Investment Opportunities in 2027: Where to Put Your Money Next Year

(Complete Guide)

Last updated: February 2026

2027 is coming.

You have money to invest. Maybe $1,000. Maybe $10,000. Maybe $100,000.

But where should you put it?

Stocks? Bonds? Real estate? Crypto? Gold? International markets? AI companies? Green energy? Treasury bills?

Too many choices. Analysis paralysis.

Most people make one of two mistakes:

Mistake 1: Do nothing (money sits in savings earning 0.5%, loses to inflation) Mistake 2: Chase hot trends (buy high, panic sell low, lose money)

Both result in the same thing: Wealth not built.

Here’s the truth: 2027 will have clear investment opportunities. Most people will miss them.

Why? Because they’re looking for “get rich quick” instead of “get rich for sure.”

The wealthy understand something critical: The best investment opportunities in 2027 aren’t sexy. They’re boring, proven, and consistently profitable.

You understand compound interest? You know how to build an emergency fund?

You’ve learned how to diversify? You can read stock charts? You know how to negotiate raises?

Don’t worry, we’ve gathered all these topics (among others) into carefully crafted and separated articles to make your learning easier.

Check out the “Categories” guide.

In this guide, you’ll learn the top investment opportunities in 2027 based on economic trends, which investments to prioritize for maximum returns, how to position your portfolio for 2027’s market conditions, specific assets and sectors with highest potential, common investment mistakes to avoid in 2027, and most importantly—how to invest your money wisely next year for long-term wealth.

By the end, you’ll know exactly where to put your money in 2027.

Let’s identify the best investment opportunities in 2027.

The 2027 Economic Landscape

Understanding 2027’s economic environment reveals the best investment opportunities in 2027.

Key Economic Factors for 2027

Interest Rates:

- Fed policy: Gradual cuts expected in 2027

- Current: ~4.5-5.0% (as of early 2026)

- Expected 2027: 3.5-4.5%

- Impact: Lower rates = stocks more attractive, bonds less attractive

Inflation:

- 2025-2026: Cooling but persistent (3-4%)

- 2027 forecast: 2-3% (closer to Fed target)

- Impact: Real returns improve, purchasing power stabilizes

GDP Growth:

- 2026: Moderate growth (1.5-2.5%)

- 2027 forecast: Steady growth (2-3%)

- Impact: Corporate earnings growth, stock market support

Unemployment:

- 2026: Low (3.5-4.5%)

- 2027 forecast: Stable (3.5-4.5%)

- Impact: Consumer spending strong, economy healthy

What This Means for Investment Opportunities in 2027

The environment favors:

- ✅ Stocks (lower rates + growth)

- ✅ Dividend investments (income attractive)

- ✅ Real estate (REITs benefit from growth)

- ✅ International markets (US dollar weakening)

Less favorable:

- ⚠️ Long-term bonds (rates falling = existing bonds less valuable)

- ⚠️ Gold (opportunity cost vs stocks)

- ⚠️ Cash (inflation eats returns)

Investment Opportunity #1: High-Yield Savings & Money Market Funds

Best for: Emergency funds and short-term savings in 2027

Why This is an Investment Opportunity in 2027

Current rates (early 2026): 4.5-5.0%

- Highest in 15+ years

- Risk-free (FDIC insured)

- Better than inflation (if inflation 2-3%)

2027 outlook:

- Rates likely decrease to 3.5-4.5%

- Still attractive for cash

- Safe haven in volatility

Best High-Yield Options for 2027

Online Banks:

- Marcus by Goldman Sachs: ~4.5%

- Ally Bank: ~4.4%

- American Express High Yield: ~4.3%

- Capital One 360: ~4.2%

To start taking advantage of high-yield savings as an investment opportunity in 2027, Marcus by Goldman Sachs offers competitive rates with FDIC insurance and no fees, making it ideal for emergency funds and short-term savings.

Money Market Funds:

- Vanguard Federal Money Market (VMFXX): ~5.0%

- Fidelity Government Money Market (SPAXX): ~4.9%

- Schwab Treasury Obligations (SNOXX): ~4.8%

Investment Strategy for 2027

Emergency fund:

- 3-6 months expenses

- High-yield savings account

- FDIC insured

- Instant access

Short-term goals (1-2 years):

- Money market fund

- Treasury bills (more below)

- Safe from market volatility

Amount to allocate: $10,000-50,000 (emergency fund + short-term needs)

Expected return 2027: 3.5-4.5% (safe, guaranteed)

This investment opportunity in 2027 = safety + decent return.

