Understanding Risk Tolerance in Investing: Find Your Perfect Investment Strategy

Last updated: January 2026

Imagine two investors, both 30 years old with the same income and savings. The stock market drops 30% overnight. One investor panics, sells everything, and locks in massive losses. The other stays calm, continues investing, and eventually recovers and profits. What’s the difference? Risk tolerance.

Risk tolerance is your ability—both financially and emotionally—to handle investment losses without panicking or making terrible decisions. It’s the difference between building wealth through decades of consistent investing and sabotaging your financial future by selling at the worst possible time.

Yet most investors never properly assess their risk tolerance. They invest too aggressively and panic during downturns, or too conservatively and miss out on decades of growth. Either way, they fail to reach their financial goals not because of bad luck or market crashes, but because their investment strategy doesn’t match who they are.

In this guide, you’ll learn exactly what risk tolerance is, how to accurately assess yours, how it should guide your investment decisions, how to adjust your strategy as you age, and the costly mistakes people make by misjudging their tolerance for risk. By the end, you’ll know your risk profile and exactly how to build a portfolio that lets you sleep at night while still growing your wealth.

Let’s find your perfect investment strategy.

What is Risk Tolerance? (Clear Definition)

Risk tolerance is your psychological and financial ability to endure investment losses and market volatility without making emotional, detrimental decisions like panic-selling or abandoning your investment strategy.

In simple terms: How much can your portfolio drop in value before you lose sleep, panic, or sell at the worst possible time?

Two Components of Risk Tolerance:

1. Emotional/Psychological Tolerance:

- How you FEEL when investments drop

- Your anxiety level during market crashes

- Whether you can stay disciplined through volatility

- Your personality and temperament

2. Financial Tolerance (Risk Capacity):

- How much loss you can AFFORD

- Your income stability

- Time until you need the money

- Your overall financial situation

Both matter. You might financially afford a 40% loss, but if it causes so much anxiety that you sell at the bottom, your actual tolerance is lower.

Why Risk Tolerance Matters:

Scenario 1: Mismatched (too aggressive)

- Conservative investor puts 100% in stocks

- Market drops 30%

- Panics and sells at the bottom

- Misses the recovery

- Returns to cash and never invests again

- Result: Destroyed wealth

Scenario 2: Mismatched (too conservative)

- Young investor with 40 years until retirement

- Keeps 80% in bonds, 20% in stocks

- Avoids volatility successfully

- But grows wealth far slower than necessary

- Retires with 40% less than if properly invested

- Result: Missed opportunity

Scenario 3: Properly matched

- Investor chooses allocation that fits tolerance

- Market drops 25%

- Feels uncomfortable but stays invested

- Continues dollar-cost averaging

- Recovers and prospers

- Result: Long-term success

The Three Types of Risk Tolerance

Most investors fall into one of three categories:

Conservative (Low Risk Tolerance)

Characteristics:

- Cannot tolerate seeing portfolio value drop significantly

- Loses sleep over market volatility

- Would rather earn less if it means more stability

- Panics easily during market downturns

- Values preservation over growth

Emotional response to 20% market drop:

- Extreme anxiety and stress

- Constantly checks portfolio

- Considers or actually sells to “stop the bleeding”

- Can’t focus on work or life

Typical allocation:

- 30-50% stocks

- 50-70% bonds/cash

- Heavy emphasis on stability

Who fits this profile:

- Older investors near retirement

- People with unstable income

- Those who’ve experienced severe losses before

- Naturally anxious personalities

- First-time investors

Moderate (Medium Risk Tolerance)

Characteristics:

- Can handle some volatility but not extreme swings

- Uncomfortable with losses but doesn’t panic immediately

- Wants growth but also some stability

- Can stay invested through moderate downturns

- Balances growth and safety

Emotional response to 20% market drop:

- Uncomfortable and concerned

- Checks portfolio more often than usual

- Considers selling but ultimately doesn’t

- Sleeps okay but worries somewhat

Typical allocation:

- 60-70% stocks

- 30-40% bonds

- Balanced approach

Who fits this profile:

- Middle-aged investors (40s-50s)

- People with 10-20 years until retirement

- Those with moderate income stability

- Balanced personalities

- Most average investors

Aggressive (High Risk Tolerance)

Characteristics:

