Roth IRA vs Traditional IRA: Which is Right for You?

Last updated: February 2026

You’ve decided to invest for retirement.

You’ve chosen your investments. You understand volatility. You’re ready to act.

Now comes the critical question: Where should you PUT this money?

You could invest in a regular taxable brokerage account. But that’s leaving free money on the table.

You could open a Traditional IRA. Tax deductible now, but taxes later.

Or you could open a Roth IRA. No tax deduction now, but tax-free forever.

Which one? Why does it matter? How much difference does it actually make?

This single decision could cost you hundreds of thousands of dollars in taxes over your lifetime. Or save you that amount. The difference between a Roth and Traditional IRA isn’t academic—it’s life-changing money.

But here’s the good news: Understanding the difference is simpler than you think.

It comes down to one fundamental question: Do you want to pay taxes now or later?

In this guide, you’ll discover exactly what Traditional IRAs are and how they work, exactly what Roth IRAs are and how they work, the key differences between them, which one is better for different situations, the 2026 contribution limits and rules, how to open each type, common mistakes to avoid, and most importantly—which one is right for YOU.

By the end, you’ll make the decision that saves you the most money in taxes.

Let’s get your retirement on the right track.

What is a Traditional IRA? (Complete Definition)

A Traditional IRA is a retirement savings account where contributions may be tax-deductible in the year you make them, and your investments grow tax-free, but withdrawals in retirement are taxed as ordinary income.

In simpler terms: Invest pre-tax dollars, grow tax-free, pay taxes on withdrawals.

How Traditional IRAs Work

Step 1: You Contribute

- You deposit money into your Traditional IRA

- In most cases, this contribution is tax-deductible

- You reduce your taxable income for that year

- Saves you taxes NOW

Step 2: Your Money Grows

- Inside the IRA, your investments grow

- You earn dividends, interest, capital gains

- NONE of this growth is taxed annually

- All gains compound tax-free

Step 3: You Retire (Age 59½+)

- You start withdrawing money

- Each withdrawal is taxed as ordinary income

- You pay taxes LATER

Step 4: You Must Withdraw (Age 73+)

- IRS requires minimum distributions

- You must withdraw a percentage yearly

- Creates tax bill whether you want it or not

Real Example: Traditional IRA

Year 1:

- You contribute: $7,000

- Tax deduction saves you: $2,100 in taxes (at 30% tax bracket)

- Out-of-pocket cost: $4,900

- IRA balance: $7,000

Year 10 (after growth at 8% annually):

- IRA balance: $15,107

- You’ve never paid taxes on the $8,107 in gains

Age 65 (retirement):

- IRA balance: $150,000

- You withdraw: $5,000

- Taxes owed: $1,500 (at 30% rate)

- You receive: $3,500

Key point: You saved $2,100 in taxes upfront. But you’ll pay taxes on everything you withdraw later.

Traditional IRA Advantages

✅ Tax deduction now — Reduces current year taxes

✅ Tax-free growth — Compound interest works harder

✅ Lower current tax burden — More money in your pocket today

✅ Flexibility — Can contribute to Traditional and Roth in same year

✅ No income limits — Anyone can open one (though deduction may be limited)

Traditional IRA Disadvantages

❌ Taxes on withdrawals — Pay taxes later at ordinary income rates

❌ Mandatory withdrawals — RMDs starting at age 73

❌ Tax bill in retirement — Creates required income/taxes

❌ Unknown future tax rates — If rates rise, you pay more

❌ Less flexibility — Some withdrawal restrictions

What is a Roth IRA? (Complete Definition)

A Roth IRA is a retirement savings account where contributions are made with after-tax dollars (not tax-deductible), investments grow tax-free, and qualified withdrawals are completely tax-free.

In simpler terms: Invest after-tax dollars, grow tax-free, withdraw tax-free forever.