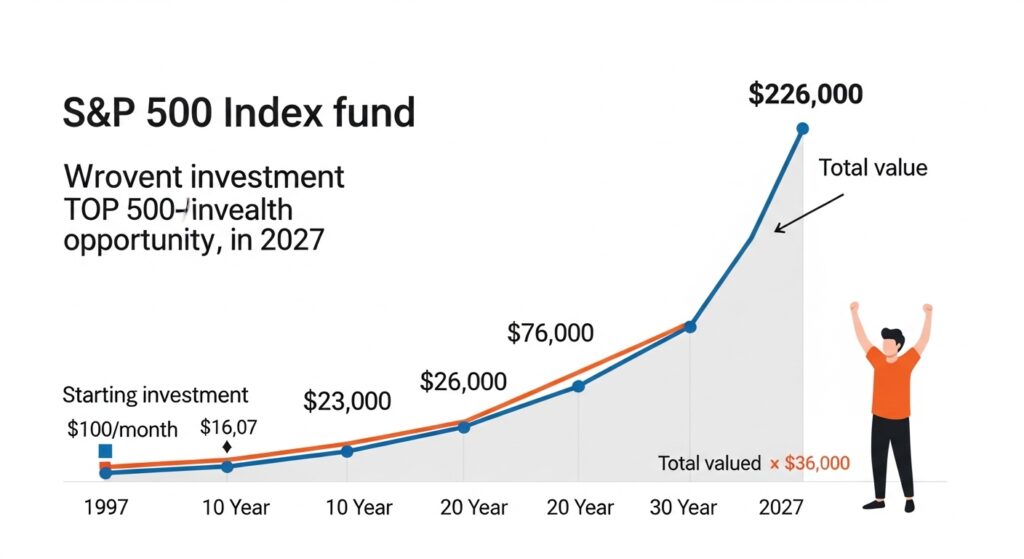

Investment Opportunity #2: S&P 500 Index Funds

Best for: Long-term wealth building in 2027

Why S&P 500 is the #1 Investment Opportunity in 2027

Historical performance:

- Average return: 10-11%/year (since 1926)

- Beats 95% of actively managed funds

- Includes America’s 500 largest companies

- Ultimate diversification

2027 specific reasons:

- Lower interest rates = higher stock valuations

- Corporate earnings growth expected

- AI revolution benefiting large-cap companies

- US economy strong

Best S&P 500 Funds for 2027

To invest in the S&P 500 as a top investment opportunity in 2027, Vanguard’s VOO ETF offers ultra-low fees (0.03%) and has consistently delivered strong long-term returns tracking the S&P 500 index.

ETFs (Exchange Traded Funds):

- VOO (Vanguard): 0.03% fee

- SPY (State Street): 0.09% fee

- IVV (iShares): 0.03% fee

Mutual Funds:

- FXAIX (Fidelity 500 Index): 0.015% fee

- SWPPX (Schwab S&P 500 Index): 0.02% fee

- VFIAX (Vanguard 500 Index Admiral): 0.04% fee

Investment Strategy for 2027

Core holding:

- 40-60% of stock portfolio

- Buy monthly (dollar-cost averaging)

- Never sell (hold 20+ years)

- Reinvest all dividends

Amount to allocate: $5,000-100,000+ (core of portfolio)

Expected return 2027: 8-12% (long-term average, year-to-year varies)

Why S&P 500 is a top investment opportunity in 2027:

- Proven track record

- Lowest fees

- Automatic diversification

- Warren Buffett’s #1 recommendation

For more on index funds, read What Are Index Funds to understand this investment opportunity fully.

Investment Opportunity #3: Dividend Growth Stocks

Best for: Income + growth in 2027

Why Dividend Stocks are an Investment Opportunity in 2027

2027 economic environment favors dividends:

- Mature companies with strong cash flow

- Inflation moderating = dividend purchasing power preserved

- Rates decreasing = dividend yields more attractive

- Recession-resistant businesses

Dividend growth = compound wealth:

- Collect 3-4% yield

- Dividends grow 5-10%/year

- Stock price appreciates

- Total return: 10-15%/year historically

Best Dividend Stocks/Funds for 2027

Dividend ETFs (easiest):

