How to Invest for Retirement in Your 20s and 30s

(Complete Guide)

Last updated: January 2026

Retirement feels impossibly far away when you’re in your 20s or 30s. You’re focused on today—paying student loans, building your career, maybe buying a house. Saving for something 30-40 years in the future seems abstract, even pointless.

But here’s what most young people don’t realize: the decisions you make about retirement in your 20s and 30s will determine whether you retire comfortably at 65, struggle financially until 75, or never retire at all.

The difference between starting at age 25 versus age 35 isn’t just 10 years—it’s potentially hundreds of thousands of dollars in lost compound growth. Starting early doesn’t just give you more time; it gives your money exponentially more time to multiply.

Yet only 40% of millennials are saving for retirement, and those who are often make critical mistakes that cost them decades of growth. They invest too conservatively, miss employer matches, choose the wrong accounts, or simply don’t invest enough.

In this guide, you’ll learn exactly how to invest for retirement in your 20s and 30s, including how much to save at each age, which accounts to prioritize, what to invest in, how to balance retirement with other goals, and the costly mistakes that sabotage young investors. By the end, you’ll have a complete retirement investment strategy tailored to your decade of life.

Let’s build your retirement wealth while you still have time on your side.

Why Your 20s and 30s Are Critical for Retirement

Time is your single greatest advantage as a young investor.

Here’s why starting early is absolutely crucial:

The Power of Compound Interest Over Decades

Compound interest is the eighth wonder of the world—and it requires time to work its magic.

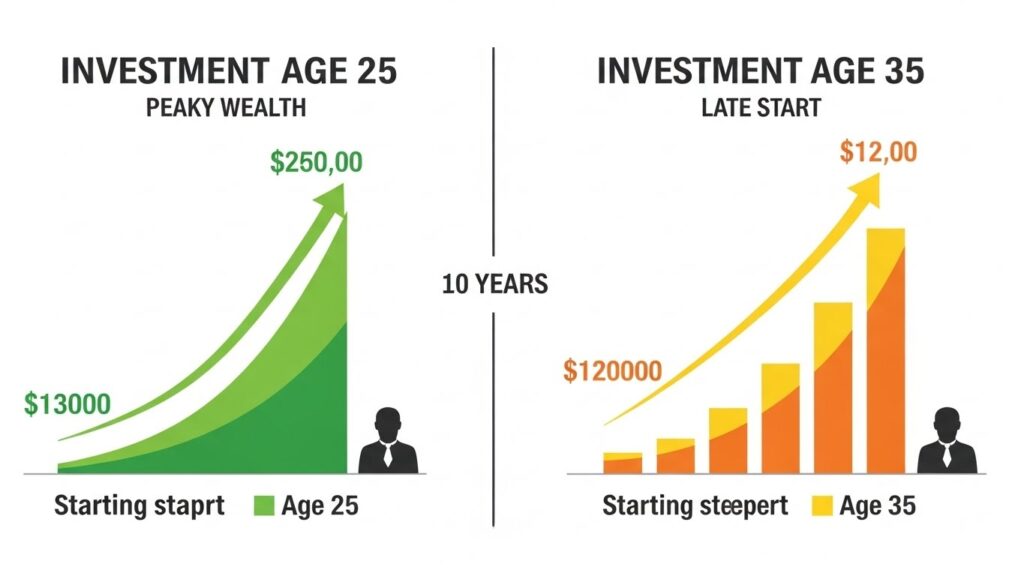

Example: Starting at 25 vs 35

Investor A (starts at 25):

- Invests $300/month for 10 years (ages 25-35)

- Then stops completely

- Total invested: $36,000

- At age 65 (8% return): $472,000

Investor B (starts at 35):

- Invests $300/month for 30 years (ages 35-65)

- Never stops

- Total invested: $108,000

- At age 65 (8% return): $446,000

Investor A invested $72,000 LESS but has $26,000 MORE at retirement!

That’s the power of starting 10 years earlier.

The 10-Year Difference Changes Everything

$200/month invested at 8% annual return:

| Starting Age | Years Invested | Total Contributed | Value at 65 | |

|---|---|---|---|---|

| Age 25 | 40 years | $96,000 | $622,000 | 💰 |

| Age 30 | 35 years | $84,000 | $366,000 | ✅ |

| Age 35 | 30 years | $72,000 | $298,000 | 😐 |

| Age 40 | 25 years | $60,000 | $182,000 | 😬 |

| Age 45 | 20 years | $48,000 | $111,000 | 😰 |

Starting at 25 vs 35 = $324,000 more with just $12,000 extra invested!

Every year you wait costs you tens of thousands in future wealth.

