What Are Index Funds? A Complete Beginner’s Guide

Last updated: December 2025

If you’ve been researching investing, you’ve probably heard the term “index fund” mentioned repeatedly. Financial experts love them. Warren Buffett recommends them. They’re called the “best investment for most people.” But what exactly are index funds, and why does everyone seem to love them so much?

The answer is simpler than you might think. Index funds are investment vehicles that allow you to own a piece of hundreds or thousands of companies with a single purchase, automatically diversified, professionally managed, and available for a fraction of the cost of traditional investing.

For beginners, index funds solve the three biggest investing challenges: they eliminate the need to pick individual stocks, they provide instant diversification, and they cost very little. This combination has made index funds the foundation of millions of successful investment portfolios.

In this guide, you’ll learn exactly what index funds are, how they work, why they’re perfect for beginners, how to choose the right ones, and how to start investing in them today. By the end, you’ll understand why index funds have revolutionized investing for everyday people.

Let’s break it down in simple terms.

What Are Index Funds? (Simple Definition)

An index fund is a type of investment fund that aims to match the performance of a specific market index by holding all (or a representative sample) of the securities in that index.

In simple terms: An index fund is a basket that contains small pieces of many different companies, designed to mirror the performance of a specific market segment.

Breaking It Down:

Index: A list or grouping of stocks that represents a portion of the market.

- Example: The S&P 500 is an index of the 500 largest U.S. companies

Fund: A pooled investment vehicle where many investors’ money is combined to buy securities.

- Your money is pooled with other investors to buy all the stocks in the index

Index Fund: A fund that tracks an index passively.

- It simply buys and holds everything in the index

- No active stock picking or market timing

A Real-World Analogy:

Imagine you want to own a piece of every major restaurant in America, but buying individual shares in each one would cost thousands of dollars and require constant management.

Instead, you buy shares in a “Restaurant Index Fund” that owns a small piece of all major restaurants. When the restaurant industry does well, your investment grows. When it struggles, your investment dips. You’re not betting on one restaurant—you’re betting on the entire industry.

That’s how index funds work, but instead of just restaurants, you’re buying pieces of entire markets or sectors.

How Index Funds Actually Work

Let’s understand the mechanics with a clear example.

Example: S&P 500 Index Fund

The S&P 500 Index:

- A list of 500 of the largest U.S. companies

- Includes Apple, Microsoft, Amazon, Google, Tesla, and 495 others

- Represents about 80% of the total U.S. stock market value

An S&P 500 Index Fund:

- Owns shares in all 500 companies in the same proportions as the index

- If Apple is 7% of the S&P 500, the fund allocates 7% of its assets to Apple

- If Tesla is 2% of the S&P 500, the fund allocates 2% to Tesla

- And so on for all 500 companies

When you invest $1,000 in an S&P 500 index fund:

- You’re automatically buying tiny pieces of all 500 companies

- Your $1,000 is split proportionally across all of them

- You instantly own a diversified portfolio

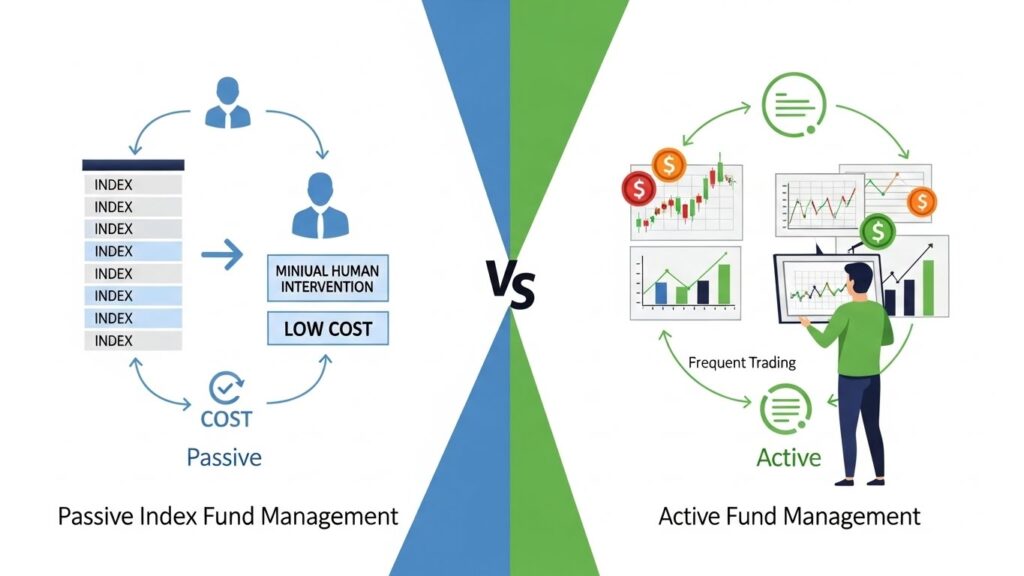

The Passive Management Approach:

Index funds are passively managed, meaning:

No stock picking: The fund doesn’t try to choose winners or avoid losers—it owns everything in the index

No market timing: The fund doesn’t try to buy low and sell high—it stays fully invested

Automatic adjustments: When companies enter or leave the index, the fund automatically adjusts

Low turnover: Very little buying and selling happens, which keeps costs and taxes low

How Index Funds Make (or Lose) Money:

Scenario 1: Market Goes Up

- The companies in the index increase in value

- Your index fund shares increase proportionally

- You profit

Scenario 2: Market Goes Down

- The companies in the index decrease in value

- Your index fund shares decrease proportionally

- You experience a temporary loss (on paper)

Scenario 3: Dividends

- Many companies pay dividends (cash to shareholders)

- Index funds collect these dividends

- Dividends are either paid to you or automatically reinvested

Long-term result: Historically, broad market index funds like the S&P 500 have returned about 10% annually over long periods, despite short-term volatility.

Index Funds vs Individual Stocks vs Mutual Funds

Understanding how index funds compare to other investment options clarifies why they’re so popular.

Index Funds vs Individual Stocks

| Aspect | Index Funds | Individual Stocks |

|---|---|---|

| Diversification | Instant (hundreds/thousands of stocks) | None (one company at a time) |

| Risk | Lower (spread across many companies) | Higher (concentrated in one company) |

| Research Required | Minimal | Extensive |

| Time Commitment | Very low | High (constant monitoring) |

| Cost | Very low (0.03-0.20% annually) | Low per trade, but adds up |

| Volatility | Moderate | High |

| Potential Returns | Market average (~10% historically) | Could be higher or much lower |

| Suitable For | Beginners and busy people | Experienced investors with time |

Example:

- Buy one Apple stock: You own one company. If Apple struggles, you lose money.

- Buy S&P 500 index fund: You own 500 companies. If Apple struggles but others thrive, you’re protected.

Index Funds vs Actively Managed Mutual Funds

| Aspect | Index Funds | Active Mutual Funds |

|---|---|---|

| Management | Passive (follows index) | Active (manager picks stocks) |

| Cost | Very low (0.03-0.20%) | High (0.50-2.00%+) |

| Goal | Match market performance | Beat market performance |

| Success Rate | Always matches index | 80-90% underperform index long-term |

| Turnover | Very low | High (lots of buying/selling) |

| Tax Efficiency | High | Lower |

| Transparency | High (you know what’s in it) | Lower (holdings can change frequently) |

The Evidence: Studies show that over 15-20 year periods, about 90% of actively managed funds fail to beat their benchmark index after accounting for fees, according to S&P Dow Jones Indices research. This is why Warren Buffett and other legendary investors recommend index funds for most people.

Bottom line: Index funds consistently beat most professional investors over time, simply by matching the market at minimal cost.

Why Index Funds Are Perfect for Beginners

Index funds solve nearly every challenge beginners face when starting to invest:

1. No Need to Pick Stocks

The problem: Beginners don’t know which companies to invest in. Should you buy Apple or Microsoft? Tesla or Ford? Amazon or Walmart?

Index fund solution: You don’t have to choose. An index fund owns all of them. You’re not betting on individual winners—you’re betting on the market as a whole.