- Can handle extreme volatility without panic

- Views market drops as buying opportunities

- Prioritizes maximum growth over stability

- Remains calm during crashes

- Willing to accept significant losses for higher potential returns

Emotional response to 20% market drop:

- Relatively calm or even excited

- Sees opportunity to invest more

- Doesn’t consider selling

- Sleeps fine

- Focused on long-term

Typical allocation:

- 80-100% stocks

- 0-20% bonds

- Maximum growth focus

Who fits this profile:

- Young investors (20s-30s)

- Long time horizons (20+ years)

- High income or high emergency fund

- Experienced investors

- Naturally calm temperaments

- Growth-focused mindset

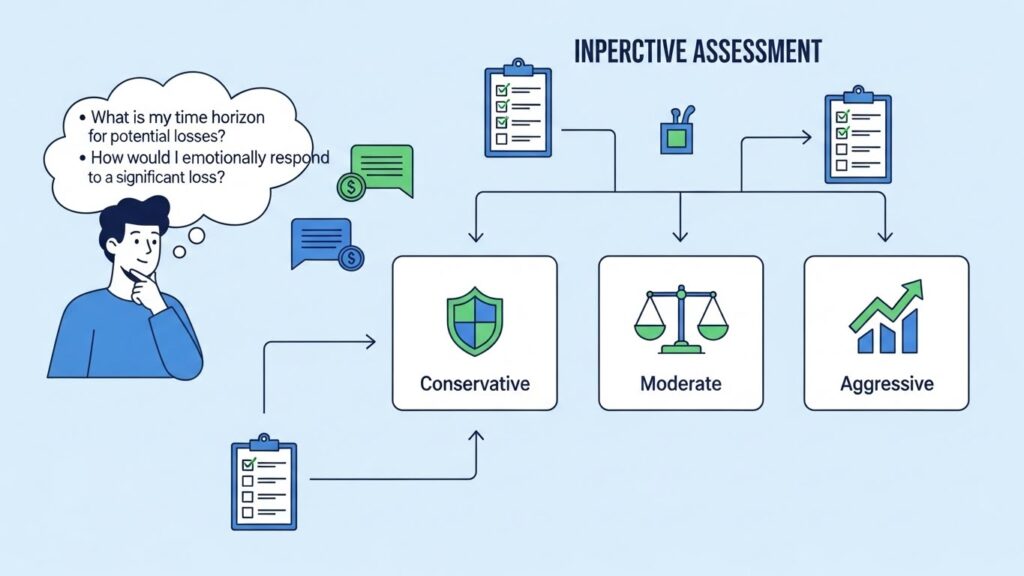

How to Assess Your Risk Tolerance Accurately

Most people misjudge their risk tolerance. Here’s how to assess yours accurately:

Method 1: The Hypothetical Loss Test

Ask yourself:

“If my $10,000 investment dropped to $7,000 (30% loss) tomorrow, I would:”

A) Panic and sell immediately → Conservative tolerance

B) Feel very uncomfortable, consider selling, but probably hold → Moderate tolerance

C) Feel uncomfortable but stay calm, might even invest more → Moderate-aggressive tolerance

D) View it as a buying opportunity and definitely invest more → Aggressive tolerance

Method 2: The Sleep Test

Ask yourself:

“What’s the maximum portfolio drop I could experience and still sleep soundly?”

– 5-10% drop: Conservative – 10-20% drop: Moderate-conservative – 20-30% drop: Moderate – 30-40% drop: Moderate-aggressive – 40%+ drop: Aggressive

Method 3: Historical Scenario Test

Look at actual historical crashes and honestly assess your reaction:

2008 Financial Crisis: S&P 500 dropped 57%

- $10,000 became $4,300

- Took 4 years to recover

Your honest reaction would be:

- Sell immediately = Conservative

- Hold but suffer greatly = Moderate-conservative

- Hold uncomfortably but okay = Moderate

- Hold calmly = Moderate-aggressive

- Buy more aggressively = Aggressive

2020 COVID Crash: S&P 500 dropped 34% in one month

- $10,000 became $6,600

- Recovered in 5 months

Your honest reaction:

- Sell in panic = Conservative

- Hold with anxiety = Moderate-conservative

- Hold steadily = Moderate

- Hold confidently = Moderate-aggressive

- Invest more = Aggressive

Method 4: Past Behavior Analysis

The most accurate predictor: How did you ACTUALLY behave?

