What Are ETFs and How Do They Work? (2026)

(Complete Guide)

Last updated: January 2026

Walk into any investment conversation today and you’ll hear the term “ETF” thrown around constantly. Financial advisors recommend them. Investment platforms feature them prominently.

Experienced investors swear by them. But what exactly are ETFs, and why has this investment vehicle revolutionized how ordinary people invest?

ETFs—Exchange-Traded Funds—have transformed investing by combining the diversification benefits of mutual funds with the flexibility and low costs of individual stocks. They’ve democratized access to sophisticated investment strategies that were once available only to wealthy investors, making it possible for anyone to build a diversified portfolio with just a few hundred dollars.

Yet despite their popularity, most beginners find ETFs confusing. How are they different from mutual funds or index funds? How do they actually work? Which ones should you buy? Are they really better than traditional investments?

In this guide, you’ll learn exactly what ETFs are, how they function behind the scenes, how they compare to other investment options, the different types available, how to choose the right ones, and the common mistakes that trip up even experienced investors. By the end, you’ll understand why ETFs have become the investment vehicle of choice for millions of investors.

Let’s break down ETFs in simple terms.

What Are ETFs? (Clear Definition)

An ETF (Exchange-Traded Fund) is an investment fund that holds a collection of assets (stocks, bonds, commodities, etc.) and trades on stock exchanges just like individual stocks, combining the diversification of mutual funds with the trading flexibility of stocks.

In simple terms: An ETF is a basket of investments that you can buy and sell throughout the trading day at market prices, just like buying a share of Apple or Tesla.

Breaking Down the Name:

Exchange-Traded:

- Trades on stock exchanges (NYSE, NASDAQ)

- Buy and sell any time the market is open

- Prices change throughout the day based on supply and demand

Fund:

- Pools money from many investors

- Uses that money to buy a collection of securities

- You own a share of the entire collection

A Simple Analogy:

Imagine you want to own a piece of every company in the technology sector, but buying individual shares of Apple, Microsoft, Google, Amazon, and hundreds of others would cost thousands and require constant management.

Instead, you buy one share of a Technology ETF for $100. That single share gives you tiny ownership in all those companies. When tech stocks go up, your ETF goes up. When they go down, your ETF goes down. You’re investing in the entire sector with one purchase.

Key Characteristics:

Trades like a stock:

- Buy/sell anytime during market hours

- Price fluctuates minute-by-minute

- Can use limit orders, stop losses, etc.

Structured like a fund:

- Holds many different securities

- Provides instant diversification

- Managed according to specific strategy or index

Typically low cost:

- Lower expense ratios than mutual funds

- No sales loads in most cases

- Competitive pricing due to structure

How ETFs Actually Work Behind the Scenes

Understanding how ETFs function helps you appreciate their unique advantages:

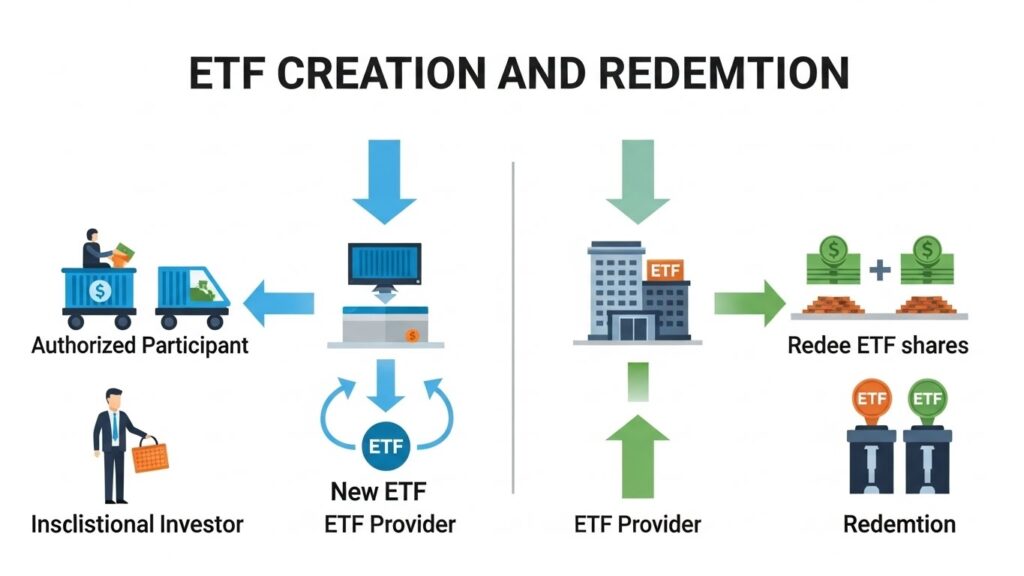

The Creation and Redemption Process

This is what makes ETFs special:

Creation (when demand increases):

- Large institutional investors (called “Authorized Participants”) gather the actual stocks that the ETF holds

- They deliver those stocks to the ETF provider

- ETF provider creates new ETF shares and gives them to the institution

- Institution sells those ETF shares on the stock exchange to investors like you

Redemption (when demand decreases):

- Authorized Participants buy ETF shares from the market

- They return those shares to the ETF provider

- ETF provider gives them the actual underlying stocks

- This removes ETF shares from circulation

Why this matters:

- Keeps ETF price aligned with the value of underlying assets

- Creates tax efficiency (more on this later)

- Allows ETFs to maintain low costs

How You Trade ETFs:

Step 1: You place an order through your brokerage

- Just like buying stock: “Buy 10 shares of [ETF ticker]”

- Market order (buy at current price) or limit order (buy at specific price)

Step 2: Your order goes to the stock exchange

- Matches with someone selling ETF shares

- Transaction happens instantly during market hours

Step 3: You own ETF shares

- Stored in your brokerage account

- Can sell anytime the market is open

The Underlying Holdings:

The ETF owns the actual investments:

- Stock ETF owns actual company shares

- Bond ETF owns actual bonds

- Commodity ETF owns futures contracts or physical commodities

- Real estate ETF owns REITs

You indirectly own them:

- Your ETF share represents proportional ownership

- If ETF holds 100 stocks, you own tiny pieces of all 100

ETFs vs Mutual Funds vs Index Funds: Key Differences

This is where confusion often starts. Let’s clarify:

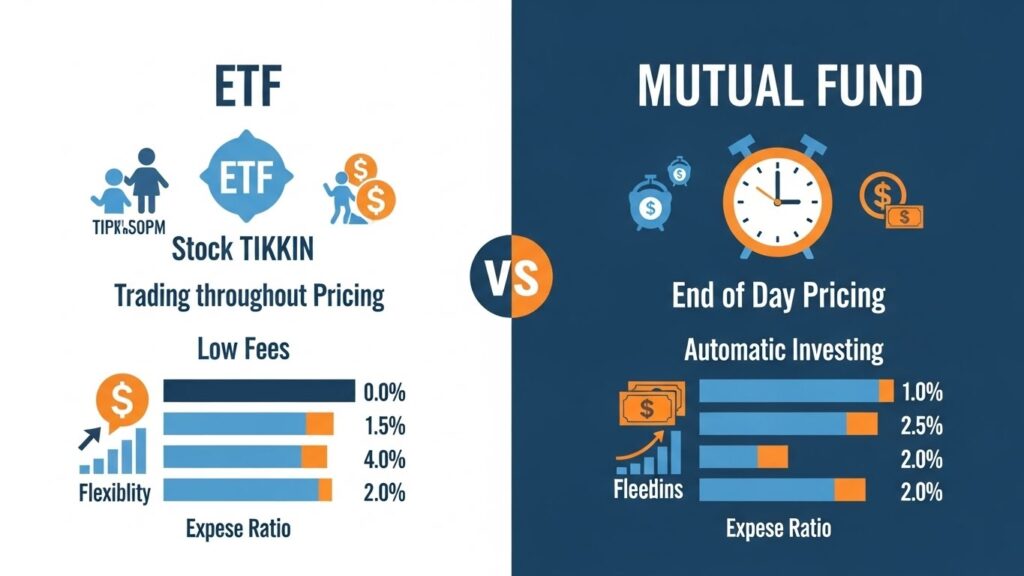

ETFs vs Mutual Funds

| Feature | ETFs | Mutual Funds |

|---|---|---|

| Trading | All day (like stocks) | Once daily at market close |

| Pricing | Real-time, fluctuates | End-of-day NAV (Net Asset Value) |

| Minimum Investment | Price of 1 share ($50-500 typically) | Often $1,000-$3,000 minimum |

| Expense Ratios | Usually lower (0.03-0.50%) | Usually higher (0.50-2.00%) |

| Tax Efficiency | Generally more tax-efficient | Less tax-efficient |

| Sales Loads | Rarely any | Often have front/back loads |

| Trading Costs | Brokerage commission (often $0 now) | No commission but higher expenses |

| Automatic Investment | Harder (fractional shares needed) | Easy to set up |

Bottom line: ETFs = more flexible, cheaper, better for most investors

Mutual Funds = easier for automatic investing, sometimes still used in 401(k)s

ETFs vs Index Funds

Here’s the confusion: An index fund can be EITHER an ETF OR a mutual fund!