How Roth IRAs Work

Step 1: You Contribute

- You deposit money into your Roth IRA

- This contribution is NOT tax-deductible

- You pay taxes on this money today

- No immediate tax savings

Step 2: Your Money Grows

- Inside the Roth, your investments grow

- You earn dividends, interest, capital gains

- NONE of this growth is taxed annually

- All gains compound tax-free

Step 3: You Retire (Age 59½+)

- You start withdrawing money

- Withdrawals are completely tax-free

- IRS taxes nothing

- You pay ZERO taxes forever

Step 4: No Mandatory Withdrawals

- Unlike Traditional IRA, NO required withdrawals

- Your money can stay invested forever

- Can pass to heirs tax-free

Real Example: Roth IRA

Year 1:

- You contribute: $7,000

- No tax deduction

- You paid taxes when earning the money

- Out-of-pocket cost: $7,000

- Roth balance: $7,000

Year 10 (after growth at 8% annually):

- Roth balance: $15,107

- You’ve never paid taxes on the $8,107 in gains

- And you NEVER will

Age 65 (retirement):

- Roth balance: $150,000

- You withdraw: $5,000

- Taxes owed: $0

- You receive: $5,000 (all of it!)

Key point: You didn’t save upfront. But you pay ZERO taxes on everything forever.

Roth IRA Advantages

✅ Tax-free withdrawals — Pay zero taxes in retirement

✅ Tax-free growth — All $150,000 in gains are yours

✅ No mandatory withdrawals — Money stays invested

✅ Withdraw contributions anytime — Access to contributions penalty-free

✅ Tax-free to heirs — Pass tax-free wealth to family

✅ Unknown taxes don’t matter — Locked in at zero

Roth IRA Disadvantages

❌ No tax deduction now — Pay full taxes today

❌ Income limits — High earners can’t contribute directly

❌ Five-year rule — Must wait 5 years to withdraw earnings

❌ Less cash now — Full out-of-pocket cost today

❌ Harder to contribute if high income — Phased out at certain incomes

Key Differences: Traditional vs Roth

Let’s compare them directly:

Contribution Tax Treatment

Traditional IRA:

- Contribution may be tax-deductible

- You reduce taxable income today

- Example: Contribute $7,000, saves $2,100 in taxes

Roth IRA:

- Contribution NOT tax-deductible

- No tax savings today

- Example: Contribute $7,000, save $0 in taxes

Growth

Both the Same:

- Investments grow tax-free inside account

- No annual taxes on gains

- Compound interest works identically

Withdrawal Taxes

Traditional IRA:

- Withdrawals taxed as ordinary income

- 100% of withdrawal is taxable (if all contributions were deductible)

- Example: Withdraw $150,000, pay tax on full amount

Roth IRA:

- Withdrawals completely tax-free

- 0% of withdrawal is taxable

- Example: Withdraw $150,000, pay tax on $0

Income Limits

Traditional IRA:

- No income limits for opening

- Deduction phase-out if covered by employer plan

- Example: Can open anytime

Roth IRA:

- Income limits for contributions

- High earners can’t contribute directly

- 2026 limits: Single $146,000+, Married $230,000+ (phases out)

Withdrawal Rules

Traditional IRA:

- Can’t withdraw before age 59½ without penalty

- Must start withdrawals at age 73 (RMD)

- Exceptions for hardship, disability, etc.

Roth IRA:

- Can withdraw contributions anytime, penalty-free

- Earnings have 5-year rule before penalty-free withdrawal

- No mandatory withdrawals ever

Tax Implications: The Core Difference

This is what actually matters financially.

The Simple Question

Traditional IRA: Pay taxes later (on withdrawals) Roth IRA: Pay taxes now (on contributions)

Which is better depends on one thing: Will your tax rate be higher or lower in retirement?