Think back to the most recent market volatility you experienced:

Did you:

- Panic-sell or seriously consider it? → Conservative

- Hold but check portfolio obsessively? → Moderate-conservative

- Hold and check occasionally? → Moderate

- Hold without much concern? → Moderate-aggressive

- Invest more aggressively? → Aggressive

If you’ve never experienced a downturn: You won’t truly know your tolerance until you do. Start conservatively and adjust.

Method 5: The Comprehensive Questionnaire

Answer honestly (1-5 scale):

- Time horizon: When do you need this money?

- 1 = Less than 5 years

- 5 = More than 20 years

- Financial stability: How stable is your income?

- 1 = Very unstable

- 5 = Very stable

- Emergency fund: Months of expenses saved?

- 1 = Less than 3 months

- 5 = 12+ months

- Investment experience: How experienced are you?

- 1 = Complete beginner

- 5 = Very experienced

- Emotional response: How do you handle stress?

- 1 = Panic easily

- 5 = Very calm under pressure

- Priority: Growth vs safety?

- 1 = Safety first

- 5 = Maximum growth

- Recovery time: Could you recover from major losses?

- 1 = No, would devastate me

- 5 = Yes, I have time/income to recover

Total Score:

- 7-14 points: Conservative tolerance

- 15-21 points: Moderate-conservative tolerance

- 22-28 points: Moderate tolerance

- 29-35 points: Aggressive tolerance

How Risk Tolerance Should Guide Your Investment Strategy

Your risk tolerance should directly determine your asset allocation:

For Conservative Investors:

Stock/Bond Allocation: 30-40% stocks, 60-70% bonds

Investment approach:

- Focus on stability and income

- Heavy bond allocation for steady returns

- Lower volatility portfolio

- Accept lower long-term returns for peace of mind

Specific investments:

- Total bond market index funds

- High-quality corporate bonds

- Treasury bonds

- Dividend-paying blue-chip stocks (small portion)

- REITs for income (small portion)

Example portfolio (Conservative):

- 30% Total U.S. Stock Market

- 10% International Stocks

- 50% Total Bond Market

- 10% Cash/Money Market

Expected returns: 4-6% annually over long term

Expected volatility: Low (10-15% maximum drops typically)

For Moderate Investors:

Stock/Bond Allocation: 60-70% stocks, 30-40% bonds

Investment approach:

- Balance growth and stability

- Can handle moderate volatility

- Reasonable growth with downside protection

- Classic balanced approach

Specific investments:

- Diversified stock index funds

- Total market funds

- Bond funds for stability

- Some international exposure

Example portfolio (Moderate):

- 50% Total U.S. Stock Market

- 20% International Stocks

- 25% Total Bond Market

- 5% REITs or other

Expected returns: 6-8% annually over long term

Expected volatility: Moderate (20-30% drops possible)

For Aggressive Investors:

Stock/Bond Allocation: 80-100% stocks, 0-20% bonds

Historical market data supports these long-term return expectations for equity-heavy portfolios.

Investment approach:

- Maximum growth focus

- Accept high volatility

- Long time horizon

- Comfortable with significant temporary losses

Specific investments:

- Heavy stock allocation

- Total market or S&P 500 funds

- International stocks

- Minimal or no bonds

- Possibly small-cap or growth tilts

Example portfolio (Aggressive):

- 60% Total U.S. Stock Market

- 30% International Stocks

- 10% Small-Cap or Emerging Markets

- 0% Bonds

Expected returns: 8-10% annually over long term

Expected volatility: High (30-50% drops possible)

The Key Principle:

Your allocation should let you:

- Sleep at night during downturns

- Stay invested through volatility

- Avoid panic-selling

- Continue regular contributions

If you can’t do all four, your allocation is too aggressive.

Risk Tolerance vs Risk Capacity: Understanding the Difference

Many people confuse these two concepts:

Risk Tolerance (Psychological)

What it is: Your emotional ability to handle losses

Question it answers: “Can I EMOTIONALLY handle a 30% drop without panicking?”

