Stocks vs Bonds: Which Should You Choose?

Last updated: January 2026

You have $10,000 to invest.

You could buy stocks—own a piece of companies that might grow dramatically but could also crash 30% tomorrow.

Or you could buy bonds—lend money to governments or corporations and get steady, predictable interest payments.

One offers excitement and growth potential. The other offers safety and stability.

But which one is right for YOU?

This is the question that stops most beginner investors in their tracks. Should you chase growth or prioritize safety? Should you bet on companies or lend money to them?

The truth is: The answer isn’t “stocks OR bonds”—it’s understanding how they work together.

Most successful investors don’t choose one over the other. They strategically combine both to build portfolios that survive market crashes while still capturing growth. The real wealth comes from understanding the differences, knowing when each works best, and building a balanced portfolio that matches your goals.

In this guide, you’ll discover exactly what stocks and bonds are, how they fundamentally differ, why experienced investors use both, how to decide which is right for your situation, and how to build a balanced portfolio using both assets.

By the end, you’ll stop seeing stocks and bonds as competitors and start seeing them as complementary tools in your wealth-building toolkit.

Let’s build your investment foundation.

What Are Stocks? (Complete Definition)

A stock is a share of ownership in a company.

When you buy stock, you become a partial owner of that business. You own a tiny piece of the company’s profits, assets, and future growth potential.

How Stocks Work

The Process:

Step 1: Company Issues Stock A company wants to raise money for expansion or operations. Instead of borrowing from a bank, it sells ownership shares to the public.

Step 2: You Buy Shares You purchase stock shares at the current market price. Each share represents a proportional ownership stake.

Step 3: You Own Part of the Company You’re now a shareholder. You own a tiny fraction of the company’s assets, profits, and decision-making power.

Step 4: Make Money Two Ways

Dividends: Some companies share profits with shareholders quarterly or annually Capital Appreciation: Stock price increases as company grows, you sell at higher price for profit

Real Example: Apple Stock

If Apple has 16 billion shares outstanding and you own 100 shares:

- You own 100/16,000,000,000 = 0.000000625% of Apple

- Tiny percentage, but real ownership

If Apple’s stock price:

- You bought at: $150/share

- Now trading at: $180/share

- Your 100 shares worth: $18,000 (up from $15,000)

- Your profit: $3,000 (20% gain)

Plus, if Apple pays $0.24/share dividend annually:

- You receive: 100 × $0.24 = $24/year in dividends

- Extra income on top of potential price appreciation

Key Stock Characteristics

Ownership: You own part of the company Income: Dividends (if company pays them) OR capital gains Volatility: Prices change daily, can be very volatile Growth Potential: Historically 10%+ annual returns long-term Voting Rights: You can vote on company decisions Risk: Can lose significant money if company struggles

What Are Bonds? (Complete Definition)

A bond is a loan you give to a company or government in exchange for regular interest payments.

When you buy a bond, you’re not owning anything. You’re lending money and getting paid interest for it. The bond issuer promises to pay you back on a specific date (maturity) plus interest along the way.

How Bonds Work

The Process:

Step 1: Company/Government Issues Bond They need to borrow money. Instead of going to a bank, they issue bonds to the public.

Step 2: You Buy the Bond You lend money at a specific interest rate. The bond specifies exactly how much you’ll be paid and when.

Step 3: You Receive Interest Payments Usually twice per year (semi-annually), the issuer pays you interest. This is called the coupon payment.

Step 4: Get Your Money Back On the maturity date (could be 2, 5, 10, or 30 years away), the issuer repays your principal in full.