You Can Afford to Take More Risk

In your 20s and 30s, market crashes are opportunities, not disasters:

Scenario: Market crashes 40% when you’re 28

- You’ve only invested $10,000-20,000

- Your loss: $4,000-8,000

- You have 35+ years to recover

- You continue buying at low prices

- By retirement, that crash is invisible on your chart

Same crash at age 60:

- You’ve invested $500,000

- Your loss: $200,000

- You have 5-7 years to recover

- You might need to delay retirement

- Much more painful

Youth = time to recover = ability to invest aggressively = higher returns

You Have Fewer Financial Obligations (Usually)

Most people in their 20s-30s:

- No or few children yet

- Lower living expenses

- More flexibility with career moves

- Can live more frugally if needed

This is the time to invest aggressively before:

- Mortgages

- Kids’ expenses

- Aging parents

- Higher lifestyle costs

It gets harder to save later, not easier.

How Much Should You Save for Retirement in Your 20s vs 30s?

The amount you should save depends on your age, income, and goals. Here are realistic targets:

The General Rule: 15% of Gross Income

Standard recommendation: Save 15% of your gross income for retirement

Examples:

- Income $40,000: Save $6,000/year ($500/month)

- Income $60,000: Save $9,000/year ($750/month)

- Income $80,000: Save $12,000/year ($1,000/month)

This assumes:

- Starting in mid-20s

- Retiring at 65-67

- Maintaining similar lifestyle in retirement

Financial advisors and retirement planning experts widely recommend this percentage as a baseline for comfortable retirement.

In Your 20s: Minimum 10-15%

Reality check: Early 20s is hardest financially

- Lower income

- Student loans

- Building emergency fund

- Maybe still living with parents or roommates

Realistic targets:

Ages 20-24:

- Minimum: 10% of income

- Ideal: 15% if possible

- Focus: Get employer match, build emergency fund

Ages 25-29:

- Minimum: 12-15%

- Ideal: 15-20% as income grows

- Focus: Max out employer match, increase Roth IRA

Why lower is okay early:

- You have time to compensate later

- Other priorities compete (debt, emergency fund)

- Income typically grows through 20s

BUT: Never skip employer match—that’s free money!

In Your 30s: Aim for 15-20%

Reality: 30s are prime earning and saving years

- Income higher than 20s

- Career more established

- Maybe settled into housing

- But family costs may begin

Realistic targets:

Ages 30-34:

- Minimum: 15%

- Ideal: 15-20%

- Focus: Increase contributions as income grows, max out accounts

Ages 35-39:

- Minimum: 15-20%

- Ideal: 20-25% if kids allow

- Focus: Maximize tax-advantaged accounts, catch-up for late start

Why more in 30s:

- Higher income means higher savings capacity

- Time to retirement shrinking

- Need to compensate if you started late

- Last decade before savings gets much harder (40s with kids)

The “Age-Based” Milestone Method

By age 30: Have 1x your annual salary saved

- Example: $50,000 salary = $50,000 saved

By age 35: Have 2x your annual salary saved

- Example: $60,000 salary = $120,000 saved

By age 40: Have 3x your annual salary saved

- Example: $70,000 salary = $210,000 saved

Behind? Don’t panic—adjust going forward:

- Increase savings rate now

- You can catch up with higher contributions

- Better late than never

If You Started Late (Mid-30s)

Didn’t save in your 20s? You need to increase savings:

Standard if started at 25: 15% for 40 years = comfortable retirement

Starting at 35: Need 18-22% for 30 years to catch up

Example:

- Age 35, $60,000 income

- Save $900-1,100/month (18-22%)

- By 65: Similar retirement as someone who started at 25 saving 15%

It’s harder but absolutely doable.

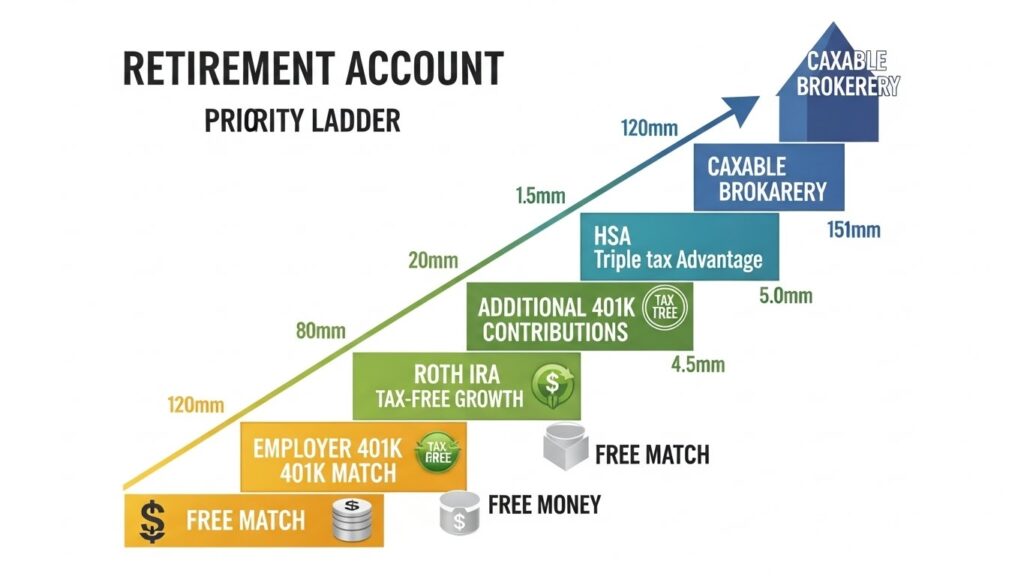

The Best Retirement Accounts for Young Investors

Not all retirement accounts are equal. Here’s the priority order:

Priority 1: Employer 401(k) (Up to Match)

ALWAYS get the full employer match first

What it is:

- Employer-sponsored retirement account

- You contribute pre-tax (lowers current taxes)

- Money grows tax-deferred

- Employer often matches 3-6% of contributions

Why it’s #1 priority:

- Employer match = instant 100% return!