Determined by:

- Personality and temperament

- Investment experience

- Past reactions to volatility

- Anxiety levels

- Comfort with uncertainty

Example: A wealthy person might still have low risk tolerance if market drops cause extreme anxiety.

Risk Capacity (Financial)

What it is: Your financial ability to absorb losses

Question it answers: “Can I FINANCIALLY afford a 30% loss and still meet my goals?”

Determined by:

- Time horizon (when you need the money)

- Income stability

- Emergency fund size

- Overall financial situation

- Ability to recover from losses

Financial advisors recommend evaluating both risk tolerance and capacity before making investment decisions.

Example: A young person with 40 years until retirement has high risk capacity regardless of their emotional tolerance.

The Four Scenarios:

Scenario 1: High Tolerance + High Capacity

- Best situation

- Invest aggressively (80-100% stocks)

- Example: 25-year-old with stable job, calm temperament

Scenario 2: High Tolerance + Low Capacity

- Risky situation – capacity wins

- Invest more conservatively than tolerance suggests

- Example: 60-year-old retiring in 2 years who claims to be comfortable with risk

Scenario 3: Low Tolerance + High Capacity

- Common situation – tolerance wins

- Invest more conservatively than capacity allows

- Example: 28-year-old with 40 years until retirement but anxious personality

Scenario 4: Low Tolerance + Low Capacity

- Most conservative situation

- Invest very conservatively (40-50% stocks maximum)

- Example: 62-year-old retiring in 3 years with anxiety about markets

The Rule:

Always choose the MORE CONSERVATIVE of the two.

If your tolerance says “aggressive” but your capacity says “moderate,” choose moderate.

If your capacity says “aggressive” but your tolerance says “conservative,” choose conservative.

Why: You can’t make good investment decisions if you’re panicking. Better to grow slower than to panic-sell and destroy your wealth.

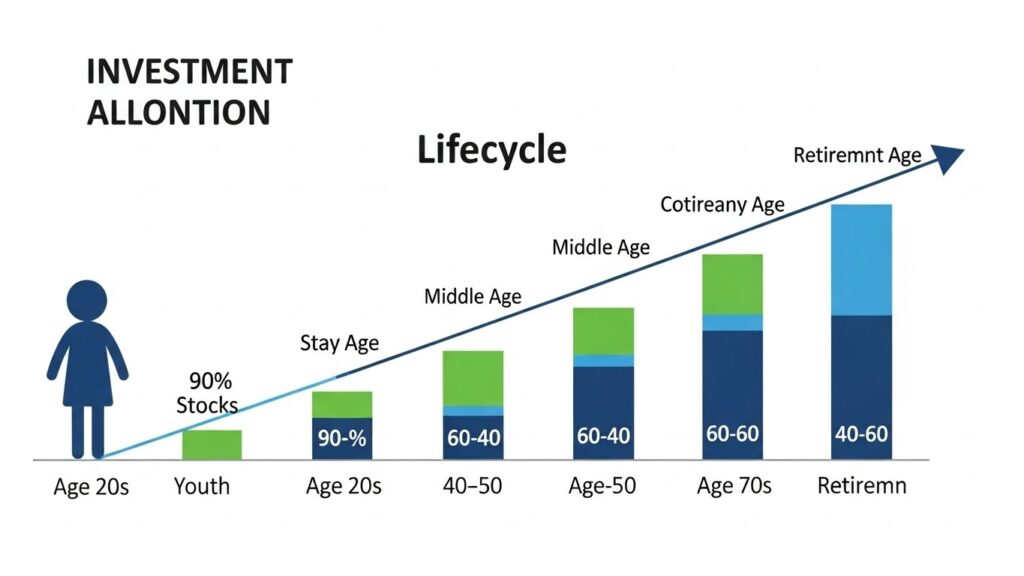

How Risk Tolerance Changes with Age and Life Stages

Your risk tolerance should evolve throughout your life:

In Your 20s:

Typical situation:

- 40+ years until retirement

- High risk capacity (time to recover)

- Often high risk tolerance (less to lose)

- Limited savings but high earning potential ahead

Recommended allocation:

- 90-100% stocks

- 0-10% bonds

- Maximum growth focus

Why: You have decades to recover from crashes. Time is your greatest asset. Even if markets crash 50%, you have 40 years for recovery and growth.