“Index Fund” describes WHAT it does:

- Tracks a specific index (S&P 500, Total Market, etc.)

- Passive management

- Low cost, broad diversification

“ETF” or “Mutual Fund” describes HOW it trades:

- ETF = trades on exchange

- Mutual Fund = trades once daily

Examples:

- Vanguard S&P 500 ETF (VOO): Index fund + ETF structure

- Vanguard S&P 500 Mutual Fund (VFIAX): Index fund + Mutual fund structure

- Both track the same index!

- Both are index funds!

- Just different trading structures!

Most index funds today are available as ETFs, which is why people often use the terms interchangeably.

Quick Reference:

Index Fund = WHAT (tracks an index)

ETF/Mutual Fund = HOW (how it trades)

You can have:

- Index ETF (most common today)

- Index Mutual Fund (traditional)

- Actively managed ETF (rare but exists)

- Actively managed Mutual Fund (traditional active funds)

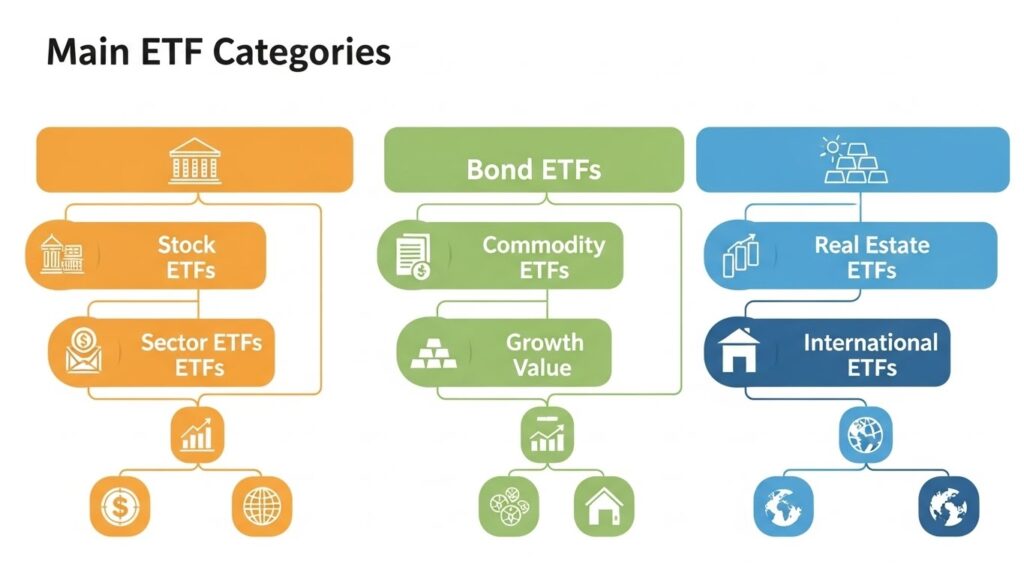

The Main Types of ETFs You Should Know

ETFs come in many flavors. Here are the major categories:

1. Stock ETFs (Equity ETFs)

What they hold: Company stocks

Types:

Broad Market ETFs:

- Total U.S. stock market

- S&P 500

- Total international stocks

- Examples: VTI, SPY, VXUS

Sector ETFs:

- Technology (XLK)

- Healthcare (XLV)

- Financial (XLF)

- Energy (XLE)

- Consumer goods, utilities, etc.