- Free money you can’t get anywhere else

- Would you turn down a 50-100% raise? That’s what skipping match is!

Example:

- You make $50,000

- Employer matches 50% up to 6% of salary

- You contribute $3,000 (6%)

- Employer adds $1,500 (50% of your 6%)

- Instant $1,500 profit before any growth!

Minimum contribution: Whatever gets full match (usually 3-6% of salary)

Priority 2: Roth IRA (Max It Out)

After getting employer match, max out Roth IRA

What it is:

- Individual retirement account

- You contribute after-tax money

- Growth is completely tax-free

- Withdrawals in retirement are tax-free

Contribution limits (2024):

- $7,000/year if under 50

- $8,000/year if 50+

The IRS provides updated contribution limits and eligibility requirements for Roth IRAs each year.

Why it’s perfect for young investors:

- You’re likely in lower tax bracket now than retirement

- Decades of tax-free growth

- No required minimum distributions

- Can withdraw contributions (not earnings) anytime without penalty

Example:

- Age 25, contribute $7,000/year for 40 years

- 8% average return

- Total contributed: $280,000

- Value at 65: $1,953,000

- All $1.67 million in growth is TAX-FREE!

This is the single best account for young people.

Priority 3: Back to 401(k) (Beyond Match)

After maxing Roth IRA, return to 401(k)

Increase contributions toward maximum:

- 2024 limit: $23,000/year

- 2025 limit: $23,500/year (adjusts for inflation)

Why:

- Lowers current taxes (pre-tax contributions)

- Higher contribution limits than IRA

- Automatic payroll deduction (forced savings)

Target: 15-20% of income total between Roth IRA and 401(k)

Priority 4: HSA (If Eligible)

Health Savings Account—the “secret” retirement account

Requirements:

- Must have high-deductible health plan (HDHP)

Contribution limits (2024):

- Individual: $4,150/year

- Family: $8,300/year

Why it’s amazing:

- Triple tax advantage:

- Contributions are pre-tax

- Growth is tax-free

- Withdrawals for medical expenses are tax-free

- After age 65: Can withdraw for anything (taxed like 401k)

- No “use it or lose it”—rolls over forever

Strategy:

- Pay medical expenses out-of-pocket if possible

- Let HSA grow for decades

- Use in retirement for medical costs (tax-free) or anything (taxed)

Often called “the best retirement account nobody uses”

Priority 5: Taxable Brokerage Account

After maxing out all tax-advantaged accounts

What it is:

- Regular investment account

- No tax advantages

- No contribution limits

- No withdrawal restrictions

When to use:

- Already maxing 401(k) ($23,500) + Roth IRA ($7,000) + HSA ($4,150) = $34,650/year

- Want to save even more

- Need more flexibility

Advantages:

- No age restrictions on withdrawals

- Can use for early retirement (before 59½)

- Good for goals between now and retirement

The Complete Priority System

Your paycheck hierarchy:

- Get employer 401(k) match (3-6% of salary) ← Free money!

- Max Roth IRA ($7,000/year) ← Tax-free growth forever

- Increase 401(k) to hit 15-20% total savings

- Max HSA if eligible ($4,150/year) ← Triple tax advantage

- Max 401(k) ($23,500/year) ← If income allows

- Taxable brokerage ← If still have money to invest

Most people in 20s-30s: Focus on steps 1-3

What to Invest In: Asset Allocation by Age

Asset allocation = how you divide money between stocks and bonds

The Basic Principle

Stocks (higher risk, higher return):

- Young investors should heavily favor stocks

- You have decades to recover from crashes

- Higher long-term returns

Bonds (lower risk, lower return):