- SCHD (Schwab US Dividend Equity): 3.5% yield, low fees

- VYM (Vanguard High Dividend Yield): 3.2% yield

- DGRO (iShares Core Dividend Growth): 2.5% yield

- VIG (Vanguard Dividend Appreciation): 2.1% yield

Individual Dividend Aristocrats (25+ years consecutive raises):

- Johnson & Johnson: Healthcare, 3.1% yield

- Coca-Cola: Consumer staple, 3.2% yield

- Procter & Gamble: Consumer staple, 2.6% yield

- McDonald’s: Restaurant, 2.4% yield

- 3M: Industrial, 3.7% yield

Investment Strategy for 2027

Income focus:

- 20-40% of stock portfolio

- Dividend ETF (SCHD recommended)

- Reinvest dividends for growth

- Tax-advantaged accounts (Roth IRA, 401k)

Individual stocks (if confident):

- Buy 5-10 dividend aristocrats

- Diversify across sectors

- Hold forever

- Reinvest dividends

Amount to allocate: $3,000-50,000 (depending on income needs)

Expected return 2027: 3-4% yield + 5-8% price appreciation = 8-12% total return

Dividend stocks = investment opportunity in 2027 for passive income.

For understanding dividend power, read The Power of Dividend Investing.

Investment Opportunity #4: Treasury Bonds & I-Bonds

Best for: Conservative investors and inflation protection in 2027

Why Bonds are an Investment Opportunity in 2027

Treasury bonds:

- Ultra-safe (US government backed)

- Current yields: 4-5% (attractive!)

- Lock in high rates before they drop

- Portfolio stabilizer

I-Bonds (inflation-protected):

- Protects against inflation automatically

- Current rate: 5.27% (as of late 2025)

- 2027 rate: Will adjust with inflation

- Tax-deferred

Best Bond Investments for 2027

Short-term Treasuries (1-3 years):

- 2-year Treasury: ~4.2% yield

- 3-year Treasury: ~4.1% yield

- Lower interest rate risk

- Good for near-term needs

Intermediate Treasuries (5-10 years):

- 5-year Treasury: ~4.0% yield

- 10-year Treasury: ~4.3% yield

- Lock in rates before Fed cuts

- Sweet spot for 2027

I-Bonds:

- Purchase limit: $10,000/year per person

- Current rate: Adjusts every 6 months

- Hold 1 year minimum

- Tax-deferred until redeemed

Treasury ETFs:

- SHY (1-3 Year Treasury): Low risk

- IEF (7-10 Year Treasury): Moderate risk

- TLT (20+ Year Treasury): Higher risk in 2027

Investment Strategy for 2027

Conservative allocation (age 50+):

- 30-50% bonds

- Mix: 5-year treasuries (core) + I-Bonds (inflation protection)

Moderate allocation (age 30-50):

- 20-30% bonds

- Focus: Short-term treasuries + I-Bonds

Aggressive allocation (age 20-30):

- 10-20% bonds

- Minimal: I-Bonds mainly

Amount to allocate: $10,000-100,000 (based on age and risk tolerance)

Expected return 2027: 3-5% (safe, predictable)

Bonds = conservative investment opportunity in 2027.

Investment Opportunity #5: Real Estate Investment Trusts (REITs)

Best for: Real estate exposure without buying property in 2027

Why REITs are an Investment Opportunity in 2027

2027 outlook for REITs:

- Interest rates decreasing = REITs more valuable

- Real estate demand strong

- High dividend yields (3-5%)

- Diversification from stocks

Benefits:

- Liquid (trade like stocks)

- No property management

- Diversified across properties

- Monthly/quarterly dividends

Best REITs for 2027

Diversified REIT ETFs:

- VNQ (Vanguard Real Estate ETF): 4.2% yield, broad exposure

- SCHH (Schwab US REIT ETF): 3.9% yield, low fees

- IYR (iShares US Real Estate): 3.7% yield

Individual REITs by sector:

Residential:

- AvalonBay (AVB): Apartments, 3.5% yield

- Equity Residential (EQR): Apartments, 3.7% yield

Healthcare:

- Welltower (WELL): Senior housing, 3.2% yield

- Ventas (VTR): Medical buildings, 3.8% yield

Industrial/Logistics:

- Prologis (PLD): Warehouses, 3.1% yield

- Duke Realty (DRE): Industrial, 2.9% yield

Data Centers (high growth):

- Digital Realty (DLR): 3.5% yield

- Equinix (EQIX): 2.1% yield

Investment Strategy for 2027

Diversified approach:

- 5-15% of total portfolio

- REIT ETF (VNQ recommended)

- Hold in taxable or Roth IRA

- Reinvest dividends

Sector-specific (if confident):

- Healthcare REITs (aging population)

- Data center REITs (AI boom)

- Avoid retail REITs (e-commerce threat)

Amount to allocate: $2,000-30,000

Expected return 2027: 3-5% dividend yield + 4-8% price appreciation = 7-13% total return

REITs = investment opportunity in 2027 for income + real estate exposure.