Size-Based ETFs:

- Large-cap (big companies)

- Mid-cap (medium companies)

- Small-cap (small companies)

- Examples: IVV (large), IJH (mid), IJR (small)

Style ETFs:

- Growth stocks (high growth potential)

- Value stocks (undervalued companies)

- Dividend stocks (high dividend payers)

Geographic ETFs:

- U.S. stocks

- International developed (Europe, Japan)

- Emerging markets (China, India, Brazil)

2. Bond ETFs (Fixed-Income ETFs)

What they hold: Government and corporate bonds

Types:

- Total bond market (AGG, BND)

- Treasury bonds (short, intermediate, long-term)

- Corporate bonds (investment grade and high-yield)

- Municipal bonds (tax-free)

- International bonds

Purpose: Stability, income, portfolio diversification

3. Commodity ETFs

What they track: Physical commodities or commodity futures

Types:

- Gold (GLD, IAU)

- Silver (SLV)

- Oil (USO)

- Agricultural commodities

- Broad commodity baskets

Purpose: Inflation hedge, diversification

4. Real Estate ETFs (REIT ETFs)

What they hold: Real Estate Investment Trusts (REITs)

Examples: VNQ, IYR

Purpose: Real estate exposure without buying property, income from dividends

5. International ETFs

What they hold: Stocks or bonds from specific countries or regions

Types:

- Developed markets (Europe, Japan, Canada)

- Emerging markets (China, India, Brazil)

- Single-country (Japan, Germany, etc.)

Purpose: Global diversification, exposure to international growth

6. Thematic/Specialty ETFs

What they focus on: Specific trends or strategies

Examples:

- Clean energy (ICLN)

- Artificial Intelligence (BOTZ)

- Cannabis (MJ)

- ESG/Sustainable (ESGU)

- Dividend aristocrats (NOBL)

Caution: More speculative, higher fees, concentrated risk

7. Inverse and Leveraged ETFs

What they do:

- Inverse: Profit when market goes down

- Leveraged: Magnify daily returns (2x or 3x)

Examples: SQQQ (3x inverse NASDAQ), TQQQ (3x long NASDAQ)

WARNING: Extremely risky, designed for day traders, NOT for long-term investors. Avoid unless you’re very experienced.

Advantages of ETFs for Investors

Why have ETFs become so popular? Here are the main benefits:

1. Lower Costs

Expense ratios:

- ETFs: 0.03-0.50% typically

- Mutual funds: 0.50-2.00% typically

Example impact:

- $10,000 invested for 30 years at 8% return

- 0.05% fee (ETF): $98,651

- 1.00% fee (Mutual fund): $81,156

- Savings: $17,495!

No sales loads:

- Most ETFs have no front-end or back-end loads

- Many mutual funds charge 3-5% just to buy in

2. Trading Flexibility

Buy/sell anytime:

- Market open = you can trade

- React to news immediately

- Set limit orders, stop losses

- Trade options on some ETFs

Mutual funds:

- Only trade once daily at 4pm ET

- Can’t react intraday

3. Tax Efficiency

ETFs are more tax-efficient due to their structure:

Creation/redemption in-kind:

- When institutions redeem ETF shares, they receive actual stocks (not cash)

- This doesn’t trigger capital gains

- Mutual funds must sell stocks to meet redemptions = capital gains = taxes passed to all shareholders

Result: ETF holders pay fewer taxes on capital gains

The SEC provides detailed information about how ETF tax efficiency works and benefits long-term investors.

Example: In 2022, many mutual funds distributed large capital gains to shareholders even though the market was down. Most ETFs did not.

4. Transparency

Daily holdings disclosure:

- ETFs disclose what they own every day

- You always know exactly what you’re invested in

Mutual funds:

- Disclose quarterly

- Holdings can change significantly between disclosures

5. Instant Diversification

One purchase = many investments:

- Buy SPY = own 500 companies

- Buy VTI = own 3,000+ companies

- Buy AGG = own thousands of bonds

Builds a diversified portfolio with minimal capital

6. Accessibility

Low minimums:

- Many ETFs cost $50-300 per share

- With fractional shares (many brokers offer), start with $1

No investment minimums:

- Unlike mutual funds ($1,000-$3,000 often required)

7. Variety and Specialization

ETF for almost any strategy:

- Want only dividend stocks? There’s an ETF

- Want only clean energy? There’s an ETF

- Want only companies with female CEOs? There’s an ETF

Allows precise portfolio construction

Disadvantages and Risks of ETFs

ETFs aren’t perfect. Here are the downsides:

1. Trading Costs Can Add Up

Commissions:

- Many brokers now offer commission-free ETF trading

- But some still charge $5-10 per trade

- Frequent trading adds up

Bid-ask spread:

- Difference between buying and selling price

- Can be $0.01 for liquid ETFs or $0.50+ for niche ETFs

- Eats into returns with frequent trading

Impact: Not ideal for frequent small automatic investments

2. Temptation to Overtrade

Because you CAN trade anytime doesn’t mean you SHOULD:

- Easy to check prices constantly

- Easy to react emotionally to news

- Easy to buy and sell impulsively

Research shows: Frequent traders underperform buy-and-hold investors

Solution: Treat ETFs like mutual funds—buy and hold long-term

3. Choice Paralysis

Too many options:

- Over 3,000 ETFs available in U.S.