- Add bonds gradually as you age

- Provide stability and reduce volatility

- More important closer to retirement

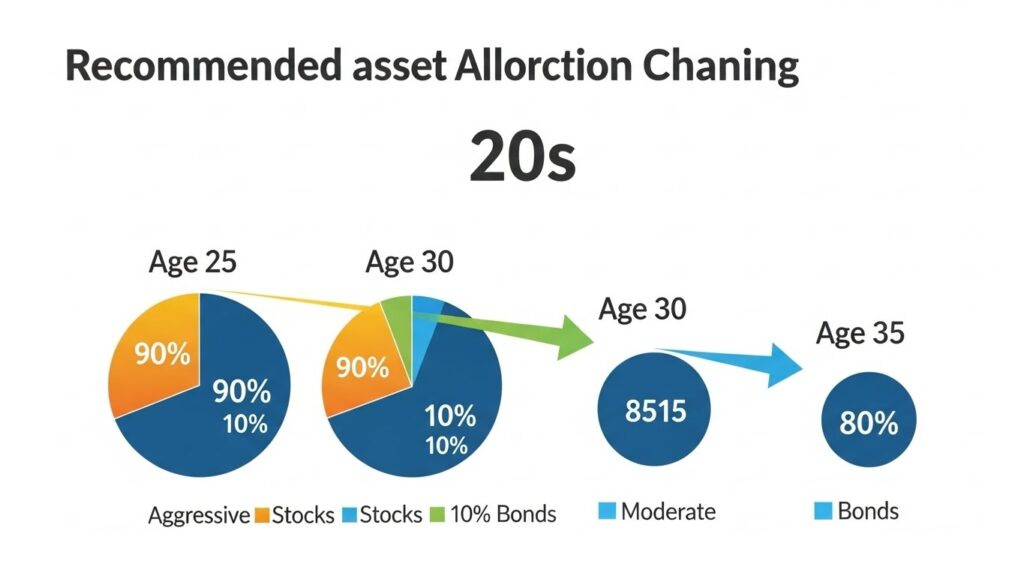

Recommended Allocation by Age

Ages 20-29: 90-100% Stocks / 0-10% Bonds

Why so aggressive:

- 40+ years until retirement

- Can recover from any crash

- Need maximum growth

- Even 50% crash recovers with time

Example allocation:

- 70% U.S. Total Stock Market (index fund)

- 20% International Total Stock Market

- 10% Bonds or keep 100% stocks

Ages 30-34: 85-90% Stocks / 10-15% Bonds

Why still aggressive:

- 30-35 years until retirement

- Still plenty of time

- Need strong growth

- Tiny bond allocation for learning/comfort

Example allocation:

- 60% U.S. Total Stock Market

- 25% International Total Stock Market

- 15% Total Bond Market

Ages 35-39: 80-85% Stocks / 15-20% Bonds

Why starting to moderate:

- 25-30 years until retirement

- Introducing more stability

- Still growth-focused

- Slight risk reduction

Example allocation:

- 55% U.S. Total Stock Market

- 25% International Total Stock Market

- 20% Total Bond Market

The “Your Age in Bonds” Rule (Traditional)

Old rule: Your age = % in bonds

- Age 25 = 25% bonds, 75% stocks

- Age 35 = 35% bonds, 65% stocks

Modern adjustment: Your age minus 10-20 = % in bonds

- Age 25 = 5-15% bonds, 85-95% stocks

- Age 35 = 15-25% bonds, 75-85% stocks

Why the adjustment:

- People live longer now

- Need more growth to last 30+ years in retirement

- Can afford more risk when young

What Specific Investments to Choose

Keep it simple with low-cost index funds:

For U.S. Stocks:

- Vanguard Total Stock Market (VTI)

- Schwab U.S. Broad Market (SCHB)

- Fidelity Total Market Index (FSKAX)

For International Stocks:

- Vanguard Total International (VXUS)

- iShares Core MSCI Total International (IXUS)

- Schwab International Equity (SCHF)

For Bonds:

- Vanguard Total Bond Market (BND)

- iShares Core U.S. Aggregate Bond (AGG)

- Schwab U.S. Aggregate Bond (SCHZ)

Or use a target-date fund:

- Example: “Target Date 2060 Fund” (if retiring around 2060)

- Automatically adjusts allocation as you age

- Perfect “set and forget” option

Learn more about ETFs and how they work for retirement investing

Retirement Investing Strategy for Your 20s (Ages 20-29)

Your 20s are about building habits and maximizing time. Here’s your specific strategy:

Financial Foundation First

Before aggressive retirement investing:

- Build $1,000 mini emergency fund

- Covers small emergencies

- Prevents going into debt

- Get employer 401(k) match

- Always priority #1

- Free money you can’t pass up

- Pay off high-interest debt (15%+ APR)

- Credit cards, personal loans

- Can’t earn 18% reliably, so eliminate 18% debt

- Build full 3-6 month emergency fund

- Financial stability foundation

- Allows confident investing

Then: Retirement Contribution Strategy

Early 20s (20-24):

If income $30,000-40,000:

- Contribute to get full 401(k) match (3-6%)

- If possible, add $100-200/month to Roth IRA

- Total: 10-12% of income

If income $40,000-55,000:

- Get full 401(k) match

- Contribute $300-400/month to Roth IRA

- Total: 12-15% of income

Mid-to-Late 20s (25-29):

As income grows to $45,000-65,000:

- Get full 401(k) match (3-6%)

- Max out Roth IRA ($7,000/year = $583/month)

- If still under 15% total, increase 401(k)

- Total: 15-18% of income

Investment Allocation in Your 20s

Be aggressive:

- 90-100% stocks

- 0-10% bonds

- Heavy U.S. and international stock exposure

Simple 3-fund portfolio:

- 70% Total U.S. Stock Market

- 20% Total International Stock Market

- 10% Total Bond Market (or 0% if comfortable)

Even simpler:

- 100% Target Date 2060-2065 Fund

Habits to Build in Your 20s

1. Automate everything:

- Set up automatic 401(k) contribution

- Automatic monthly transfer to Roth IRA

- Dollar-cost averaging happens automatically

2. Increase with raises:

- Got a 3% raise? Increase retirement savings by 1-2%

- You’ll never miss money you never had

3. Never touch retirement accounts:

- Resist temptation to withdraw

- Loans from 401(k) are last resort only

- Let compound interest work

4. Ignore short-term performance:

- Don’t check accounts obsessively

- Market drops are normal and temporary

- Stay invested through volatility

What Success Looks Like by 30

If you follow this strategy from 22-30:

- Saved 10-15% of income consistently

- 8 years of contributions and growth

- Likely have $40,000-80,000 saved (depending on income)

- Have 1x annual salary saved (the milestone)

Example:

- Age 22-30 (8 years)

- Average income $45,000

- Saved 12% = $5,400/year ($450/month)

- 8% average return

- Age 30 balance: ~$58,000

That $58,000 at age 30, with no additional contributions, grows to $632,000 by age 65!

That’s the power of your 20s.

Retirement Investing Strategy for Your 30s (Ages 30-39)

Your 30s are about acceleration and maximization. Income is higher, strategy gets more sophisticated:

Financial Situation in Your 30s

Common realities:

- Income 30-70% higher than 20s

- Maybe married, maybe kids

- Possibly homeowner

- Student loans hopefully declining or paid off

- Career more established

This means:

- Higher savings capacity

- More competing priorities (kids, house)

- Need to balance multiple goals

- Last chance before retirement savings gets much harder

Retirement Contribution Strategy

Early 30s (30-34):

If income $50,000-70,000:

- Get full 401(k) match (3-6%)

- Max Roth IRA ($7,000/year)

- Increase 401(k) to hit 15% total

- Total: 15-18% of income

If income $70,000-100,000:

- Get full 401(k) match

- Max Roth IRA ($7,000/year)

- Increase 401(k) toward maximum ($23,500/year)

- Consider HSA if eligible

- Total: 18-22% of income

Mid-to-Late 30s (35-39):

If started late (didn’t save in 20s):

- Need 18-22% to catch up

- Prioritize maxing Roth IRA

- Aggressive 401(k) contributions

- Every 1% increase matters

If on track from 20s:

- Maintain 15-20%

- Consider maxing 401(k) ($23,500)

- Add HSA contributions if eligible

- Build taxable brokerage if maxing accounts

Investment Allocation in Your 30s

Still aggressive but slightly moderating:

Ages 30-34:

- 85-90% stocks

- 10-15% bonds

Ages 35-39:

- 80-85% stocks

- 15-20% bonds

Example portfolios:

Age 32:

- 60% U.S. Total Stock

- 25% International Total Stock

- 15% Total Bond Market

Age 37:

- 55% U.S. Total Stock

- 25% International Total Stock

- 20% Total Bond Market

Advanced Strategies for Your 30s

1. Backdoor Roth IRA (if income too high):

- Traditional IRA contribution

- Immediately convert to Roth

- Bypasses income limits

2. Mega Backdoor Roth (if 401k allows):

- After-tax 401(k) contributions

- Convert to Roth 401(k) or Roth IRA

- Can contribute up to $69,000/year total (2024)

3. Tax-loss harvesting in taxable accounts:

- Sell losing investments for tax deduction

- Immediately buy similar investment

- Reduces taxes without changing allocation

4. Consider financial advisor:

- If income over $100k

- Complex situation (business owner, stock options)

- Want professional guidance

What Success Looks Like by 40

If you follow this strategy from 30-40:

- Saved 15-20% consistently

- 10 years of contributions on top of 20s

- Likely have $150,000-350,000 saved

- Have 3x annual salary saved (the milestone)

Example:

- Age 30-40 (10 years)

- Average income $65,000

- Saved 18% = $11,700/year ($975/month)

- Starting balance: $60,000 (from 20s)

- 8% average return

- Age 40 balance: ~$265,000

With that $265,000 at age 40, continuing to save $975/month:

- By age 65: $2,247,000

- Comfortable retirement achieved

How to Balance Retirement with Other Financial Goals

Your 20s and 30s have competing priorities. Here’s how to balance them:

The Priority Framework

Tier 1 (Non-negotiable):

- $1,000 mini emergency fund

- Employer 401(k) match (free money!)