Example: 100% in total stock market index fund

In Your 30s:

Typical situation:

- 30-35 years until retirement

- Still high risk capacity

- More to lose but still long timeline

- Higher income, building wealth

Recommended allocation:

- 80-90% stocks

- 10-20% bonds

- Growth focus with tiny buffer

Why: Still plenty of time for recovery. You’re accumulating wealth rapidly. Don’t slow growth too early.

Example:

- 70% U.S. stocks

- 20% international stocks

- 10% bonds

In Your 40s:

Typical situation:

- 20-25 years until retirement

- Moderate risk capacity

- Significant assets accumulated

- Peak earning years

Recommended allocation:

- 70-80% stocks

- 20-30% bonds

- Balanced growth and some protection

Why: Still time to recover but getting closer to retirement. Start adding some stability without sacrificing too much growth.

Example:

- 50% U.S. stocks

- 20% international stocks

- 25% bonds

- 5% other

In Your 50s:

Typical situation:

- 10-15 years until retirement

- Lower risk capacity (less recovery time)

- Usually lower risk tolerance (more to lose)

- Preserving accumulated wealth becomes priority

Recommended allocation:

- 60-70% stocks

- 30-40% bonds

- Shift toward stability

Why: You no longer have decades to recover from crashes. A 50% loss at age 55 is devastating. Protect what you’ve built while still growing.

Example:

- 40% U.S. stocks

- 20% international stocks

- 35% bonds

- 5% cash

In Your 60s (At/Near Retirement):

Typical situation:

- 0-10 years until retirement

- Low risk capacity (need money soon)

- Often lower risk tolerance (lifetime of savings at stake)

- Transition from accumulation to preservation

Recommended allocation:

- 40-60% stocks

- 40-60% bonds

- Heavy focus on stability and income

Why: You’re about to start withdrawing. Can’t afford major crash right before or during early retirement.

Example:

- 30% U.S. stocks

- 15% international stocks

- 50% bonds

- 5% cash

In Retirement (70+):

Typical situation:

- Withdrawing from portfolio

- Low risk capacity

- Need income and stability

- Still need some growth (could live 20-30+ more years!)

Recommended allocation:

- 30-50% stocks (yes, still some!)

- 50-70% bonds

- Income and preservation focus

Why: You still need growth to combat inflation over potentially decades of retirement. But stability is paramount.

Example:

- 30% U.S. stocks (for growth)

- 60% bonds (for stability and income)

- 10% cash (for immediate needs)

The Traditional Rule of Thumb:

“Your age in bonds”

- Age 30 = 30% bonds, 70% stocks

- Age 50 = 50% bonds, 50% stocks

- Age 70 = 70% bonds, 30% stocks

Modern adjustment: Subtract 10-20 from your age

- Age 30 = 10-20% bonds, 80-90% stocks

- Age 50 = 30-40% bonds, 60-70% stocks

- Age 70 = 50-60% bonds, 40-50% stocks

Why the adjustment: People live longer now. Need more growth to last 30+ years in retirement.

Common Risk Tolerance Mistakes That Cost Money

Mistake 1: Overestimating Your Risk Tolerance

The error: “I can handle any volatility! 100% stocks!”… until the first 20% drop.

What happens:

- Market drops 25%

- Investor panics despite previous confidence

- Sells at the bottom

- Misses recovery

- Never fully reinvests

Real example: 2008 crash. Many “aggressive” investors discovered they couldn’t actually handle 50% losses.

The fix: Be brutally honest. If you’ve never experienced a crash, start more conservative than you think necessary. You can always become more aggressive later.

Mistake 2: Letting Recent Performance Dictate Tolerance

The error: After bull market: “I’m aggressive!” After crash: “I’m conservative!”

What happens:

- Buy high (when feeling confident after gains)

- Sell low (when panicking after losses)

- Exactly backwards from what works

The fix: Determine risk tolerance during calm markets, then stick to it regardless of recent performance.

Mistake 3: Ignoring Risk Capacity

The error: “I’m young and aggressive!” (while needing money in 2 years for house down payment)

What happens:

- Market drops 30% right before needing the money

- Forced to sell at loss or delay major life goal

- High tolerance doesn’t matter when capacity is low

The fix: Time horizon matters more than age. Money needed within 5 years shouldn’t be in aggressive investments regardless of your tolerance.