- Analysis paralysis—which one to choose?

- Marketing hype for trendy ETFs

Many niche ETFs are unnecessary:

- You don’t need 20 different ETFs

- 3-5 broad ETFs cover most needs

4. Some ETFs Are Complex and Risky

Leveraged and inverse ETFs:

- Not suitable for buy-and-hold

- Decay over time due to daily rebalancing

- Can lose money even if you’re “right” long-term

Exotic asset ETFs:

- Commodities, currencies, volatility

- Complex pricing mechanisms

- Often high fees

Solution: Stick to simple, broad-market ETFs as beginner

5. Potential Tracking Error

ETFs aim to match their index but sometimes don’t perfectly:

- Small differences due to fees, trading costs, timing

- Usually minimal (0.05-0.20% annually)

- But it means you don’t get EXACT index returns

6. Market Price vs NAV Discrepancy

NAV (Net Asset Value): True value of underlying holdings

Market Price: What ETF trades for on exchange

Usually very close, but occasionally:

- High demand = ETF trades above NAV (premium)

- Low demand = ETF trades below NAV (discount)

For liquid ETFs: Difference is tiny ($0.01-0.05)

For niche ETFs: Can be larger

How to Choose the Right ETFs for Your Portfolio

With thousands of options, how do you choose? Follow these criteria:

Criteria 1: Match Your Investment Goals

For core holdings (foundation of portfolio):

- Broad market ETFs

- Total market or S&P 500

- Examples: VTI, VOO, SPY, IVV

For diversification:

- International ETFs

- Bond ETFs

- Real estate ETFs

For specific exposure:

- Sector ETFs (if you want to tilt toward tech, healthcare, etc.)

- Thematic ETFs (but be cautious—often speculative)

Criteria 2: Low Expense Ratio

Target: Under 0.20%, ideally under 0.10%

Great options:

- VTI: 0.03%

- VOO: 0.03%

- SCHB: 0.03%

- BND: 0.03%

Avoid: ETFs charging over 0.50% unless there’s clear justification

Criteria 3: High Liquidity

Liquidity = how easily you can buy/sell

Check:

- Average daily volume: Aim for 100,000+ shares traded daily

- Assets under management (AUM): Prefer $100M+

Why it matters:

- High liquidity = narrow bid-ask spread = lower trading costs

- Low liquidity = wide spreads = expensive to trade

Criteria 4: Tracking Difference

How closely does ETF match its index?

Check:

- Historical performance vs benchmark

- Should be very close (within 0.05-0.20%)

Red flag: ETF consistently underperforms its index by significant margin

Criteria 5: Reputation of Provider

Stick with established providers:

- Vanguard: Low-cost pioneer, investor-owned

- BlackRock (iShares): Largest ETF provider globally

- State Street (SPDR): Creator of first ETF (SPY)

- Schwab: Competitive low-cost options

- Fidelity: Recent entry with zero-fee ETFs

Be cautious with:

- Tiny, new providers

- Exotic, trendy ETFs with short track records

Criteria 6: Tax Efficiency

For taxable accounts:

- ETFs are generally tax-efficient

- Avoid ETFs with high turnover (frequent trading inside the fund)

For retirement accounts:

- Tax efficiency doesn’t matter (already tax-advantaged)

How to Buy and Sell ETFs

Buying ETFs is simple:

Step 1: Open a Brokerage Account

Best brokers for ETF investing:

Vanguard:

- Vanguard ETFs trade commission-free

- Great for buy-and-hold

Fidelity:

- All ETFs commission-free

- Excellent research tools

Schwab:

- All ETFs commission-free

- Strong mobile app

Robinhood:

- Commission-free

- Fractional shares available

- User-friendly for beginners

What you need:

- Social Security Number

- Bank account

- Government ID

- Basic personal info

Step 2: Fund Your Account

- Link your bank account

- Transfer money (usually takes 1-3 days)

- Some allow instant deposits

Step 3: Research and Choose ETFs

Use brokerage research tools:

- Search by ticker (e.g., “VTI”)

- View holdings, performance, fees

- Read ETF description

Or start simple:

- Total market ETF: VTI or ITOT

- S&P 500 ETF: VOO or SPY

- Can’t go wrong with these for beginners

Step 4: Place Your Order

Market Order:

- Buy at current market price

- Executes immediately

- Good for liquid ETFs during market hours

Limit Order:

- Buy only at specified price or better

- May not execute if price doesn’t reach your limit

- Good for less liquid ETFs or volatile times

How many shares?

