You’ve defined your goal.

You understand your timeline and risk tolerance. You’ve chosen your allocation.

The hardest part is done. The decision is made.

Now comes the easy part: Take action.

Here’s What Happens Next

Week 1: Open account, fund it Week 2: Make first purchase Month 2+: Set up automatic monthly investing Year 1: Check quarterly, don’t overthink Year 5: Rebalance once annually Year 10+: Watch compound interest create wealth

That’s literally it.

The Only Thing You Can Get “Wrong”

The only way you truly fail is by not starting.

Perfect investors who never start build $0. Average investors who start and stay consistent build substantial wealth.

The difference between millionaires and non-millionaires isn’t usually intelligence or luck. It’s starting early and staying consistent.

You now have everything you need to start.

Frequently Asked Questions – FAQ 👈

Q: What if I choose the wrong investment?

A: For broad market index funds, there’s no really “wrong” choice. VOO and VTI are nearly identical long-term. The difference between “right” and “close” is minimal. Starting is more important than picking perfectly.

Q: What if market crashes right after I invest?

A: Perfect. You buy more shares at lower prices through dollar-cost averaging. Market crashes are opportunities for long-term investors, not disasters.

Q: Should I wait for the market to crash before investing?

A: No. You can’t time the market. History shows “worst time to invest” was often followed by massive gains within months. Time in market beats timing the market.

Q: How much should my first investment be?

A: Any amount works. Start with $100 if that’s all you have. Many brokers now have $0 minimums and allow fractional shares. The amount matters less than starting.

Q: Should I invest in individual stocks or index funds?

A: As your FIRST investment, choose index funds. Master the basics first. Individual stock picking comes later (if ever).

Q: What about taxes on my investment?

A: That’s why you use tax-advantaged accounts first (401k, Roth IRA). Contribute max allowed, THEN use taxable account. This minimizes taxes.

Q: Can I change my investment later?

A: Yes. Your first choice isn’t permanent. As you learn more, your situation changes, or goals shift, adjust. Flexibility is built in.

Q: What if I’m scared to invest?

A: That’s normal. Everyone is. The fear of doing nothing (missing decades of compound interest) should exceed fear of investing. Take action anyway.

BONUS

Want to see a real-world example of someone applying this decision framework to choose their first investment?

This video walks through the exact steps and decisions:

INTERESTING TOPICS: Your First Investment is Just the Beginning

Here’s what most people get wrong about choosing their first investment: They think it has to be PERFECT.

It doesn’t.

Your first investment will probably not be the “best” possible choice. There will always be better options in hindsight. There will always be investments that outperform yours. There will always be second-guessing.

But here’s what matters: Your first investment is the one that COMPOUNDS.

The difference between the investor who chose a “good enough” S&P 500 index fund in 2000 and the investor who waited for the “perfect” investment? The first investor has hundreds of thousands more dollars today.

The Real Secret

The secret to wealth isn’t picking the perfect investment. It’s understanding that:

- Starting beats waiting — A mediocre investment started today beats a perfect investment started in six months

- Consistency beats perfection — Monthly investing beats trying to time the market

- Time beats timing — 20 years of average returns beats trying to pick winners

- Compound interest beats everything — Give it decades and math does the work

Your first investment will teach you more than any article or course. It will make investing real. It will show you that compound interest actually works. It will prove that crashes are temporary and opportunities are permanent.

Your Action This Week

Stop reading. Start doing.

Monday: Assess your financial foundation (emergency fund, high-interest debt) Tuesday: Define your goal and timeline Wednesday: Determine your risk tolerance (honestly) Thursday: Choose your allocation (stocks/bonds mix) Friday: Open your brokerage account Saturday: Fund it and make your first purchase Sunday: Set up automatic monthly investing

That’s it. Your investment journey begins.

It doesn’t have to be perfect. It just has to start.

And you now have everything you need to do exactly that.

INTERESTING TOPICS

Ready to understand compound interest → how time multiplies your returns?

Want to discover dollar-cost averaging → how to have your investment strategy systematic?

Need to learn how to diversify → after choosing your first investment?

Want more financial insights delivered to you? Subscribe to our newsletter

and get weekly articles with practical strategies to grow your wealth sent straight to your inbox.

Obs: Sign up for our newsletter and receive a free Finance For Beginner eBook.

Disclaimer: This article is for educational purposes only. Diversification does not guarantee profits or protect against all losses. Consider your financial situation, risk tolerance, and investment timeline before making investment decisions.

—— End of Article ——