2. Instant Diversification

The problem: Building a properly diversified portfolio of individual stocks requires buying 20-30+ different companies across various sectors, which costs thousands of dollars.

Index fund solution: One index fund purchase gives you instant exposure to hundreds or thousands of companies. Diversification happens automatically with your first $100.

3. Extremely Low Cost

The problem: High fees destroy returns over time. A 1% annual fee can cost you hundreds of thousands of dollars over decades.

Index fund solution: Most index funds charge 0.03-0.20% annually—a fraction of the cost of actively managed funds. Research on investment costs shows that lower fees significantly improve long-term returns, making cost one of the most important factors in fund selection. More money stays invested and compounds.

Example:

- $10,000 invested for 30 years at 10% return

- 0.05% fee (index fund): Final value = $174,491

- 1.00% fee (active fund): Final value = $149,035

- Difference: $25,456 saved with index fund!

4. Requires Minimal Time and Knowledge

The problem: Most people don’t have time to research stocks, monitor markets, or make constant investment decisions.

Index fund solution: Set it and forget it. Buy an index fund, contribute regularly through dollar-cost averaging, and let it grow for decades. No constant monitoring needed.

5. Historically Strong Returns

The problem: Beginners want good returns but don’t want excessive risk.

Index fund solution: The S&P 500 has delivered about 10% average annual returns over the past 50+ years, despite numerous recessions and market crashes. This includes:

- The 2008 financial crisis

- The 2000 dot-com bubble

- The 2020 COVID crash

- Multiple other downturns

Over long periods, index funds have consistently recovered and grown.

6. Simplicity and Clarity

The problem: Investing can feel overwhelming with complex strategies, confusing terminology, and conflicting advice.

Index fund solution: One simple decision: choose a broad market index fund (like total stock market or S&P 500), invest consistently, and hold long-term. That’s the entire strategy.

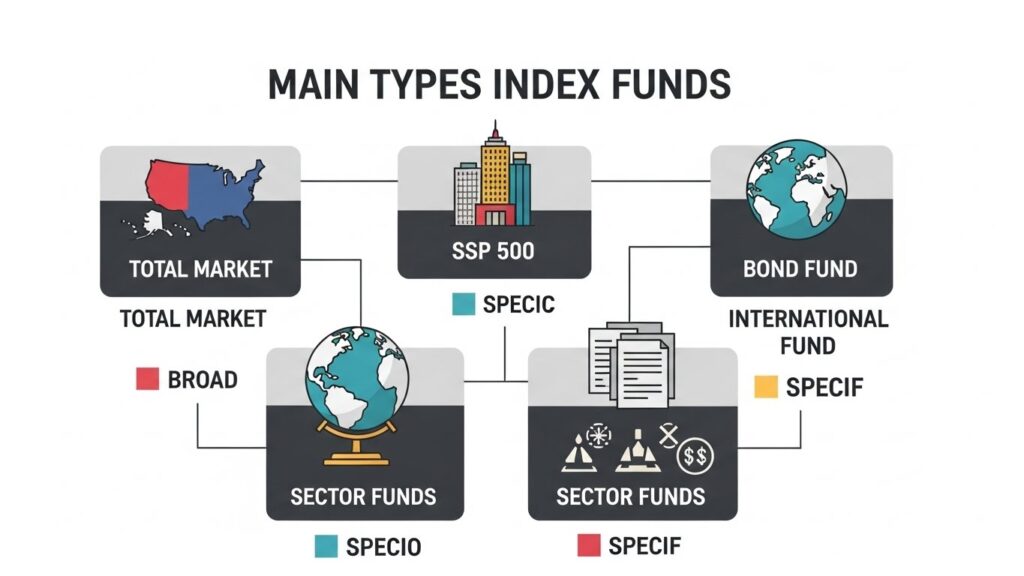

Types of Index Funds You Should Know

Not all index funds are the same. Here are the main types:

1. Broad U.S. Stock Market Index Funds

What they track: The entire U.S. stock market (3,000-4,000 companies of all sizes)

Examples:

- Vanguard Total Stock Market Index (VTSAX / VTI)