- Decide how much to invest ($500? $1,000?)

- Divide by current share price

- Example: $1,000 ÷ $200/share = 5 shares

Or use fractional shares (if broker offers):

- Invest exact dollar amount ($500)

- Broker calculates fractional shares (2.5 shares)

Step 5: Confirm and Monitor

- Review order details

- Submit order

- Receive confirmation

- Shares appear in your account

Then: Hold long-term! Don’t check daily!

Selling ETFs:

Same process as buying, just click “Sell” instead:

- Enter number of shares to sell

- Choose market or limit order

- Submit

- Money settles in 2 business days (T+2)

Common ETF Mistakes to Avoid

Mistake 1: Chasing Performance

The error: Buying last year’s top-performing ETF

Why it fails:

- Past performance doesn’t predict future results

- Hot sectors/themes cool off

- You end up buying high

Example:

- 2020: ARK Innovation ETF (ARKK) gained 150%

- Everyone piled in during 2021

- 2021-2022: ARKK dropped 75%+

- Late investors crushed

The fix: Invest in broad, diversified ETFs regardless of recent performance

Mistake 2: Over-Diversification

The error: Buying 15-20 different ETFs thinking more = better

Why it’s wrong:

- Creates complexity

- Many ETFs overlap significantly

- Dilutes returns

- Hard to track

Example:

- S&P 500 ETF + Total Market ETF + Large-Cap ETF = 90% overlap!

The fix: 3-5 well-chosen ETFs cover most needs

Simple portfolio:

- 60% U.S. total market ETF

- 30% International total market ETF

- 10% Bond ETF

- Done!

Mistake 3: Trading Too Frequently

The error: Buying and selling ETFs based on news, feelings, market movements

Why it costs you:

- Trading costs add up

- Usually buy high, sell low

- Miss recovery periods

- Generate unnecessary taxes

The fix: Buy and hold long-term, ignore short-term noise

Mistake 4: Using Leveraged/Inverse ETFs Long-Term

The error: “I’ll buy 3x leveraged NASDAQ ETF and hold it!”

Why it’s dangerous:

- These ETFs reset daily

- Decay over time due to volatility

- Not designed for buy-and-hold

- Can lose money even if you’re right

Example:

- Index goes: +10%, -9%, +10%, -9% (ends roughly flat)

- Leveraged ETF: +30%, -27%, +30%, -27% = significant loss due to compounding

The fix: Avoid entirely unless you’re experienced day trader

Mistake 5: Ignoring Expense Ratios

The error: “0.50% expense ratio vs 0.05%—what’s 0.45%?”

Why it matters:

- Compounds over decades

- $10,000 for 30 years at 8% return:

- 0.05% fee: $98,651

- 0.50% fee: $92,152

- Cost: $6,499!

The fix: Always choose lowest-cost option for similar ETFs

Mistake 6: Buying Niche/Trendy ETFs

The error: “Clean energy is the future! I’ll go 100% into clean energy ETF!”

Why it’s risky:

- Concentrated exposure

- Subject to hype cycles

- Higher volatility

- Often higher fees

The fix: Niche ETFs as small position (5-10%) if desired, not core holdings

Frequently Asked Questions – FAQ

What are ETFs in simple terms?

ETFs (Exchange-Traded Funds) are investment funds that hold collections of stocks, bonds, or other assets and trade on stock exchanges just like individual stocks. You can buy and sell them throughout the trading day at market prices. One ETF share gives you instant exposure to dozens, hundreds, or thousands of underlying investments, providing easy diversification at low cost.

Are ETFs better than mutual funds?

For most investors, yes. ETFs typically have lower expense ratios (0.03-0.20% vs 0.50-2.00%), better tax efficiency, no sales loads, and more trading flexibility than mutual funds. The main advantage of mutual funds is easier automatic investing. However, many brokers now offer fractional ETF shares and automatic investment plans, eliminating even this advantage.