- High-interest debt over 15% (credit cards, payday loans)

Tier 2 (Build foundation): 4. Full 3-6 month emergency fund 5. Moderate interest debt 7-15% (personal loans, some student loans)

Tier 3 (Wealth building): 6. Retirement savings (Roth IRA, 401k beyond match) 7. Save for house down payment (if goal within 3-5 years) 8. Low-interest debt under 7% (student loans, car loans)

Tier 4 (Advanced goals): 9. Max out all retirement accounts 10. Taxable investment accounts 11. Save for kids’ college 12. Other investments

Common Scenarios and Solutions

Scenario 1: “I have $30,000 in student loans at 5%”

Strategy:

- Get 401(k) match (Tier 1)

- Build emergency fund (Tier 2)

- Split between retirement and extra loan payments

- Invest 10% in retirement, put extra toward loans

- As loans decrease, shift that money to retirement

Why: 5% debt vs 8-10% investment returns = invest while paying minimums is mathematically better, but psychological win of eliminating debt is valid too. Split the difference.

Scenario 2: “I want to buy a house in 3 years”

Strategy:

- Get 401(k) match (never skip!)

- Build emergency fund

- Save for down payment in high-yield savings (not investments!)

- Reduce retirement to 10% temporarily if needed

- After buying house, increase retirement back to 15%+

Why: Money needed within 3-5 years shouldn’t be in stocks. Use savings. Temporarily reducing retirement is okay for important life goal.

Scenario 3: “I’m 32 and didn’t save in my 20s”

Strategy:

- Start NOW (today!)

- Get 401(k) match

- Max Roth IRA ($7,000)

- Increase 401(k) to 18-22% of income

- Cut expenses aggressively for 2-3 years to catch up

- Every raise goes to retirement

Why: Can’t change the past, but 30 years is still enough. Need higher savings rate but absolutely can catch up.

Scenario 4: “My employer doesn’t offer 401(k)”

Strategy:

- Max Roth IRA ($7,000/year)

- Open Traditional IRA for additional $7,000/year

- If income too high for Traditional IRA deduction, use taxable brokerage

- Consider changing jobs to employer with 401(k)

Why: Losing out on employer match and higher contribution limits, but can still save 15% in IRAs and taxable accounts.

Scenario 5: “I want to start a business in 5 years”

Strategy:

- Get 401(k) match now

- Save 10% for retirement

- Save aggressively in taxable brokerage for business

- Keep business funds separate from retirement

- Don’t raid retirement for business

Why: Starting business is risky. Keep retirement protected. Can use taxable brokerage funds for business without penalties.

The 50/30/20 Budget Rule Applied

50% Needs:

- Housing, food, utilities, transportation, insurance

- Essential debt payments

20% Savings & Debt:

- 15% retirement

- 5% emergency fund/other savings/extra debt payments

30% Wants:

- Entertainment, dining out, hobbies, shopping

- Adjust this down if need to save more

When to Prioritize Retirement Over Other Goals

Always prioritize retirement over:

- Paying off very low-interest debt (under 3%)

- Saving for kids’ college (they can get loans, you can’t for retirement)

- Buying brand-new car (buy used and invest difference)

- Expensive wedding (keep it reasonable, invest difference)

Temporarily reduce retirement for:

- Building emergency fund (critical foundation)

- House down payment (if ready and makes financial sense)

- Starting business (if well-planned)

- Eliminating high-interest debt (over 8%)

Never sacrifice retirement for:

- Keeping up with friends’ lifestyles

- Expensive vacation

- Luxury purchases

- “I’ll catch up later” (you won’t—never works)

Common Retirement Investing Mistakes in Your 20s and 30s

Mistake 1: Not Starting Because “I’ll Do It Later”

The error: “I’m only 24, I have plenty of time. I’ll start saving seriously in my 30s.”

Why it’s devastating:

- Lose the most powerful compounding years

- 10 years of contributions in 20s = hundreds of thousands more at retirement

- Starting at 35 vs 25 costs $324,000+ (from earlier example)

The fix: Start with even $50-100/month NOW. Increase later. Starting beats waiting.

Mistake 2: Not Taking the Employer Match

The error: “I can’t afford to save for retirement right now.”

Why it’s wrong:

- Turning down free money (50-100% instant return!)

- Would you refuse a raise? That’s what this is!

- Even if in debt, get the match

Example of lost money:

- Salary: $50,000

- Employer matches 50% up to 6%

- Not contributing: Losing $1,500/year in free money

- Over 10 years with growth: Lost $22,000+

The fix: At minimum, contribute enough to get full match. Always.

Mistake 3: Cashing Out 401(k) When Changing Jobs

The error: “I’m leaving my job. I’ll just take that $8,000 in my 401(k).”

Why it destroys wealth:

- Pay income taxes (22-24% bracket = $1,760-1,920)

- Pay 10% early withdrawal penalty ($800)

- Lose all future growth

That $8,000 at age 28:

- Cashed out: Receive $5,280, lose $2,720 to taxes/penalties

- Left invested until 65: Worth $86,000

Cost of cashing out: $80,720!

The fix: Roll over to new employer 401(k) or IRA. Never cash out.

Mistake 4: Investing Too Conservatively

The error: “I don’t want to lose money, so I’ll put my 401(k) in the stable value fund (1% return).”