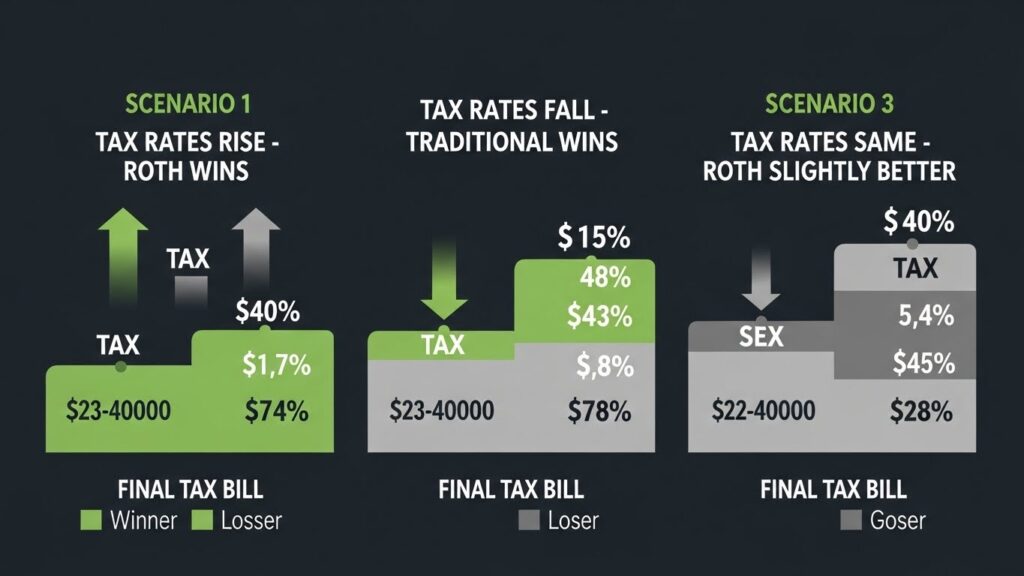

Scenario 1: Tax Rates Rise (Roth Wins)

Today:

- Your tax bracket: 24%

- You earn: $100,000

Retirement (in 30 years):

- Tax rates have risen

- Your tax bracket: 35%

Traditional IRA Result:

- Contribution saved: $2,400 in taxes (24% × $100,000)

- But withdraw $150,000 in retirement

- Taxes owed: $52,500 (35% × $150,000)

- Net: Paid more taxes (ouch!)

Roth IRA Result:

- Contribution cost: $2,400 in taxes (24% × $100,000)

- Withdraw $150,000 in retirement

- Taxes owed: $0

- Net: Paid same upfront, but saved on growth

Winner: Roth (if rates rise)

Scenario 2: Tax Rates Fall (Traditional Wins)

Today:

- Your tax bracket: 35%

- You earn: $100,000

Retirement (in 30 years):

- Tax rates have fallen

- Your tax bracket: 24%

Traditional IRA Result:

- Contribution saved: $3,500 in taxes (35% × $100,000)

- Withdraw $150,000 in retirement

- Taxes owed: $36,000 (24% × $150,000)

- Net: Saved money!

Roth IRA Result:

- Contribution cost: $3,500 in taxes (35% × $100,000)

- Withdraw $150,000 in retirement

- Taxes owed: $0

- Net: Paid more upfront

Winner: Traditional (if rates fall)

Scenario 3: Tax Rates Stay Same

Traditional IRA:

- Save $2,400 upfront, pay $2,400+ later (on growth)

- Roughly equal or slightly worse

Roth IRA:

- Pay $2,400 upfront, pay $0 later

- Roughly equal or slightly better (because tax-free growth is better)

The Reality

Nobody knows future tax rates. This is the core problem.

However, most experts believe:

- Tax rates will likely rise (government debt growing)

- Roth is safer bet (locking in current rates)

- Diversification is smartest (use both!)

Income Limits and Eligibility

Not everyone can contribute to a Roth IRA. Income limits exist.

Traditional IRA

Anyone with earned income can open one.