- Fidelity Total Market Index (FSKAX / ITOT)

- Schwab U.S. Broad Market (SCHB)

Best for: Core holding, maximum U.S. diversification

Typical return: ~10% annually over long periods

2. S&P 500 Index Funds

What they track: The 500 largest U.S. companies

Examples:

- Vanguard S&P 500 Index (VFIAX / VOO)

- Fidelity 500 Index (FXAIX / SPY)

- Schwab S&P 500 Index (SWPPX / IVV)

Best for: Core holding, large-cap U.S. exposure

Typical return: ~10% annually over long periods

Note: Very similar to total market funds but focused only on large companies

3. International Stock Index Funds

What they track: Companies outside the U.S. (developed and/or emerging markets)

Examples:

- Vanguard Total International Stock (VTIAX / VXUS)

- Fidelity International Index (FTIHX)

- Schwab International Equity (SCHF)

Best for: Global diversification, reducing U.S.-only risk

Typical allocation: 20-40% of stock portfolio

4. Bond Index Funds

What they track: Government and corporate bonds

Examples:

- Vanguard Total Bond Market (VBTLX / BND)

- Fidelity U.S. Bond Index (FXNAX)

- Schwab U.S. Aggregate Bond (SCHZ)

Best for: Stability, income, reducing portfolio volatility

Typical allocation: Based on age/risk tolerance (see asset allocation)

5. Sector-Specific Index Funds

What they track: Specific industries or sectors

Examples:

- Technology sector index

- Healthcare sector index

- Real estate sector index (REITs)

Best for: Advanced investors wanting to overweight certain sectors

Caution: Less diversified than broad market funds

6. Small-Cap and Mid-Cap Index Funds

What they track: Smaller companies with higher growth potential

Examples:

- Small-cap index funds (companies $300M-$2B)

- Mid-cap index funds (companies $2B-$10B)

Best for: Adding growth tilt to portfolio

Note: More volatile than large-cap funds

How to Choose the Right Index Funds

With so many options, how do you choose? Follow these criteria:

Criteria 1: Low Expense Ratio

What it is: The annual fee charged by the fund, expressed as a percentage.

Target: Under 0.20%, ideally under 0.10%

Why it matters: Lower fees mean more of your money stays invested and compounds.

Example expense ratios:

- Vanguard Total Stock Market (VTI): 0.03%

- Fidelity Total Market (FSKAX): 0.015%

- SPDR S&P 500 ETF (SPY): 0.0945%

All excellent choices!

Criteria 2: Broad Diversification

What it means: The fund holds many companies across various sectors.

Good: S&P 500 (500 companies), Total Stock Market (3,000+ companies)

Less ideal: Sector-specific funds (concentrated risk)

For beginners: Start with the broadest funds possible.

Criteria 3: High Trading Volume (for ETFs)

What it means: How many shares are bought and sold daily.

Why it matters: High volume means you can buy and sell easily without price impact.

Check: Average daily volume over 1 million shares

Note: Not a concern for mutual funds, only ETFs.

Criteria 4: Reputable Provider

Stick with established, low-cost providers:

- Vanguard: Pioneer of index funds, owned by investors (no profit motive)

- Fidelity: Competitive fees, excellent service

- Schwab: Low costs, great platform

- BlackRock (iShares): Largest ETF provider

Avoid: Obscure providers with high fees or new, unproven funds.

Criteria 5: Tax Efficiency (for taxable accounts)

What it means: How much in taxes the fund generates annually.

Better: Index funds (low turnover = fewer taxable events)

Worse: Actively managed funds (high turnover = more taxes)

Best: Hold index funds in tax-advantaged accounts (401k, IRA) when possible.