Real Example: US Government Bond

You buy a 10-year US Treasury bond:

- Face Value (what you pay): $10,000

- Interest Rate (coupon): 4.5%

- Maturity: 10 years

What happens:

- Every year for 10 years: You receive $450 in interest ($10,000 × 4.5%)

- In year 10: You receive final $450 payment + $10,000 principal back

- Total interest collected: $4,500 on your $10,000 investment

- Your return: 4.5% annually, guaranteed

Key Bond Characteristics

Lending: You lend money, don’t own anything Income: Fixed interest payments, very predictable Volatility: Prices can change, but less volatile than stocks Return Potential: Historically 4-6% annual returns Safety: Generally safer than stocks (especially government bonds) Maturity Date: Money returned on a specific date Risk: Lower risk, but risk depends on bond issuer (government vs corporation)

Key Differences: Stocks vs Bonds

Let’s compare them directly across important dimensions:

Ownership vs Lending

Stocks:

- You OWN part of the company

- You’re an owner/shareholder

- You share in profits and losses

Bonds:

- You LEND money to company/government

- You’re a creditor

- You receive fixed payments regardless of company performance

Income: Dividends/Growth vs Interest

Stocks:

- Dividends (occasional, variable, not guaranteed)

- Capital appreciation (stock price going up)

- Income NOT guaranteed

- Total return varies widely

Bonds:

- Fixed interest payments (very predictable)

- Regular income every 6 months or annually

- Income is contractually guaranteed

- Total return predictable

Price Volatility

Stocks:

- Highly volatile

- Can swing 5-10% in a single day

- Prices reflect company performance and investor sentiment

- Example: Stock worth $100 today, $85 tomorrow, $120 next week

Bonds:

- Much less volatile

- Prices change gradually

- Less affected by daily sentiment

- Example: Bond value stays relatively stable until maturity

Historical Returns

Stocks:

- Long-term average: 10% annually

- But with significant volatility

- Best returns over 20+ year periods

- Short-term can be very unpredictable

Bonds:

- Long-term average: 4-6% annually

- Much more predictable

- Steady income regardless of market conditions

- Lower but more reliable returns

Risk Level

Stocks:

- Higher risk

- Can lose 50%+ of investment in severe market downturn

- Company could go bankrupt (you lose everything)

- Suitable for long-term investors with high risk tolerance

Bonds:

- Lower risk

- Usually lose only 10-20% in extreme crisis

- Government bonds nearly risk-free

- Suitable for conservative investors or near-retirees

Time Horizon

Stocks:

- Best for 10+ year timeframes

- Short-term volatility evens out over decades

- Need patience to weather downturns

- Optimal for wealth building over time

Bonds:

- Good for any timeframe

- Short-term investors can use them safely

- Shorter maturity bonds especially safe short-term

- Optimal for near-term income needs

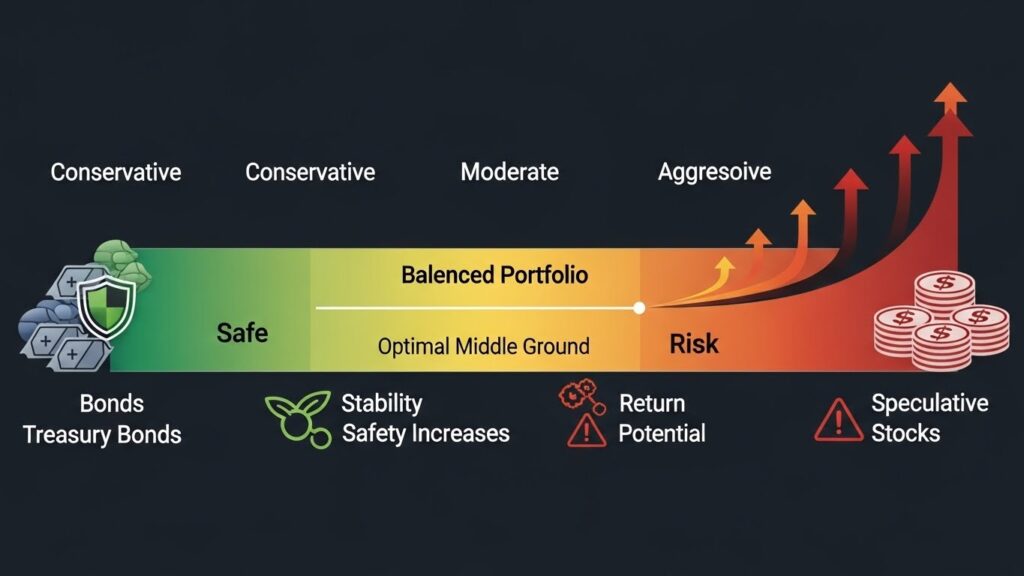

Risk Comparison: Understanding the Trade-offs

The Risk-Return Spectrum

Lower Risk ← → Higher Risk

Bonds: Lower risk, Lower return Balanced Portfolio: Medium risk, Medium return Stocks: Higher risk, Higher return Speculative Stocks: Highest risk, Highest potential return