Tax deduction phase-out (if covered by employer retirement plan):

- Single: $77,000-$87,000 (2026)

- Married filing jointly: $123,000-$133,000 (2026)

- Married filing separately: $0-$10,000 (2026)

If you’re below these limits: Full deduction If you’re between these limits: Partial deduction If you’re above these limits: No deduction (but can still contribute)

Roth IRA

Income limits for direct contributions:

Single Filers (2026):

- Below $146,000: Can contribute full amount

- $146,000-$161,000: Partial contribution (phase-out)

- Above $161,000: Cannot contribute directly

Married Filing Jointly (2026):

- Below $230,000: Can contribute full amount

- $230,000-$240,000: Partial contribution (phase-out)

- Above $240,000: Cannot contribute directly

Married Filing Separately:

- Below $0: Can contribute

- $0-$10,000: Partial contribution

- Above $10,000: Cannot contribute

The SEC provides comprehensive information about IRAs, contribution limits, tax implications, and how to choose between account types.

What If You Make Too Much for Roth?

Backdoor Roth Strategy:

- Contribute to Traditional IRA (no income limits)

- Immediately convert to Roth IRA

- Pay taxes on the conversion

- Achieve Roth benefits despite high income

(More complex, but works for high earners)

Contribution Limits for 2026

How Much Can You Contribute?

For 2026:

For detailed information about current IRA contribution limits, eligibility requirements, and annual updates, the IRS provides official guidelines.

- Age under 50: $7,000/year maximum

- Age 50+: $8,000/year maximum (catch-up)

Total per person per year: $7,000 or $8,000

Important: You can split between Traditional and Roth

- Example: $4,000 Traditional + $3,000 Roth = $7,000 total

You CANNOT contribute $7,000 to each.

Can You Contribute If You Have No Income?

Traditional IRA: No, you need earned income

Roth IRA: No, you need earned income

Exception: Spousal IRA (working spouse can contribute for non-working spouse)

When Must You Contribute?

Deadline: April 15 of next year

- Contribute in 2025 by April 15, 2026

- Or contribute in 2026 anytime before April 15, 2027

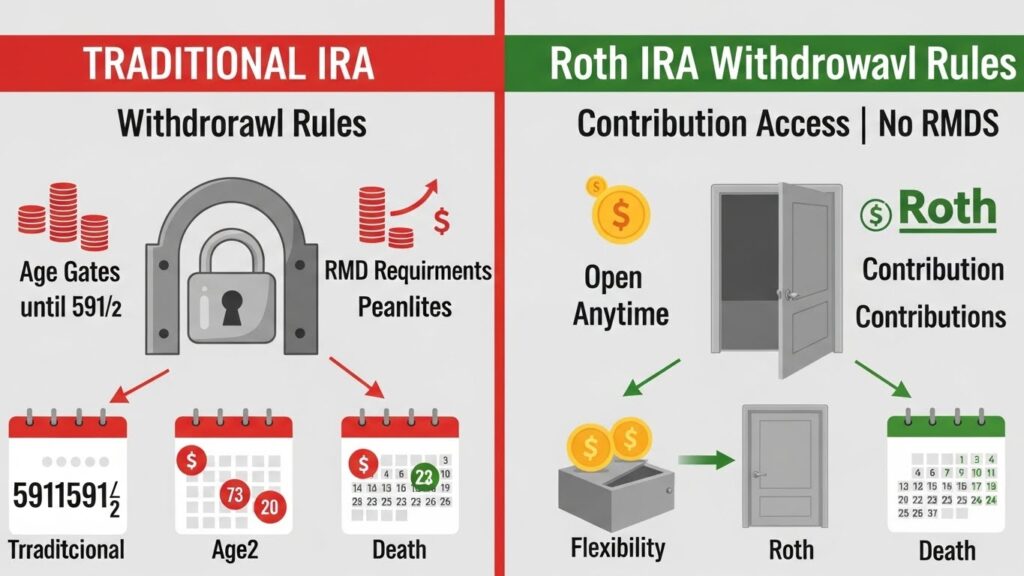

Withdrawal Rules: When You Can Access Your Money

This matters more than you think.