Investment Opportunity #6: International Markets (Emerging Markets)

Best for: Diversification and higher growth potential in 2027

Why International Markets are an Investment Opportunity in 2027

US dollar expected to weaken in 2027:

- Fed cutting rates

- International investments benefit

- Currency gains + stock gains

Emerging markets undervalued:

- Trading at lower valuations than US

- Faster GDP growth

- Younger demographics

- Infrastructure spending

Top emerging markets for 2027:

- India: 6-7% GDP growth, tech boom

- Vietnam: 6-7% growth, manufacturing

- Brazil: Commodity-rich, recovery

- Mexico: Nearshoring beneficiary

Best International Investment Funds for 2027

Broad international:

- VXUS (Vanguard Total International): Developed + emerging

- IXUS (iShares Core International): Low fee

- SCHF (Schwab International Equity): Developed markets

Emerging markets specific:

- VWO (Vanguard Emerging Markets): Broad EM exposure

- IEMG (iShares Core Emerging Markets): Lower fees

- EEM (iShares Emerging Markets): Most popular

Country-specific:

- INDA (India ETF): 15-20% growth potential

- EWZ (Brazil ETF): Commodity play

- EWW (Mexico ETF): Manufacturing nearshoring

Investment Strategy for 2027

Moderate allocation:

- 20-30% of stock portfolio

- 15% developed international (VXUS)

- 10% emerging markets (VWO)

- Rebalance annually

Aggressive allocation:

- 30-40% international

- 20% emerging markets

- 10% country-specific (India)

Amount to allocate: $3,000-40,000

Expected return 2027: 10-15% (higher risk, higher reward)

International markets = investment opportunity in 2027 for diversification.

Investment Opportunity #7: Technology Sector ETFs

Best for: Growth-focused investors in 2027

Why Technology is an Investment Opportunity in 2027

Mega-trends continuing in 2027:

- Artificial Intelligence (AI) revolution

- Cloud computing growth

- Cybersecurity demand

- 5G and connectivity

- Semiconductor shortage recovery

Tech sector fundamentals:

- Highest profit margins

- Strong cash flows

- Innovation leaders

- Dominant market positions

Best Technology ETFs for 2027

Broad technology:

- QQQ (Nasdaq 100): Top 100 tech companies, 0.20% fee

- VGT (Vanguard Information Technology): Pure tech, 0.10% fee

- XLK (Technology Select Sector): S&P 500 tech, 0.10% fee

AI-focused:

- ARKQ (ARK Autonomous Tech): AI + robotics

- ROBO (Robotics & AI ETF): AI infrastructure

- BOTZ (Global Robotics ETF): Automation

Semiconductor:

- SMH (Semiconductor ETF): Chip makers

- SOXX (iShares Semiconductor): Broad chip exposure

Cloud/SaaS:

- SKYY (Cloud Computing ETF): Cloud leaders

- WCLD (WisdomTree Cloud): SaaS companies

Investment Strategy for 2027

Growth allocation:

- 15-25% of stock portfolio

- Core: QQQ (Nasdaq 100)

- Satellite: SMH (semiconductors) or AI-focused ETF

- Hold long-term

Concentration risk awareness:

- Tech can be volatile

- Don’t overallocate (max 30%)

- Pair with dividend/value stocks

Amount to allocate: $3,000-50,000

Expected return 2027: 12-20% (higher volatility, higher potential)

Technology = high-growth investment opportunity in 2027.