Scenario: Market Crash

Your $100,000 Portfolio

100% Stocks Portfolio:

- Market crashes 40%

- Your portfolio: $60,000

- Loss: $40,000 (40%)

- Recovery time: 3-7 years typically

- Emotional difficulty: VERY HIGH

70% Stocks / 30% Bonds Portfolio:

- Stocks down 40%, Bonds down 5%

- Stock portion: $70,000 × 0.6 = $42,000

- Bond portion: $30,000 × 0.95 = $28,500

- Total: $70,500

- Loss: $29,500 (29.5%)

- Recovery time: 2-4 years

- Emotional difficulty: MODERATE

100% Bonds Portfolio:

- Market crashes 40%, Bonds down 5%

- Your portfolio: $95,000

- Loss: $5,000 (5%)

- Recovery time: <1 year

- Emotional difficulty: LOW

The Trade-off is Clear:

More stocks = bigger crashes but faster long-term growth More bonds = smaller crashes but slower wealth building

The Real Risk: Missing Growth

Here’s what people don’t understand:

If you’re 30 years old and need money at 65, being 100% in bonds is actually RISKY because:

- You won’t grow wealth fast enough

- Inflation erodes your purchasing power

- You may not have enough for retirement

Being 100% in stocks is also risky because:

- You might panic-sell in crash near retirement

- You could be devastated by market downturn before you need the money

The real answer: Balance based on your timeline and risk tolerance.

Return Potential: What History Shows

Historical Annual Returns (1926-2024)

US Stocks: 10.0% average annual return

- Range: -37% to +54% in individual years

- Best 10-year period: 19.4% annually

- Worst 10-year period: 0.5% annually

US Bonds: 5.3% average annual return

- Range: -8% to +40% in individual years

- Best 10-year period: 14.2% annually

- Worst 10-year period: 0.2% annually

Combined 60/40 Portfolio: 8.6% average annual return

- Much more stable than pure stocks

- Still captures significant growth

- Smoother ride with better sleep at night

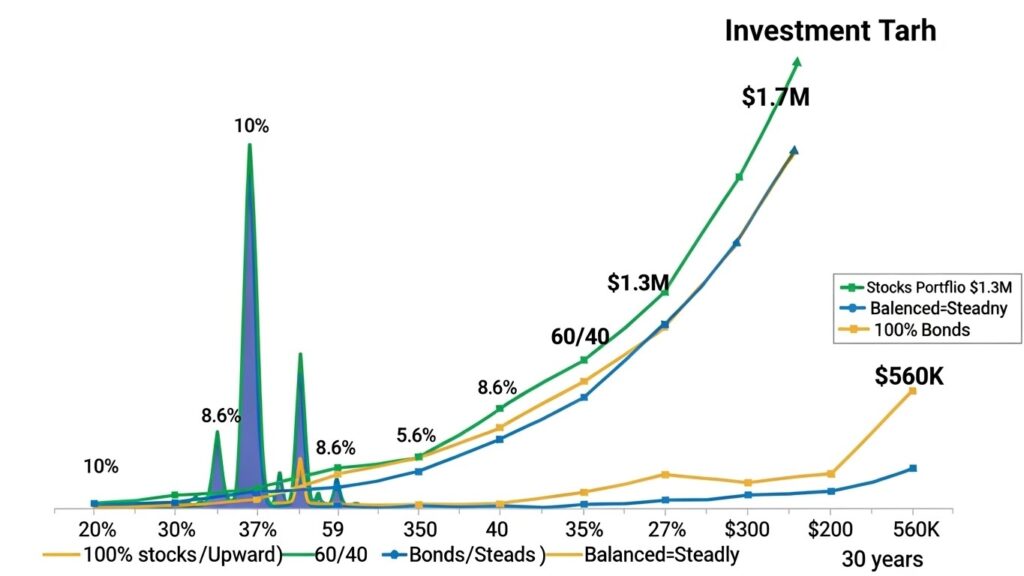

Long-Term Wealth Building

Scenario: $100,000 invested for 30 years

100% Stocks at 10% return:

- Final value: $1,744,000

- Growth: 1,644%

- But volatile journey

60% Stocks / 40% Bonds at 8.6% return:

- Final value: $1,329,000

- Growth: 1,229%

- Smoother journey, less stress

100% Bonds at 5.3% return:

- Final value: $563,000

- Growth: 463%

- Stable but slower

The difference is real, but all three become substantial wealth.

What This Teaches Us

Over long periods, stocks win on total return. But bonds reduce volatility and stress, making it easier to stay invested through market crashes.

Tax Implications: How Each Is Taxed

Stock Taxation

Dividends:

- Qualified dividends: Taxed at capital gains rates (0%, 15%, or 20%)

- Non-qualified dividends: Taxed as ordinary income (up to 37%)

Capital Gains:

- Long-term (held 1+ year): Capital gains rates (0%, 15%, 20%)

- Short-term (held <1 year): Ordinary income rates (up to 37%)

Tax Advantage: Long-term capital gains are often taxed less than ordinary income

Bond Taxation

Interest Income:

- Regular bonds: Taxed as ordinary income (up to 37%)

- Municipal bonds: Often tax-free

- US Treasury: Federal tax only, no state tax

Price Changes:

- If you sell before maturity at profit: Capital gains treatment

- If you sell at loss: Capital loss (can offset gains)

Tax Disadvantage: Bond interest is taxed as ordinary income, usually higher rate than stock dividends

Tax-Smart Strategy

In Taxable Account:

- Hold stocks (better tax treatment)

- Hold growth stocks (no dividends = no annual taxes)

In Retirement Account (Roth IRA, 401k):

- Hold bonds (interest is tax-free inside retirement account)

- All gains grow tax-free

Tax-Loss Harvesting:

- Sell losing positions to offset gains

- More effective with stocks/bonds mix

When to Choose Stocks

Choose stocks if:

✅ You have 10+ year time horizon

- Gives time to recover from crashes

- Volatility becomes your friend (buy low opportunities)

✅ You have high risk tolerance

- Can handle 40%+ portfolio swings

- Won’t panic-sell in crashes

- Sleep well during volatility

✅ You have steady income

- Can buy during crashes (dollar-cost averaging)

- Don’t need to withdraw for 10+ years

✅ You want maximum long-term growth

- Historically 10% annual returns

- Best for building substantial wealth

✅ Your financial goal is ambitious

- Need significant wealth in 20+ years

- Bonds alone won’t get you there

Best stock vehicles for beginners:

- Index funds and ETFs (diversified, low-cost)

- Dividend growth stocks (income + growth)

- Diversified portfolio (multiple holdings)

When to Choose Bonds

Choose bonds if:

✅ You need money within 5 years

- Stocks too risky for short timeframe

- Bonds preserve capital

- Predictable returns

✅ You have low risk tolerance

- Can’t handle 40%+ swings

- Need stable, predictable income

- Prefer sleep over wealth-building

✅ You’re near retirement

- Don’t want to risk crash near withdrawal date

- Need stable income stream

- Capital preservation important

✅ You want steady income NOW

- Bonds pay regular interest

- Stocks may not pay dividends

- Predictable cash flow

✅ You want portfolio stability

- Bonds act as shock absorbers

- Reduce volatility dramatically

- Sleep better at night

Best bond types for beginners:

- US Treasury Bonds (safest)

- Investment-Grade Corporate Bonds (good balance)

- Bond ETFs (diversified, easy to buy)

- I-Bonds (inflation protection)

For detailed information on Treasury bonds and current interest rates, visit the official US government portal.