Traditional IRA Withdrawals

Before Age 59½:

- Can withdraw, but 10% penalty applies

- Plus income taxes on full amount

- Example: Withdraw $10,000, pay $1,000 penalty + $2,400 taxes (24%) = $6,600 received

Exceptions (no penalty):

- Disability or death

- First-time home buyer ($10,000 lifetime)

- Qualified education expenses

- Medical expenses over 7.5% AGI

- Health insurance premiums (if unemployed)

- IRS levy

- SEPP (Substantially Equal Periodic Payments)

After Age 59½:

- Withdraw anytime, no penalty

- Still pay ordinary income taxes

Age 73+:

- Must take Required Minimum Distributions

- IRS dictates how much you withdraw

- Fail to withdraw = 25% penalty (reduced to 10% if caught early)

Roth IRA Withdrawals

Contributions anytime:

- Can withdraw contributions anytime, no penalty, no taxes

- Example: Contributed $35,000 over 5 years, can withdraw $35,000 anytime penalty-free

- This is HUGE advantage for emergencies

Earnings before Age 59½:

- 10% penalty + income taxes

- Same exceptions as Traditional IRA apply

Earnings after Age 59½ (and 5-year rule met):

- Withdraw completely tax-free

- No penalties, no taxes

No mandatory withdrawals:

- Ever

- Your money can stay invested forever

- Can pass to heirs

Early Withdrawal Penalties and Exceptions

Understanding exceptions matters.

Traditional IRA Exceptions (No 10% Penalty)

Qualified exceptions:

- Disability (permanent and total)

- Medical expenses (over 7.5% of AGI)

- Health insurance (unemployed, needs coverage)

- Qualified education expenses

- First-time home buyer ($10,000 lifetime limit)

- IRS levy

- Substantially Equal Periodic Payments (SEPP)

- Heir distributions

- Birth/adoption expenses ($5,000 lifetime)

You still owe income taxes on all withdrawals above contributions.

Roth IRA Advantages (Contribution Access)

You can ALWAYS withdraw contributions:

- No penalty, no taxes

- You contributed after-tax dollars

- IRS has already taxed this money

Example:

- Contributed $40,000 over 8 years

- Account grown to $60,000

- You can withdraw $40,000 anytime

- Zero penalty, zero taxes

- The $20,000 gain stays invested

This makes Roth safer for emergencies.

Required Minimum Distributions (RMDs)

One critical difference many people miss.

Traditional IRA RMDs

Starting age 73 (as of 2023, was 72, will increase):

- IRS calculates required minimum

- Formula: Account balance ÷ life expectancy factor

- Example: $500,000 balance at age 75 = ~$18,900 required withdrawal

If you don’t withdraw:

- 25% penalty on amount not withdrawn (reduced to 10% if corrected)

- Must still pay income taxes on withdrawal

You cannot avoid this:

- Don’t need the money? Too bad, withdraw anyway

- Creates tax bill whether you want it

- Can’t use “I don’t want to withdraw” excuse

Roth IRA No RMDs

Your lifetime:

- ZERO required withdrawals

- Your money stays invested forever

- Never forced to create tax bill

After you pass away:

- Heirs must withdraw within 10 years

- But no RMD timeline for you

This is HUGE advantage for wealth building.

Which IRA is Right for You?

Here’s the decision framework.