Investment Opportunity #8: Healthcare & Biotech

Best for: Defensive growth in 2027

Why Healthcare is an Investment Opportunity in 2027

Demographic trends:

- Aging population (Baby Boomers 77-85 in 2027)

- Increased healthcare spending

- Medicare growth

- Chronic disease management

Innovation drivers:

- Gene therapy breakthroughs

- Personalized medicine

- AI in drug discovery

- Weight-loss drugs (GLP-1s)

Defensive qualities:

- Recession-resistant (people need healthcare)

- Stable cash flows

- Dividend payers

Best Healthcare Investments for 2027

Broad healthcare ETFs:

- VHT (Vanguard Health Care): Large-cap healthcare

- XLV (Health Care Select Sector): S&P 500 healthcare

- IHI (iShares US Medical Devices): Device makers

Biotech (higher risk/reward):

- XBI (Biotech ETF): Small-cap biotech

- IBB (iShares Biotech): Large-cap biotech

- ARKG (ARK Genomic Revolution): Gene therapy

Healthcare REITs:

- Welltower (WELL): Senior housing

- Ventas (VTR): Medical buildings

Top healthcare companies:

- UnitedHealth Group: Insurance + services

- Johnson & Johnson: Pharma + devices + consumer

- Eli Lilly: Diabetes + weight-loss drugs

- AbbVie: Immunology leader

Investment Strategy for 2027

Conservative-growth allocation:

- 10-20% of stock portfolio

- Core: VHT or XLV (broad healthcare)

- Satellite: Individual stocks (UnitedHealth, Eli Lilly)

Aggressive allocation:

- 15-25% healthcare/biotech

- 10% broad healthcare ETF

- 10% biotech (XBI)

- Higher risk, higher reward

Amount to allocate: $2,000-40,000

Expected return 2027: 9-14% (defensive growth)

Healthcare = stable investment opportunity in 2027.

Investment Opportunity #9: Renewable Energy

Best for: Long-term growth and ESG investors in 2027

Why Renewable Energy is an Investment Opportunity in 2027

Policy support:

- Inflation Reduction Act (IRA) incentives

- Global climate commitments

- Corporate renewable goals

- Grid modernization

Technology improvements:

- Solar costs down 90% since 2010

- Battery storage breakthroughs

- EV adoption accelerating

- Green hydrogen potential

2027 specific catalysts:

- China reopening (demand surge)

- Europe energy independence

- US clean energy mandates

- Investment flowing into sector

Best Renewable Energy Investments for 2027

Broad clean energy ETFs:

- ICLN (iShares Global Clean Energy): Global exposure

- QCLN (First Trust Clean Edge): US + global

- PBW (Invesco WilderHill Clean Energy): Pure-play

Solar:

- TAN (Solar ETF): Solar companies

- Enphase Energy (ENPH): Solar technology

- First Solar (FSLR): US solar manufacturing

Electric Vehicles:

- DRIV (Global Electric Vehicle ETF)

- Tesla (TSLA): EV leader (high volatility)

- Rivian (RIVN): EV startup (high risk)

Utilities (safer play):

- NextEra Energy (NEE): Largest renewable utility

- Brookfield Renewable (BEP): Diversified renewables

Investment Strategy for 2027

Long-term allocation:

- 5-10% of portfolio

- Core: ICLN or QCLN (broad ETF)

- Satellite: NEE (stable utility)

- Hold 5-10 years minimum

Risk awareness:

- Volatile sector (20-30% swings)

- Government policy dependent

- Technology risk

- Not for short-term

Amount to allocate: $1,000-20,000

Expected return 2027: 10-20% (high volatility, growth potential)

Renewable energy = long-term investment opportunity in 2027.

Investment Opportunity #10: Alternative Investments

Best for: Sophisticated investors seeking diversification in 2027

Alternative Investment Options for 2027

Gold/Precious Metals:

- Why: Inflation hedge, currency hedge

- How: GLD (Gold ETF) or physical gold

- Allocation: 5-10% (insurance)

- 2027 outlook: Moderate (USD weakening helps)

Commodities:

- Why: Inflation protection, China demand

- How: DBC (Commodity ETF), GSG (Commodity index)

- Allocation: 5-10%

- 2027 outlook: Positive (infrastructure spending)

Cryptocurrency (high risk):

- Why: Digital gold thesis, blockchain adoption

- How: Bitcoin ETF (IBIT, FBTC), Ethereum ETF

- Allocation: 1-5% maximum (speculation)

- 2027 outlook: Highly uncertain (extreme volatility)

Private Equity/REITs:

- Why: Illiquid premium, diversification

- How: Fundrise (real estate), Masterworks (art)

- Allocation: 5-10% (if accredited)

- 2027 outlook: Strong (alternative to public markets)

Alternative Investment Strategy for 2027

Conservative approach:

- 5% gold (GLD)

- 0% crypto

- Focus on traditional assets

Moderate approach:

- 5-10% gold

- 2% Bitcoin (via ETF)

- 5% commodities

Aggressive approach:

- 10% gold

- 5% crypto (Bitcoin + Ethereum ETFs)

- 10% commodities

- Private investments if qualified

Amount to allocate: $1,000-30,000 (alternatives)

Expected return 2027: Highly variable (-20% to +50%)

Alternatives = speculative investment opportunities in 2027.