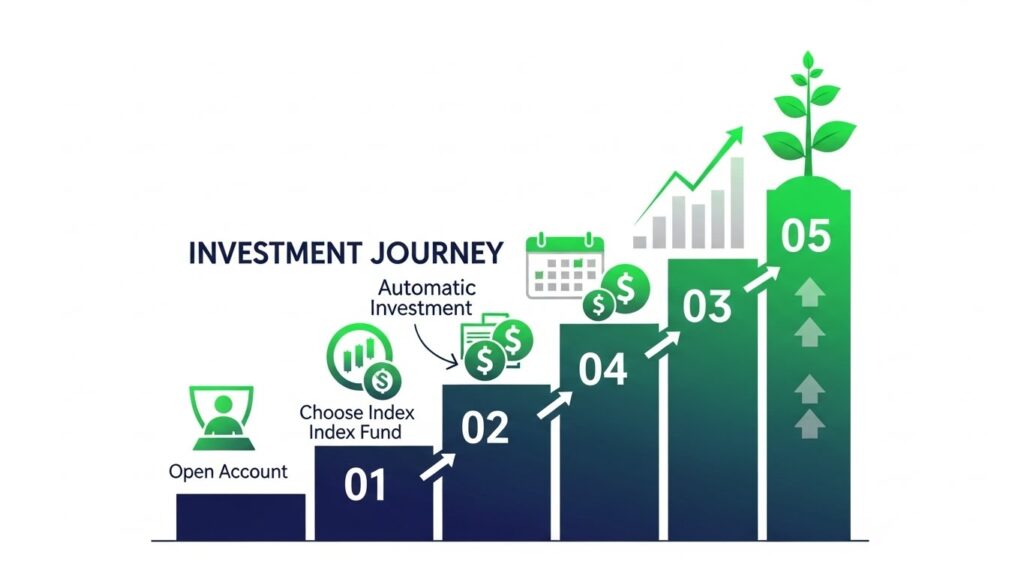

How to Start Investing in Index Funds

Ready to invest? Here’s your step-by-step action plan:

Step 1: Choose Your Account Type

For retirement savings:

- 401(k): Through your employer (get the match!)

- IRA or Roth IRA: Individual retirement account (tax advantages)

For non-retirement goals:

- Taxable brokerage account: Flexible, no contribution limits, no restrictions

Priority order:

- 401(k) up to employer match

- Max out Roth IRA ($7,000/year in 2024)

- Additional 401(k) contributions

- Taxable brokerage account

Step 2: Open an Account

Best brokerages for index fund investing:

Vanguard:

- Lowest-cost index funds

- Owned by investors

- Great for buy-and-hold

Fidelity:

- Zero expense ratio index funds

- Excellent customer service

- User-friendly platform

Schwab:

- Low costs

- Great research tools

- Strong mobile app

What you’ll need:

- Social Security Number

- Bank account for transfers

- Basic personal information

- Government-issued ID

Process takes: 10-15 minutes online

Step 3: Choose Your Index Fund(s)

For absolute beginners (simplest approach):

Option 1: One-Fund Portfolio

- 100% Total Stock Market Index Fund

- Example: VTI (Vanguard) or ITOT (iShares)

- Perfect for long time horizons (20+ years)

Option 2: Two-Fund Portfolio

- 70% Total U.S. Stock Market

- 30% Total International Stock Market

- Better global diversification

Option 3: Three-Fund Portfolio (most popular)

- 60% Total U.S. Stock Market

- 20% Total International Stock Market

- 20% Total Bond Market

- Balanced approach with some stability

Your choice depends on:

- Age (younger = more stocks)

- Risk tolerance (comfortable with volatility?)

- Timeline (when do you need the money?)

Step 4: Decide How Much to Invest

Options:

Lump sum:

- Invest available money all at once

- Historically slightly better performance

- Can feel riskier emotionally

- Invest fixed amount regularly (e.g., $200/month)

- Reduces timing risk

- Emotionally easier

- Perfect for investing from regular income

Recommendation for beginners:

- Start with whatever you have (even $100)

- Set up automatic monthly investments

- Increase as income grows

Step 5: Set Up Automatic Investments

Why automate:

- Removes emotion from investing

- Ensures consistency

- You never “forget” to invest

- Implements dollar-cost averaging automatically

How to set up:

- Log into your brokerage account

- Find “automatic investment” or “recurring investment” settings

- Choose your index fund

- Set amount ($100, $500, whatever you can afford)

- Set frequency (monthly on payday is common)

- Set start date

- Turn on automatic dividend reinvestment (DRIP)

Done! Your investment strategy is now on autopilot.