The Power of Combining Both (Asset Allocation)

Here’s the secret most beginners miss: You don’t choose stocks OR bonds. You choose a mix.

The percentage split depends on:

- Your age

- Your risk tolerance

- Your time horizon

- Your financial goals

- Your income stability

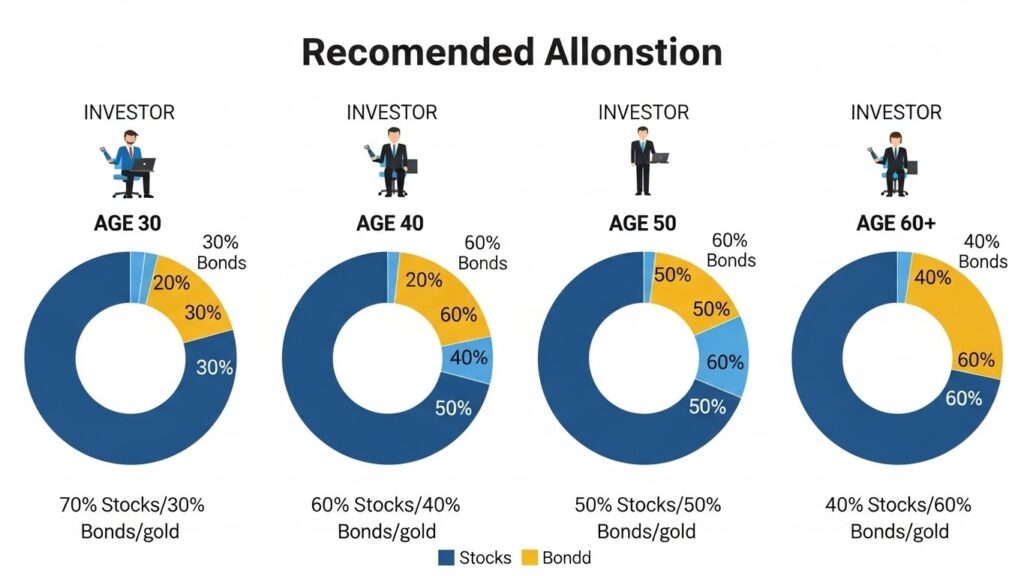

Common Asset Allocation Models

Aggressive (Age 25-35, Long Time Horizon)

- 90% Stocks / 10% Bonds

- Maximize growth, weather crashes easily

- Example: 90/10 portfolio

Moderate (Age 35-50, Medium Time Horizon)

- 70% Stocks / 30% Bonds

- Balance growth and stability

- Example: 70/30 or 60/40 portfolio

Conservative (Age 50+, Shorter Time Horizon)

- 50% Stocks / 50% Bonds

- Emphasize stability, some growth

- Example: 50/50 portfolio

Very Conservative (Age 60+, Near Retirement)

- 30% Stocks / 70% Bonds

- Capital preservation, steady income

- Example: 30/70 portfolio

Why This Works

During Bull Markets:

- Stocks grow dramatically

- Bonds stay stable

- Portfolio grows overall

During Bear Markets (Crashes):

- Stocks crash 40%

- Bonds actually GAIN (prices rise when stocks fall)

- Portfolio declines less than pure stocks

- You don’t panic-sell

During Recovery:

- Stocks rebound powerfully

- Bonds provide stability floor

- You have capital to benefit from recovery

The real magic: When stocks crash, bonds often rise.

They move opposite directions, creating balance.

How to Build a Balanced Portfolio

Step 1: Determine Your Asset Allocation

Ask yourself:

- How old are you?

- When do you need this money?

- How would you feel if portfolio dropped 30%?

- Can you sleep at night with volatility?

- Do you have steady income to buy during crashes?