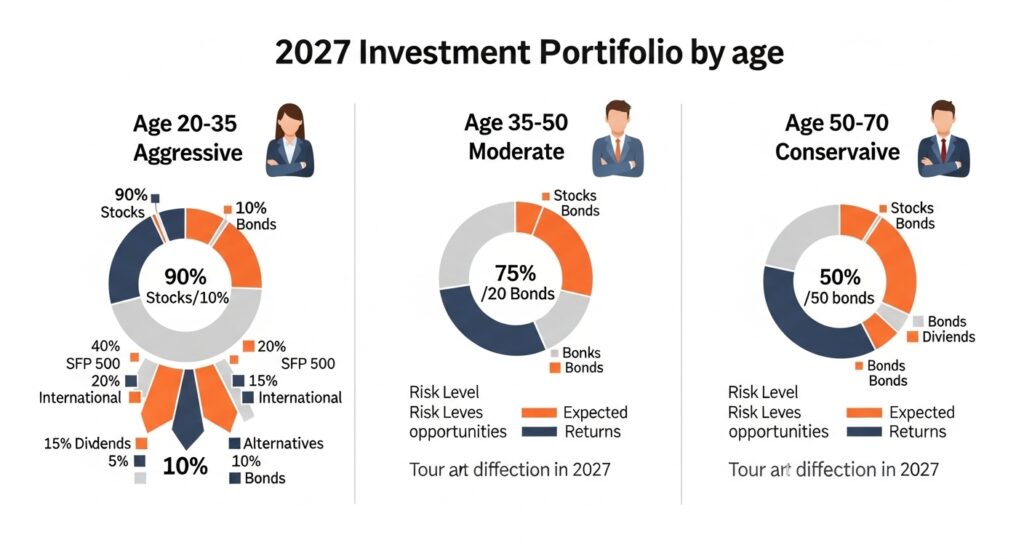

How to Build Your 2027 Investment Portfolio

Putting it all together based on your age and risk tolerance

Conservative Portfolio (Age 50-70)

Goal: Preserve wealth, generate income

Allocation:

- 40% Bonds (Treasuries, I-Bonds)

- 30% S&P 500 Index

- 15% Dividend stocks/ETFs

- 10% REITs

- 5% International

- 0% Speculative

Expected return: 5-7%/year Risk level: Low

Moderate Portfolio (Age 35-50)

Goal: Balanced growth and safety

Allocation:

- 25% Bonds

- 35% S&P 500 Index

- 15% Dividend stocks

- 10% International (emerging markets)

- 10% Technology/Healthcare

- 5% REITs

Expected return: 7-9%/year Risk level: Moderate

Aggressive Portfolio (Age 20-35)

Goal: Maximum growth

Allocation:

- 10% Bonds (I-Bonds)

- 40% S&P 500 Index

- 20% Technology sector

- 15% International (emerging markets)

- 10% Small-cap growth / Biotech

- 5% Alternatives (crypto, gold)

Expected return: 9-12%/year Risk level: High

Rebalancing in 2027

Quarterly or annually:

- Review allocation

- Sell overweight positions

- Buy underweight positions

- Maintain target percentages

Example:

- Target: 60% stocks, 40% bonds

- Current: 70% stocks (market grew), 30% bonds

- Action: Sell 10% stocks, buy 10% bonds

- Back to 60/40

Investment Mistakes to Avoid in 2027

Common errors that will cost you money.

❌ Mistake 1: Chasing Last Year’s Winners

The error:

- 2026 AI stocks +200%

- “I should buy AI stocks in 2027!”