Choose Traditional IRA If:

✅ You want to reduce taxes NOW

- You’re in high tax bracket today

- You want maximum deduction this year

- You need cash flow relief today

✅ You expect lower taxes in retirement

- You’ll have less income

- Tax rates might fall

- You’ll be in lower bracket

✅ You want to maximize contributions

- Deduction gives you more investable money today

- The tax savings gives you extra cash

✅ You expect to live frugally in retirement

- Lower retirement income = lower taxes

- Withdrawals will be small

✅ You want to reduce current AGI

- Deduction lowers adjusted gross income

- Can help with other tax benefits

- Can help with income phase-outs for other programs

Choose Roth IRA If:

✅ You expect higher taxes in retirement

- Tax rates will rise

- Your retirement income will be high

- You want to lock in current rates

✅ You’re young (decades until retirement)

- Time horizon is long

- Tax-free growth compounds for decades

- Early withdrawals less likely

✅ You’re in lower tax bracket now

- Tax cost of contribution is low

- Tax-free growth is huge benefit

✅ You want flexibility in retirement

- Can withdraw contributions anytime

- No required minimum distributions

- More control over income/taxes

✅ You want to leave tax-free money to heirs

- Roth passes tax-free to family

- Traditional requires heirs to pay taxes

✅ You want simplicity in retirement

- No required withdrawals

- No complicated tax calculations

- Less stress

The Honest Truth

Most people should prioritize Roth if eligible because:

- Tax rates likely rising

- Tax-free growth for 30+ years is powerful

- No forced distributions

- More flexibility

- Heirs get tax-free wealth

However, if you’re in very high tax bracket today:

- Traditional IRA deduction is valuable now

- Might make sense

The Strategic Approach: Using Both

Here’s what smart investors do.

Diversify Your Tax Strategy

Contribute to both:

- Some to Traditional (get deduction now)

- Some to Roth (lock in tax-free growth)

- Example: $4,000 Traditional + $3,000 Roth = $7,000 total

Benefits:

- Hedge against unknown future tax rates

- Have both tax-deferred and tax-free accounts

- Maximize flexibility in retirement

- Can withdraw from lowest-tax account when needed

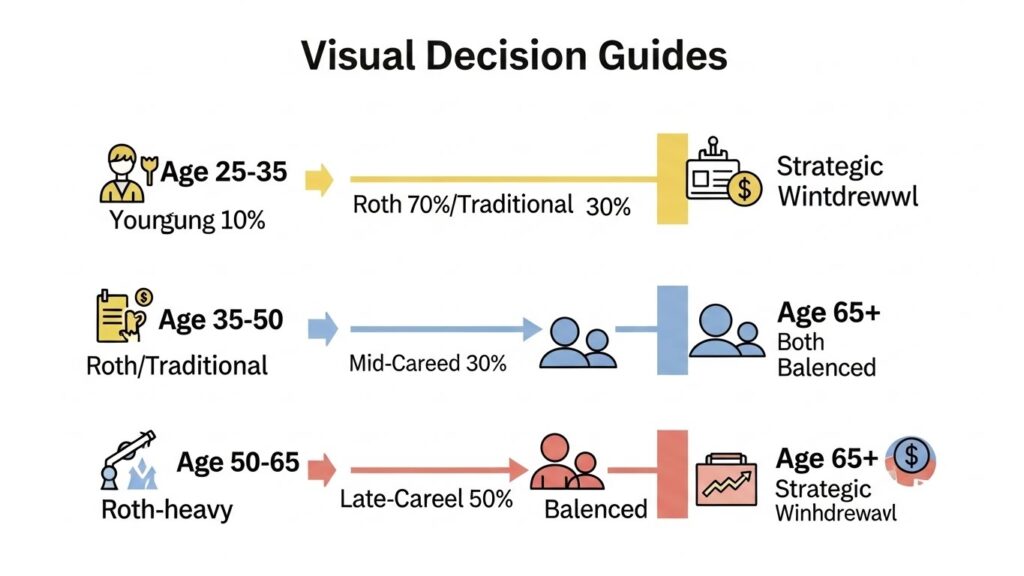

Example Strategy by Age

Age 25-35 (Young, Long Timeline):