Why it’s wrong:

- In your 20s-30s, you need growth, not safety

- 1-2% barely beats inflation

- Missing out on 8-10% returns

Impact:

- $500/month for 30 years at 2% = $246,000

- $500/month for 30 years at 8% = $745,000

- Lost: $499,000!

The fix: 85-100% stocks in your 20s-30s. Accept volatility for growth.

Mistake 5: Trying to Time the Market

The error: “The market is at all-time highs. I’ll wait for a crash to invest.”

Why it fails:

- Market timing doesn’t work—even professionals fail

- Miss months/years of growth waiting

- When crash comes, too scared to buy

- Dollar-cost averaging beats timing

Example:

- Waiting for “perfect” time since 2020

- S&P 500 up 60%+ since then

- Still waiting while missing massive gains

The fix: Invest consistently regardless of market level. Automate it.

Mistake 6: Stopping During Market Crashes

The error: Market crashes 30%, panic, stop contributing or sell everything.

Why it’s catastrophic:

- Sell at worst time (locking in losses)

- Miss the recovery (happens fast)

- Miss buying at discount prices

Historical fact: Every crash in history has recovered. Every single one.

The fix: Keep investing through crashes. You’re buying stocks on sale! This is when fortunes are built.

Mistake 7: Ignoring Fees

The error: Not paying attention to expense ratios in 401(k).

Why it matters:

- 1% fee doesn’t sound like much

- Over decades, costs hundreds of thousands

Example:

- $300/month for 35 years at 8% return

- 0.05% fee: $611,000

- 1.00% fee: $508,000

- Cost of high fees: $103,000!

The fix: Choose lowest-cost index funds in your 401(k). Target under 0.20% expense ratio.

Mistake 8: Not Increasing Contributions with Raises

The error: Got 4% raise, lifestyle inflates by 4%, retirement contributions stay the same.

Why it’s missed opportunity:

- Perfect time to save more without feeling it

- Slow creep toward better retirement

Better approach:

- Got 4% raise? Increase retirement by 1-2%

- Still enjoy 2-3% lifestyle improvement

- Retirement improves without sacrifice

Example:

- Salary $50,000 → $52,000 (4% raise)

- Increase 401(k) from 6% → 8%

- Still take home more, save much more long-term

Your Step-by-Step Retirement Investment Action Plan

Ready to start? Here’s exactly what to do:

This Week

Day 1-2: Assess Your Situation

- Calculate monthly income

- Review current retirement savings (if any)

- Check if employer offers 401(k) and match percentage

- Calculate what 15% of income would be

Day 3-4: Set Up Accounts

- Sign up for employer 401(k) (if not already)

- Open Roth IRA account (Vanguard, Fidelity, or Schwab)

- Set contribution to get full employer match minimum

Day 5-7: Choose Investments

- In 401(k): Select target-date fund OR low-cost index funds

- In Roth IRA: Choose total stock market or target-date fund

- Set up automatic monthly contribution to Roth IRA

This Month

Week 2:

- Review budget to find money for retirement savings

- Identify one expense to cut ($50-200/month)

- Redirect that money to Roth IRA

Week 3:

- Set up automatic transfers on payday

- Enable automatic dividend reinvestment

- Review investment allocations (80-100% stocks)

Week 4:

- Calculate if you’re hitting 15% total (401k + IRA)

- If not, make plan to increase gradually

- Set calendar reminder in 6 months to increase 1%

This Year

Quarter 1 (Months 1-3):

- Build $1,000 mini emergency fund if don’t have

- Consistently contribute to 401(k) and Roth IRA

- Don’t check accounts obsessively (quarterly max)

Quarter 2 (Months 4-6):

- Increase contributions if got raise

- Check if hitting 15% goal

- Adjust budget if needed

Quarter 3 (Months 7-9):

- Review investment performance (don’t panic if down)

- Ensure still getting full employer match

- Consider increasing by 1% if comfortable

Quarter 4 (Months 10-12):

- Annual review of accounts and allocations

- Rebalance if allocation drifted more than 5%

- Set goals for next year (increase savings rate?)

Long-Term (Next 5-10 Years)

Every year:

- Increase contributions by 1% (or half of raises)

- Review and rebalance once annually

- Adjust allocation gradually (add 1-2% bonds per 5 years)

By age 30:

- Have 1x salary saved

- Be contributing 15% minimum

- Have Roth IRA maxed ($7,000/year)

By age 35:

- Have 2x salary saved

- Be contributing 15-20%

- Consider HSA if eligible

By age 40:

- Have 3x salary saved

- Be contributing 18-22%

- Working toward maxing 401(k)

Frequently Asked Questions – FAQ

How much should I save for retirement in my 20s?

In your 20s, aim to save 10-15% of your gross income for retirement, increasing toward 15% as income grows. At minimum, always contribute enough to get your full employer 401(k) match—this is free money you can’t pass up. If you’re 25 earning $45,000, this means $4,500-6,750 per year ($375-563 per month). Start with employer match, then max your Roth IRA ($7,000/year), then increase 401(k) contributions.

Is it too late to start saving for retirement at 30?