- Buy at peak

- Market corrects, lose money

The reality:

- Past performance ≠ future results

- What’s hot becomes cold

- Timing the market fails

The solution:

- Invest in boring index funds

- Ignore hot trends

- Long-term focus

❌ Mistake 2: Market Timing

The error:

- “Market might crash in 2027, I’ll wait”

- Sits in cash

- Market goes up 15%

- Misses gains

The reality:

- Can’t predict crashes

- Time in market > timing market

- Waiting costs money

The solution:

- Dollar-cost average

- Invest consistently

- Ignore predictions

❌ Mistake 3: Over-Concentration

The error:

- 80% portfolio in one stock

- 60% in crypto

- 90% in tech sector

- One bad year = portfolio destroyed

The solution:

- Diversify across assets

- No single holding over 10-15%

- Broad index funds as core

❌ Mistake 4: Panic Selling

The error:

- Market drops 15% in 2027

- Panic: “I need to get out!”

- Sell everything

- Market recovers, they’re out

The solution:

- Expect volatility

- Have emergency fund (never sell investments for emergencies)

- Hold through downturns

❌ Mistake 5: Ignoring Fees

The error:

- Active mutual fund: 1.5% fee

- Robo-advisor: 1.0% fee

- Financial advisor: 1.0% fee

- Total: 3.5% fees eating returns

The reality:

- $100,000 at 10% return – 3.5% fees = 6.5% actual

- Over 30 years: Fees cost $400,000!

The solution:

- Index funds: 0.03-0.20% fees

- Avoid high-fee products

- DIY investing when possible

Frequently Asked Questions – FAQ 👈

Q: What are the best investment opportunities in 2027 for beginners?

A: S&P 500 index funds and high-yield savings.

Start with:

- Emergency fund in high-yield savings (3-6 months expenses)

- Remaining money in S&P 500 index fund (VOO or FXAIX)

- Hold 20+ years

As you learn:

- Add dividend ETF (SCHD)

- Add international (VXUS)

- Add bonds (treasuries)

Keep it simple: 80% of wealth comes from simple strategies.

For beginner guidance, read How to Start Investing With Little Money.

Q: Should I wait for a market crash in 2027 to invest?

A: No. Start investing now regardless of market level.

Why:

- Can’t predict crashes (nobody can)

- Market up 70% of years

- Waiting costs more than crashes

- Dollar-cost averaging protects you

Strategy:

- Invest monthly regardless of market

- If crash happens: Keep investing (it’s on sale!)

- If crash doesn’t happen: You’re already invested (winning!)

Q: How much should I invest in 2027?

A: 15-20% of income minimum, 30-50% if aggressive.

General rule:

- Age 20-30: Save 15-20% income

- Age 30-40: Save 20-25% income

- Age 40-50: Save 25-30% income

- Age 50+: Save 30-40% income

Priority order:

- Emergency fund (3-6 months)

- Employer 401(k) match (free money!)

- Max Roth IRA ($7,000/year in 2026-2027)

- Additional 401(k)

- Taxable brokerage account

For budgeting to invest more, read The 50/30/20 Budget Rule.

Q: Are investment opportunities in 2027 different from 2026?

A: Minor differences, but core strategy stays the same.

2027 specific factors:

- Interest rates slightly lower (bonds less attractive)

- AI momentum continuing (tech still strong)

- International recovering (more attractive)

- Renewable energy policy support (long-term play)

But fundamentals don’t change:

- Index funds still best

- Diversification still critical

- Long-term investing still wins

Q: What percentage should I allocate to each investment opportunity in 2027?

A: Depends on age and risk tolerance (see portfolio examples above).

Quick guide:

- Age 20-35: 80-90% stocks, 10-20% bonds

- Age 35-50: 70-80% stocks, 20-30% bonds

- Age 50-65: 50-70% stocks, 30-50% bonds

- Age 65+: 40-60% stocks, 40-60% bonds

Within stocks:

- 60-70%: Index funds (S&P 500, total market)

- 10-20%: Dividend stocks

- 10-20%: International

- 5-10%: Sector ETFs (tech, healthcare)

Q: Should I invest in crypto in 2027?

A: Maximum 1-5% if you understand and accept total loss risk.

Reality about crypto:

- Extremely volatile (can drop 50-80%)

- Speculative (no intrinsic value like stocks/bonds)

- Regulation uncertain

- Not an investment, a speculation

If you invest:

- Bitcoin ETF only (IBIT, FBTC)

- Maximum 5% of portfolio

- Accept you might lose it all

- Don’t check daily

Most people: Skip crypto, focus on proven investments.

Your 2027 Investment Action Plan

Step-by-step implementation

January 2027: Foundation

Week 1: Review current portfolio

- Where is money now?