- 90% Roth / 10% Traditional

- Maximize tax-free growth decades

- Low current tax rate makes Roth cheap

Age 35-50 (Mid-Career):

- 70% Roth / 30% Traditional

- Still want tax-free growth

- Increasing income makes Traditional deduction valuable

Age 50-65 (Late Career, High Income):

- 50% Roth / 50% Traditional

- Traditional deduction valuable now

- Still want some tax-free growth

- Approaching retirement, flexibility matters

Age 65+ (Retired):

- Stop contributing

- Withdraw strategically from both

- Pay lowest total taxes

- Manage RMDs from Traditional

Frequently Asked Questions – FAQ 👈

Q: Can I have both Traditional and Roth IRAs?

A: Yes. You can split $7,000/year between them. Example: $4,000 Roth + $3,000 Traditional = $7,000 total.

Q: Can I convert Traditional IRA to Roth?

A: Yes. Called a Roth conversion. You pay taxes on the conversion but then enjoy tax-free growth. Many people do this strategically.

Q: What if I withdraw from Roth before age 59½?

A: Contributions come out tax and penalty-free. Earnings have 10% penalty + taxes (with exceptions). Contributions are always accessible.

Q: Do Traditional IRA contributions reduce my taxes?

A: Not always. If you’re covered by an employer retirement plan and make over the phase-out limit, deduction is partial or eliminated.

Q: What happens if I don’t take RMD from Traditional IRA?

A: 25% penalty on the amount you should have withdrawn (reduced to 10% if corrected). Plus you still owe income taxes.

Q: Can my spouse contribute to my IRA?

A: Not directly. But a working spouse can open a Spousal IRA for the non-working spouse.

Q: Which grows faster, Traditional or Roth?

A: Same growth rate inside account. The difference is the tax treatment of withdrawals, not the growth.

Q: Should I max out 401(k) first or IRA?

A: If employer matches 401(k), max that first (free money). Then max IRA. Then back to 401(k).

BONUS

Want to see detailed examples of how Roth and Traditional IRAs differ in real retirement scenarios?

This video shows side-by-side comparisons and helps you make the right choice:

FINAL THOUGHTS: The IRA Decision That Changes Your Life

Here’s what most people get wrong about this choice: They think it’s complicated.

It’s not.

It really comes down to one question: Do you want to pay taxes now or later?

If you’re young (decades until retirement), choose Roth. Lock in tax-free growth for 30+ years.

If you’re older or in high tax bracket, maybe split between both or emphasize Traditional.

If you genuinely don’t know future tax rates (nobody does), use both. Hedge your bets.

The real mistake isn’t choosing wrong between Roth and Traditional. The real mistake is not using either.

Too many people invest in taxable brokerage accounts and miss out on tax-deferred or tax-free growth entirely. That’s leaving free money on the table.

Your choice between Roth and Traditional isn’t between “perfect” and “wrong.” It’s between “good” and “really good.”

Both beat not investing at all. Both beat taxable accounts.

So open one. Or both. Just get started.

The sooner you start, the more compound interest works for you. Whether it’s in a Roth or Traditional account, tax-free growth for 30 years is transformative.

Make your choice. Open your account. Start contributing.

Your future self will thank you.

INTERESTING TOPICS

Ready to understand how compound interest multiplies your retirement wealth?

Want to discover how to choose your first investment inside an IRA?

Need to learn how to diversify your retirement portfolio across different assets?

Want more financial insights delivered to you? Subscribe to our newsletter

and get weekly articles with practical strategies to grow your wealth sent straight to your inbox.

Obs: Sign up for our newsletter and receive a free Finance For Beginner eBook.

Disclaimer: This article is for educational purposes only. Diversification does not guarantee profits or protect against all losses. Consider your financial situation, risk tolerance, and investment timeline before making investment decisions.

—— End of Article ——