No, 30 is not too late—you still have 35 years until retirement, which is plenty of time for compound interest to work. However, you’ll need to save 15-18% of income (versus 12-15% if you started at 25) to catch up. Start immediately by getting your employer match, maxing your Roth IRA, and increasing your 401(k) contributions. A 30-year-old saving $500/month until 65 at 8% returns will accumulate over $935,000—more than enough for retirement.

Should I pay off student loans or invest for retirement?

Do both, but prioritize based on interest rates. Always get your employer 401(k) match first (free money). For high-interest debt (8%+), aggressively pay it off while saving 10% for retirement. For moderate interest (4-7%), split between extra payments and retirement. For low interest (under 4%), make minimum payments and invest the rest—investment returns typically exceed low interest rates over time. Never skip the employer match to pay debt.

What’s the best retirement account for someone in their 20s or 30s?

The Roth IRA is the best retirement account for most people in their 20s and 30s because you’re likely in a lower tax bracket now than you will be in retirement. You pay taxes on contributions now, but all growth and withdrawals in retirement are completely tax-free. Max this out ($7,000/year) after getting your employer 401(k) match. The decades of tax-free compound growth make this incredibly powerful for young investors.

How should I invest my retirement money in my 30s?

In your 30s, invest 80-90% in stocks and 10-20% in bonds using low-cost index funds. A simple three-fund portfolio works perfectly: 60% U.S. total stock market fund, 25% international stock fund, and 15% bond fund. Or use a target-date fund (like “Target 2055”) that automatically adjusts as you age. Avoid trying to pick individual stocks or timing the market—consistent investing in diversified, low-cost funds beats active management for most investors.

Can I retire early if I start investing in my 20s?

Yes, starting in your 20s makes early retirement possible if you save aggressively. Retiring at 55 instead of 65 requires saving 25-30% of income versus the standard 15%. For example, saving $1,000/month from age 25-55 (30 years) at 8% returns gives you approximately $1.5 million—enough to retire comfortably. The key is starting early, saving consistently, living below your means, and letting compound interest do the heavy lifting over decades.

BONUS

Want to see retirement investing strategies in action?

This video shows exactly how young investors can build wealth for retirement:

Here’s what most people in their 20s and 30s don’t realize: the retirement savings decisions you make today will determine your entire quality of life from age 65 until you die.

That’s not an exaggeration. That’s reality.

Your choices today determine whether you:

- Retire comfortably at 65 or work until 75

- Travel in retirement or struggle to pay bills

- Help your kids or depend on them financially

- Live with dignity or constant financial stress

And the decisions are simple:

- Start now or wait?

- Save 15% or spend it?

- Get the match or leave free money on the table?

- Invest consistently or try to time the market?

- Stay invested through crashes or panic sell?

The Math Is Unforgiving

Start at 25, save $500/month for 40 years at 8%: $1,745,000

Start at 35, save $500/month for 30 years at 8%: $745,000

Difference from waiting 10 years: $1,000,000

One million dollars. That’s what procrastination costs.

But here’s the good news: you’re reading this right now, which means you haven’t waited too long.

If you’re 24, you have the full power of compound interest ahead of you. If you’re 34, you still have 30 years—plenty of time. If you’re 39, you can still build a comfortable retirement with focused effort.

The Simple Truth

You don’t need to be a financial genius. You don’t need to pick winning stocks or time the market perfectly. You don’t need a six-figure income.

You need:

- Start now (today, not next month)

- Get the employer match (free money)

- Max the Roth IRA ($7,000/year)

- Save 15-20% consistently (automate it)

- Invest in low-cost index funds (80-100% stocks)

- Never stop or panic-sell (stay invested through everything)

That’s it. That’s the strategy that’s created millions of comfortable retirements.

Your Action This Week

Stop reading. Start doing.

Monday: Sign up for 401(k) (if not already), increase to get full match

Tuesday: Open Roth IRA at Vanguard, Fidelity, or Schwab

Wednesday: Set up automatic $250-500/month transfer to Roth IRA

Thursday: Choose investments (target-date fund or index funds)

Friday: Enable automatic dividend reinvestment

Done. Your retirement is now on autopilot.

Forty years from now, you’ll look back at this week as one of the most important in your life. The week you took control of your financial future. The week you guaranteed a comfortable retirement.

The compound interest clock is ticking. Every day you wait costs you money you’ll never get back.

Start today. Your 65-year-old self is counting on you.

INTERESTING TOPICS

Ready to understand the power behind retirement investing?

Learn about compound interest and why time is your greatest asset.

Want to invest consistently without timing the market?

Master dollar-cost averaging, the strategy that removes emotion from retirement investing.

Need to know what to invest in?

Discover index funds and ETFs, the perfect vehicles for retirement savings.

For more content on finance and relevant information to enhance your knowledge and learning,

subscribe to our newsletter and receive weekly articles in your personal email.

Disclaimer: This article is for educational purposes only. Diversification does not guarantee profits or protect against all losses. Consider your financial situation, risk tolerance, and investment timeline before making investment decisions.

—— End of Article ——