- What’s your current allocation?

- Any high-fee products? (close them)

Week 2: Set 2027 goals

- How much to invest total?

- Monthly contribution amount?

- Target allocation?

Week 3: Open accounts if needed

- Brokerage (Fidelity, Vanguard, Schwab)

- Roth IRA (if not opened)

- 401(k) enrollment

Week 4: Make first investments

- Core: S&P 500 index fund

- Set up automatic monthly contributions

- Enable dividend reinvestment (DRIP)

Q1 2027 (Jan-Mar): Build Core

Monthly:

- Automatic contributions continue

- Don’t check balance daily

- Focus on earning more income

Add:

- Dividend ETF (SCHD) if desired

- International fund (VXUS) if desired

Q2-Q3 2027 (Apr-Sep): Diversify

Quarterly review:

- Check allocation

- Rebalance if needed

- Increase contributions if income grew

Add:

- Bonds (if over age 35)

- REITs (if desired)

- Sector ETFs (tech, healthcare)

Q4 2027 (Oct-Dec): Optimize

Year-end tasks:

- Tax-loss harvesting (sell losers, offset gains)

- Rebalance to target allocation

- Plan 2028 contributions

- Review performance

Increase:

- Raise 401(k) contribution 1-2%

- Raise automatic investments 10-20%

- Set 2028 goals

2028-2030+: Stay the Course

Quarterly:

- 15-minute portfolio check

- Rebalance if more than 5% off target

- Otherwise: Do nothing!

Annually:

- Increase contributions

- Adjust allocation (more bonds as you age)

- Celebrate progress

After 30 years:

- You’re wealthy

- All from identifying investment opportunities in 2027 and acting!

B ONUS

Want to see expert analysis on investment opportunities in 2027?

This video breaks down the top strategies:

FINAL THOUGHTS: Investment Opportunities in 2027 Are Clear

Here’s what most people misunderstand about investment opportunities in 2027:

They think they need to find the “next big thing.”

The next Tesla. The next Bitcoin. The next breakthrough stock that will 100x.

That’s gambling, not investing.

The real investment opportunities in 2027 are the same as 1987, 2007, and 2017:

- Diversified index funds

- Dividend-paying stocks

- Bonds for stability

- Real estate exposure

- International diversification

Boring? Yes. Effective? Absolutely.

The truth about investment opportunities in 2027:

- S&P 500 will beat 95% of investors (like every year)

- Dividend stocks will pay consistent income (like every year)

- Bonds will provide stability (like every year)

- International markets will offer diversification (like every year)

The “secret” to wealth in 2027 isn’t finding secret investments.

The secret is:

- Start investing (today, not tomorrow)

- Contribute consistently (every month, no exceptions)

- Diversify broadly (index funds, not stock picking)

- Hold forever (ignore volatility)

- Increase contributions (as income grows)

Simple strategies executed consistently beat complex strategies executed poorly.

After implementing these investment opportunities in 2027:

Year 1 (2027):

- Invested $15,000

- Portfolio value: $15,800 (5.3% return)

- Building momentum

Year 5 (2031):

- Invested $100,000 total

- Portfolio value: $128,000

- Compound growth visible

Year 10 (2036):

- Invested $250,000 total

- Portfolio value: $387,000

- Wealth building accelerating

Year 30 (2056):

- Invested $900,000 total

- Portfolio value: $2,400,000

- Financially independent

All from boring, proven investment opportunities in 2027.

The question isn’t “What are the best investment opportunities in 2027?”

The question is: “Will I actually invest in them or wait another year?”

Every year you wait costs you tens of thousands in lost compound growth.

The best investment opportunities in 2027 are already here.

Start investing. Stay consistent. Build wealth.

Your future self will thank you.

INTERESTING TOPICS

Want to learn what are index funds to invest in 2027 wisely?

Need to understand how to start investing with little money in 2027?

Ready to learn the 50/30/20 budget rule to free up money to invest in 2027?

Want more financial insights delivered to you? Subscribe to our newsletter

and get weekly articles with practical strategies to grow your wealth sent straight to your inbox.

Obs: Sign up for our newsletter and receive a free Finance For Beginner eBook.

Disclaimer: This article is for educational purposes only. Diversification does not guarantee profits or protect against all losses. Consider your financial situation, risk tolerance, and investment timeline before making investment decisions.

—— End of Article ——