Step 6: Rebalance Annually

What is rebalancing: Adjusting your portfolio back to target allocations when they drift.

Example:

- Target: 70% stocks, 30% bonds

- After 1 year: 80% stocks (grew), 20% bonds

- Rebalance: Sell some stocks, buy bonds, return to 70/30

How often: Once per year is sufficient

Why: Maintains your desired risk level and forces you to “buy low, sell high”

Common Mistakes to Avoid

Even with simple index funds, mistakes happen:

Mistake 1: Choosing High-Fee Index Funds

The error: Buying an S&P 500 fund with a 0.50% expense ratio when 0.03% options exist.

Why it’s costly: That extra 0.47% annually costs tens of thousands over decades.

Example:

- $10,000 invested for 30 years at 10% return

- 0.03% fee: $172,000

- 0.50% fee: $161,000

- Cost of ignoring fees: $11,000!

The fix: Always compare expense ratios before buying.

Mistake 2: Over-Diversifying with Too Many Index Funds

The error: Owning 10 different index funds thinking more = better.

Why it’s wrong: Creates unnecessary complexity, potential overlap, and dilutes returns.

Example:

- S&P 500 fund + Total Market fund + Large Cap fund = 90% overlap!

The fix: 1-3 index funds is plenty for most investors.

Mistake 3: Panic Selling During Market Drops

The error: Market drops 20%, you panic and sell your index funds.

Why it’s costly: You lock in losses and miss the recovery. Every major market drop has been followed by a recovery.

Historical fact: If you invested in an S&P 500 index fund at the peak before the 2008 crash and held, you recovered all losses by 2013 and doubled your money by 2020.

The fix: Don’t look at your account during crashes. Keep investing through downturns (you’re buying shares on sale!).

Mistake 4: Trying to Time the Market

The error: “I’ll wait for the market to drop before investing,” or “I’ll sell now and buy back when it’s lower.”

Why it fails: Nobody can consistently predict short-term market movements, not even professionals.

The data: Missing just the 10 best days in the market over 20 years can cut your returns in half.

The fix: Invest now, invest consistently, stay invested. Time IN the market beats TIMING the market.

Mistake 5: Ignoring Tax-Advantaged Accounts

The error: Investing everything in taxable accounts while not maxing out 401(k) or IRA.

Why it’s costly: You pay unnecessary taxes on gains and miss out on tax-deferred or tax-free growth.

The fix:

- Max out employer 401(k) match (free money!)

- Max out Roth IRA ($7,000/year)

- Increase 401(k) contributions

- Then use taxable accounts

Mistake 6: Forgetting to Reinvest Dividends

The error: Taking dividends as cash instead of reinvesting them.

Why it’s costly: Dividends are a significant part of total returns. Not reinvesting means missing compound growth.

Example: From 1930-2020, about 40% of total stock market returns came from reinvested dividends.

The fix: Turn on automatic dividend reinvestment (DRIP) in your account settings.

Frequently Asked Questions – FAQ

What are index funds in simple terms?

Index funds are investment funds that hold all the stocks (or bonds) in a specific market index, like the S&P 500. Instead of trying to pick winning stocks, they simply own everything in the index in the same proportions. This gives you instant diversification and allows your investment to match the overall market performance at very low cost.

Are index funds good for beginners?

Yes, index funds are ideal for beginners because they require minimal investment knowledge, provide instant diversification across hundreds of companies, charge very low fees (typically 0.03-0.20% annually), and historically deliver solid returns (around 10% annually for U.S. stock index funds over long periods). You don’t need to pick stocks, time the market, or constantly monitor your investments.

How much money do I need to start investing in index funds?

You can start with as little as $1 with most modern brokerages through fractional shares. Many index fund ETFs trade around $50-400 per share, and most brokerages now allow you to buy partial shares. Some mutual fund index funds have minimums of $1,000-$3,000, but their ETF versions have no minimum. Starting with $100 is completely realistic.

What is the difference between index funds and ETFs?