Simple Rule of Thumb:

- Age 30: 70% stocks / 30% bonds

- Age 40: 60% stocks / 40% bonds

- Age 50: 50% stocks / 50% bonds

- Age 60: 40% stocks / 60% bonds

Adjust based on risk tolerance (conservative = more bonds, aggressive = more stocks)

Step 2: Choose Your Investment Vehicles

For Stocks:

- Broad index funds (S&P 500)

- Diversified ETFs

- Individual dividend stocks (if you want to pick)

For Bonds:

- Bond index funds

- Individual bonds (Treasury, Corporate)

- Bond ETFs

Easiest beginner approach:

- 70% in VTI or SPLG (stock index)

- 30% in BND or AGG (bond index)

- Done. Automatic diversification

Step 3: Implement Your Portfolio

If you have $10,000:

- $7,000 into stock index fund

- $3,000 into bond index fund

- Set and forget

Add monthly:

- $700 into stocks

- $300 into bonds

- Automatic dollar-cost averaging

Step 4: Rebalance Annually

Stocks outperformed?

- Now 75% stocks / 25% bonds

- Sell some stocks, buy bonds

- Return to target allocation

Bonds outperformed?

- Now 65% stocks / 35% bonds

- Sell some bonds, buy stocks

- Return to target allocation

This forces you to buy low and sell high automatically.

Real-Life Examples: Different Investor Scenarios

Scenario 1: Jessica, Age 28, $50,000 to Invest

Profile:

- 37 years until retirement

- High risk tolerance

- Steady software engineer salary

- Can buy during crashes

Allocation: 85% Stocks / 15% Bonds

- $42,500 in stock index fund

- $7,500 in bond index fund

Expected:

- ~9% annual return historically

- Volatility: high (35-40% swings possible)

- But 37 years to recover and grow

- Projected retirement portfolio: $2.3+ million

Rationale: Young, long timeframe, can weather crashes, wants maximum growth

Scenario 2: Michael, Age 45, $100,000 to Invest

Profile:

- 20 years until retirement

- Moderate risk tolerance

- Concerned about 2008-style crash

- Can’t easily add more money

Allocation: 60% Stocks / 40% Bonds

- $60,000 in stock index fund

- $40,000 in bond index fund

Expected:

- ~8.4% annual return historically

- Volatility: moderate (20-25% swings possible)

- Bond cushion helps during crashes

- Projected retirement portfolio: $463,000 to retirement

Rationale: Mid-career, need some growth but can’t afford big crash, bonds provide stability

Scenario 3: Sarah, Age 62, $300,000 to Invest

Profile:

- 3 years until retirement

- Low risk tolerance

- Will need income from portfolio soon

- Experienced 2008 crash (traumatized)

Allocation: 30% Stocks / 70% Bonds

- $90,000 in stock index fund

- $210,000 in bond index fund

Expected:

- ~6.2% annual return historically

- Volatility: low (5-10% swings)

- Can generate ~$12,600/year bond income

- Projected retirement portfolio: $340,000+ (income stream)

Rationale: Near retirement, capital preservation critical, steady income needed, can’t afford big crash

Frequently Asked Questions – FAQ 👈

Q: Can I just pick one or the other?

A: You CAN, but it’s not optimal. Stocks alone means high volatility and potential for panic-selling. Bonds alone means insufficient growth for long-term wealth. The combination works better than either alone.

Q: Which is better for beginners?

A: A balanced portfolio (60/40 or 70/30) is best for beginners. It removes the “all-or-nothing” pressure and lets you learn while staying invested through market conditions.

Q: What if I’m wrong about my risk tolerance?

A: Most people discover their TRUE risk tolerance during market crashes. If you chose 80% stocks and panic during a 35% crash, you learned you need more bonds. Adjust and move forward. This is normal.

Q: How often should I rebalance?

A: Once annually is perfect. Don’t rebalance every month (creates taxes and trading costs). Annually keeps allocation on track.

Q: Are bonds boring?

A: Bonds ARE boring—that’s their job. They’re supposed to be stable and predictable. Exciting investments usually mean higher risk. Let stocks be exciting; let bonds be boring and stable.

Q: What if interest rates rise?

A: Bond prices fall when rates rise (you want to buy then, cheap bonds). Stock prices might rise (companies healthier). This is when diversification shines.

Q: Can I use both in my retirement account?