Mistake 4: Being Too Conservative for Too Long

The error: 25-year-old keeping 70% in bonds “to be safe”

What happens:

- Sacrifices decades of compound growth

- Portfolio grows at 4% instead of 9%

- Retires with half the wealth they could have had

Example:

- Conservative: $500/month for 40 years at 5% = $763,000

- Aggressive: $500/month for 40 years at 9% = $2,171,000

- Cost of excessive conservatism: $1,408,000!

The fix: If you have decades until retirement and stable income, being too conservative is riskier than being appropriately aggressive.

Mistake 5: Never Reassessing Tolerance

The error: Set allocation at age 30, never adjust, still 90% stocks at age 60.

What happens:

- Risk capacity decreased (less time to recover)

- But allocation stayed the same

- Major crash near retirement devastates portfolio

The fix: Reassess every 5 years or after major life changes (marriage, kids, career change, approaching retirement).

Mistake 6: Confusing Risk Tolerance with Return Expectations

The error: “I need 12% returns, so I’ll invest aggressively even though I hate volatility.”

What happens:

- Chases high returns despite low tolerance

- Panics during inevitable downturn

- Sells and locks in losses

- Never achieves needed returns anyway

The fix: Your tolerance dictates your allocation. Your allocation dictates realistic return expectations. Work backwards from your tolerance, not forwards from your dreams.

How to Build a Portfolio That Matches Your Risk Tolerance

Step-by-step process:

Step 1: Accurately Assess Your Tolerance

Use the methods from earlier in this article:

- Hypothetical loss test

- Sleep test

- Historical scenario test

- Comprehensive questionnaire

Be honest, not aspirational.

Step 2: Determine Your Risk Capacity

Consider:

- Time horizon (when do you need this money?)

- Income stability

- Emergency fund status

- Overall financial health

- Ability to contribute more if markets drop

Step 3: Choose the More Conservative

Compare tolerance vs capacity. Choose whichever suggests more conservative allocation.

Step 4: Select Your Allocation

Conservative: 30-40% stocks / 60-70% bonds

Moderate-Conservative: 50-60% stocks / 40-50% bonds

Moderate: 60-70% stocks / 30-40% bonds

Moderate-Aggressive: 70-80% stocks / 20-30% bonds

Aggressive: 80-100% stocks / 0-20% bonds

Step 5: Choose Specific Investments

For stocks:

- Total market index funds

- S&P 500 funds

- International index funds

For bonds:

- Total bond market funds

- Treasury bonds

- Corporate bond funds

Keep it simple. Diversification through index funds is sufficient.

Step 6: Implement and Automate

- Open investment accounts

- Buy your chosen funds

- Set up automatic monthly investments

- Turn on dividend reinvestment

Step 7: Rebalance Annually

Once per year:

- Check if allocation has drifted (stocks grew more than bonds)

- Sell some winners, buy some losers

- Return to target allocation

This forces you to “buy low, sell high” systematically.

Step 8: Adjust as Life Changes

Reassess and adjust when:

- You age significantly (every 5-10 years)

- Major life changes (marriage, kids, job loss)

- Approaching retirement (5-10 years before)

- After experiencing actual volatility (learned your true tolerance)

Frequently Asked Questions – FAQ

What is risk tolerance in investing?

Risk tolerance in investing is your psychological and financial ability to withstand investment losses and market volatility without making emotional decisions like panic-selling. It includes both your emotional comfort with seeing portfolio values drop and your financial capacity to absorb losses based on time horizon, income stability, and overall financial situation.

How do I know my risk tolerance?

Assess your risk tolerance by honestly answering: How much could my portfolio drop before I panic and sell? Consider hypothetical scenarios like a 30% market crash—would you sell, hold uncomfortably, or buy more? Also evaluate your financial capacity: when do you need this money, how stable is your income, and could you recover from major losses? Your true tolerance is usually revealed during actual market downturns.

What is a good risk tolerance for investing?

There’s no universally “good” risk tolerance—the right tolerance depends on your specific situation. Young investors (20s-30s) with decades until retirement can typically handle aggressive portfolios (80-100% stocks). Middle-aged investors (40s-50s) often need moderate allocations (60-70% stocks). Near-retirees should be more conservative (40-50% stocks). The “good” tolerance is one that lets you sleep at night while still achieving your financial goals.