Index funds come in two structures: mutual funds and ETFs (Exchange-Traded Funds). Both can track the same index, but ETFs trade like stocks throughout the day, while mutual funds trade once per day at closing price. ETFs often have lower minimums and sometimes slightly lower fees. For buy-and-hold investors, the difference is minimal—both are excellent choices.

Can you lose money in index funds?

Yes, index funds can lose value in the short term when the overall market declines. During the 2008 crisis, the S&P 500 dropped about 50%. However, it recovered fully and went on to new highs. Over long periods (10+ years), broad market index funds have consistently delivered positive returns despite temporary downturns. The key is having a long investment timeline and not selling during drops.

Which index fund should I buy first?

For most beginners, start with a total U.S. stock market index fund like Vanguard Total Stock Market (VTI), Fidelity Total Market (FSKAX), or Schwab U.S. Broad Market (SCHB). These provide instant diversification across the entire U.S. stock market. Alternatively, an S&P 500 index fund provides similar benefits with focus on large companies. Choose one from a reputable provider with an expense ratio under 0.20%.

BONUS

Want to see index funds explained visually?

This video breaks down exactly how index funds work

and why they’re the foundation of successful investing for beginners:

FINAL THOUGHTS: The Investment That Changed Everything

Index funds didn’t exist until 1976 when Vanguard founder John Bogle created the first one. Before that, regular people had two choices: try to pick individual stocks (risky and time-consuming) or pay high fees to active mutual fund managers (who usually underperformed the market anyway).

Index funds changed everything. They democratized investing, making it possible for anyone to build wealth through the stock market without special knowledge, without dedicating hours to research, and without paying excessive fees.

The results speak for themselves:

Over the past 50 years, a simple strategy of buying and holding an S&P 500 index fund has:

- Turned $10,000 into over $1 million

- Outperformed about 90% of professional money managers

- Required almost no time or effort from investors

- Cost a fraction of traditional investing approaches

That’s not hype. That’s historical fact.

The Simple Truth

You don’t need to be a financial genius to build wealth. You don’t need to spend hours analyzing stocks. You don’t need expensive advisors or complex strategies.

You need:

- A low-cost index fund (total market or S&P 500)

- Consistent contributions (through dollar-cost averaging)

- Time (decades for compound interest to work)

- Patience (to not panic during inevitable market drops)

- Discipline (to stay the course regardless of market noise)

That’s it. That’s the strategy that’s created more wealth for ordinary people than any other investment approach in history.

Your Action Steps This Week

Monday:

- Decide which type of account you need (401k, IRA, or taxable)

- Choose a brokerage (Vanguard, Fidelity, or Schwab)

Wednesday:

- Open your account (takes 10-15 minutes)

- Link your bank account

Friday:

- Choose your index fund (total market or S&P 500)

- Make your first investment (even if it’s just $50-100)

- Set up automatic monthly contributions

- Turn on dividend reinvestment

Done! You’re now an index fund investor. You’ve just implemented the same strategy Warren Buffett recommends, the approach that’s outperformed most professional investors, and the foundation for building long-term wealth.

The market will rise and fall. News will be good and bad. Experts will make predictions (that usually prove wrong).

But your index fund will quietly do what it’s done for 50 years: capture the growth of the overall market, compound your returns through reinvested dividends, and steadily build your wealth.

That’s the power of index funds. Start today.

Your future self will thank you.

INTERESTING TOPICS

Ready to start?

Learn how to begin investing with just $100 and start your index fund journey today.

Want to invest consistently?

Master dollar-cost averaging to remove emotion and timing from your index fund investing.

Need a complete strategy?

Discover how to build a diversified portfolio using index funds as your foundation.

Want more financial insights delivered to you? Subscribe to our newsletter

and get weekly articles with practical strategies to grow your wealth sent straight to your inbox.

Obs: Sign up for our newsletter and receive a free Finance For Beginner eBook.

Disclaimer: This article is for educational purposes only. Diversification does not guarantee profits or protect against all losses. Consider your financial situation, risk tolerance, and investment timeline before making investment decisions.

—— End of Article ——