A: Absolutely. In a Roth IRA or 401(k), tax efficiency matters less, so bonds actually work well there (their interest grows tax-free inside the account). The SEC provides comprehensive information and resources on stocks and bonds for beginner investors.

Q: What about inflation? Will bonds keep up?

A: Regular bonds don’t. But Treasury I-Bonds adjust automatically for inflation. Stocks historically beat inflation. Balanced portfolio beats inflation better than bonds alone.

Your Stock-Bond Strategy

Here’s your action plan to build a balanced portfolio:

This Week

Day 1: Determine your risk tolerance

- Would a 30% portfolio drop stress you?

- How many years until you need this money?

- Can you buy during crashes or must you sell?

Day 2: Calculate your target allocation

- Use age-based rule or risk tolerance assessment

- Decide on your stocks/bonds split

- Write it down (your target allocation)

Day 3: Choose your vehicles

- Decide: index funds, individual stocks, or mix?

- Decide: individual bonds or bond funds?

- Research: lowest-cost options in your brokerage

Day 4: Open account (if needed) and fund it

- Open brokerage account

- Transfer money in

- Keep it in cash for now

Day 5: Make your first purchase

- Buy stock allocation (index fund preferred)

- Buy bond allocation

- Enable DRIP if available

This Month

- Research dividend stocks if interested in individual picks

- Learn about ETFs for easier diversification

- Set up automatic monthly investments

- Create a one-page plan document

This Year

- Build consistency (invest same amount monthly)

- Stop checking portfolio daily (quarterly is enough)

- Monitor allocation drift

- Rebalance once annually

- Let compound interest work

Long-Term (5-20+ Years)

- Stay the course through market crashes

- Rebalance annually

- Increase contributions when possible

- Adjust allocation as you age

- Watch your balanced portfolio grow steadily

BONUS

Want to see real examples of how stocks and bonds behave differently during market conditions?

This video breaks down the fundamentals and shows why combining both creates powerful portfolios:

FINAL THOUGHTS: Stocks AND Bonds, Not Stocks OR Bonds

Here’s what most beginners get wrong: They see stocks and bonds as competitors fighting for their money.

The truth is different: They’re dance partners.

Stocks are the growth engine. They multiply your wealth over decades. They’re essential for building real, substantial wealth.

Bonds are the shock absorber. They cushion crashes, provide stability, and let you sleep at night. They’re essential for not panic-selling when stocks crash.

Neither works perfectly alone. Together, they’re powerful.

The wealthy don’t debate stocks vs bonds. They use both strategically.

Your age, your timeline, your goals—these determine the right mix. A 25-year-old and a 60-year-old should have dramatically different allocations. That’s not a bug; that’s the entire point.

The math is simple:

- Young + Long timeline: More stocks (growth matters more than stability)

- Middle-aged + Medium timeline: Balanced (growth and stability both matter)

- Near retirement + Short timeline: More bonds (stability matters most)

Your job is simple:

- Choose your allocation (based on age and risk tolerance)

- Pick low-cost vehicles (index funds for both stocks and bonds)

- Invest consistently (same amount every month)

- Rebalance annually (return to target allocation)

- Stay the course (don’t panic in crashes)

That’s it. That’s the entire strategy that builds lasting wealth.

Your balanced portfolio won’t make you rich overnight. But over 20, 30, 40 years? It compounds into serious, life-changing wealth.

The question isn’t stocks OR bonds. The question is: What’s the right balance for YOUR situation?

Once you answer that, you have your investing roadmap.

INTERESTING TOPICS

Ready to understand compound interest and how time multiplies your returns?

Want to learn how to diversify your portfolio across multiple assets and sectors?

Need to discover which ETFs are perfect for your stock and bond allocation?

Want more financial insights delivered to you? Subscribe to our newsletter

and get weekly articles with practical strategies to grow your wealth sent straight to your inbox.

Obs: Sign up for our newsletter and receive a free Finance For Beginner eBook.

Disclaimer: This article is for educational purposes only. Diversification does not guarantee profits or protect against all losses. Consider your financial situation, risk tolerance, and investment timeline before making investment decisions.

—— End of Article ——