Should I invest aggressively or conservatively?

Your investment approach should match both your emotional risk tolerance and your financial risk capacity, choosing whichever is more conservative. If you have decades until retirement, stable income, and can emotionally handle 30-40% portfolio drops without selling, invest aggressively (80%+ stocks). If you’re near retirement, have unstable income, or panic during market drops, invest conservatively (40-60% stocks). Most investors fall somewhere in the moderate range (60-70% stocks).

Does risk tolerance change with age?

Yes, risk tolerance typically decreases with age for two reasons: lower risk capacity (less time to recover from losses) and often lower emotional tolerance (more wealth at stake). A 25-year-old might invest 90-100% in stocks, while a 60-year-old near retirement might invest only 40-50% in stocks. However, individual circumstances matter more than age alone—a 50-year-old with 20 years until retirement has different needs than one retiring next year.

What happens if I invest too aggressively for my risk tolerance?

Investing too aggressively for your tolerance typically leads to panic-selling during market downturns, locking in losses at the worst possible time. For example, if you can’t actually handle a 30% drop but invest 100% in stocks, you’ll likely sell when markets crash, miss the recovery, and destroy your long-term returns. It’s better to accept slightly lower returns with an allocation you can stick with than to chase higher returns with a strategy you’ll abandon during volatility.

BONUS

Want to see risk tolerance explained visually?

This video helps you understand your investor profile and choose the right strategy:

FINAL THOUGHTS: Know Yourself, Build Wealth

Here’s the uncomfortable truth that most investing advice ignores: the perfect investment strategy on paper is worthless if you can’t stick with it.

You can read every book, follow every expert, and design the mathematically optimal portfolio. But if that portfolio causes so much anxiety that you sell during the first major downturn, it was the wrong portfolio for you.

The best investment strategy isn’t the one with the highest theoretical returns. It’s the one you can actually follow for decades.

That’s what risk tolerance is really about. It’s not about being brave or conservative. It’s not about what you should be comfortable with or what others are doing. It’s about honest self-assessment: Who are you? How do you actually react to losses? What lets you sleep at night?

The Simple Truth

Understanding your risk tolerance isn’t optional. It’s the foundation everything else is built on:

- Your risk tolerance determines your asset allocation

- Your asset allocation determines your expected returns

- Your expected returns determine whether you’ll reach your goals

- But none of it matters if you panic-sell during the first crash

The investor who can stick with a 60/40 portfolio through every crash will build more wealth than the investor who tries 100% stocks but sells in panic at 80/20.

Consistency beats optimization. Discipline beats perfection. Knowing yourself beats following others.

Your Action Steps This Week

Today:

- Take the risk tolerance assessments in this article honestly

- Identify your true tolerance (not what you wish it was)

- Compare your tolerance to your current portfolio

- Acknowledge if there’s a mismatch

This week:

- Calculate your appropriate stock/bond allocation

- Review your current investments

- Identify what needs to change

- Make a plan to adjust gradually (don’t sell everything at once)

This month:

- Implement your risk-appropriate allocation

- Set up automatic rebalancing

- Document your strategy and why you chose it

- Commit to sticking with it through volatility

Twenty years from now, you won’t remember the exact year markets dropped 30%. You won’t remember which allocation earned 0.5% more annually.

But you’ll remember whether you stayed invested or panicked. Whether you built wealth steadily or sabotaged yourself repeatedly. Whether you knew yourself well enough to choose the right strategy from the beginning.

That’s what understanding risk tolerance gives you: the self-knowledge to build a strategy you can actually follow for decades.

And following an imperfect strategy for decades beats abandoning a perfect strategy after one bad year.

Know yourself. Match your strategy to who you actually are. Stay the course.

That’s how you build lasting wealth.

INTERESTING TOPICS

Ready to build your portfolio?

Learn about index funds, the simple investment that matches any risk tolerance.

Want to invest consistently?

Master dollar-cost averaging, the strategy that works regardless of your tolerance.

Need to establish your foundation first?

Build your emergency fund before investing based on risk tolerance.

Disclaimer: This article is for educational purposes only. Diversification does not guarantee profits or protect against all losses. Consider your financial situation, risk tolerance, and investment timeline before making investment decisions.

—— End of Article ——