How do ETFs make money?

ETFs generate returns two ways: (1) Price appreciation—when the underlying stocks or bonds increase in value, your ETF shares increase in value, and (2) Income distribution—many ETFs pay dividends from the stocks they hold or interest from bonds they hold. Most investors reinvest these distributions automatically to benefit from compound growth over time.

What is the difference between ETFs and index funds?

An index fund is a type of fund that tracks a specific market index (like S&P 500). An index fund can be structured as either an ETF or a mutual fund. Most index funds today are available as ETFs. So “index fund” describes what it does (tracks an index passively), while “ETF” describes how it trades (on an exchange like a stock).

Can you lose money in ETFs?

Yes, ETFs can lose value. If the underlying stocks or bonds decrease in price, your ETF will decrease in value proportionally. For example, if the stock market drops 20%, a total market ETF will drop approximately 20%. However, broad market ETFs historically recover from downturns over long periods. The key is having appropriate risk tolerance and a long-term investment horizon.

What are the best ETFs for beginners?

For beginners, start with broad, low-cost market ETFs: (1) Total U.S. stock market (VTI, ITOT, SCHB), (2) S&P 500 (VOO, SPY, IVV), or (3) Total international stock market (VXUS, IXUS). These provide instant diversification across hundreds or thousands of companies at rock-bottom costs (0.03-0.05% expense ratios). As you gain experience and build your portfolio, you can add bond ETFs for stability and international ETFs for global diversification.

BONUS

Want to see ETFs explained visually?

This video breaks down exactly what ETFs are and how they work in simple terms:

FINAL THOUGHTS: The Investment Vehicle That Changed Everything

In 1993, the first ETF launched. Just 30 years later, ETFs hold over $7 trillion in assets and have fundamentally changed how people invest.

Why? Because ETFs solved real problems:

Before ETFs:

- Want diversification? Pay 1-2% annually for an active mutual fund

- Want to trade during the day? Buy individual stocks (expensive, risky, time-consuming)

- Want tax efficiency? Too bad—mutual funds distributed capital gains whether you wanted them or not

- Want low costs? Limited options and high minimums

After ETFs:

- Diversification: One purchase, instant exposure to thousands of securities

- Flexibility: Trade anytime, just like stocks

- Costs: Rock-bottom fees (0.03%) with no minimum investment

- Tax efficiency: Structure minimizes capital gains distributions

ETFs democratized investing. They gave ordinary people access to institutional-quality investment tools at retail prices.

The Simple Truth

You don’t need to understand every technical detail of how ETFs work. You need to understand this:

ETFs allow you to build a properly diversified, low-cost, tax-efficient portfolio with a few hundred dollars and three simple purchases.

That’s revolutionary. Before ETFs, building such a portfolio required:

- Thousands of dollars

- Buying 20-30 individual stocks

- Constantly rebalancing

- Significant time and knowledge

Now? Buy VTI (total U.S. market), VXUS (total international), and BND (total bonds). That’s it. You own over 10,000 securities, globally diversified, for less than 0.05% annual cost.

That’s the power of ETFs.

Your Action Steps This Week

Today:

- Decide if ETFs fit your investment strategy (they probably do)

- Identify which type of account you need (taxable or retirement)

- Choose a broker that offers commission-free ETF trading

This week:

- Open your account if you don’t have one

- Choose 1-3 core ETFs (keep it simple!)

- Total market or S&P 500 for U.S. stocks

- International ETF for global exposure

- Bond ETF for stability (if desired)

This month:

- Make your first ETF purchase

- Set up automatic monthly investments

- Turn on automatic dividend reinvestment

- Commit to long-term holding

Twenty years from now, you won’t remember which specific ETFs you bought or what the market did on the day you invested.

But you’ll see the results: a portfolio that grew steadily through decades, required minimal effort, cost almost nothing in fees, and funded your financial goals.

That’s what ETFs make possible. Start today.

INTERESTING TOPICS

Ready to start investing?

Learn how to begin with just $100 using ETFs and build wealth.

Want to understand the best ETF strategy?

Read about index funds, which most ETFs are based on.

Need to know how much to invest in ETFs?

Discover dollar-cost averaging, the strategy that removes emotion from ETF investing.

Disclaimer: This article is for educational purposes only. Diversification does not guarantee profits or protect against all losses. Consider your financial situation, risk tolerance, and investment timeline before making investment decisions.

—— End of Article ——