How to Build Wealth After 40: The Complete Guide

Starting Late Doesn’t Mean Starting Behind

Last updated: May 2026

You’re 40. Or 45. Or 50.

You haven’t saved for retirement.

You have minimal investments. Maybe significant debt.

Everyone says “start investing young.” But what if you didn’t?

What if you’re starting now to build wealth after 40?

Most financial advice ignores people who build wealth after 40:

- Articles about “compound interest over 40 years” (you don’t have 40 years)

- Advice to “save 15% in your 20s” (you’re 40, not 20)

- Retirement calculators showing you need $2 million (discouraging)

- Success stories of people who started at 22 (irrelevant to you)

Traditional wealth advice assumes you started young.

But millions need to build wealth after 40. You’re not alone.

Here’s the truth: You CAN build wealth after 40. It requires different strategies than starting at 25, but it’s absolutely achievable. Late start doesn’t mean no wealth—it means focused strategy.

The wealthy understand something critical: When you build wealth after 40, you have advantages young people don’t: higher income, wisdom, focus, fewer distractions. Use these advantages strategically.

This article was prepared especially for Finance For Beginner subscribers who requested this type of content due to the challenges they face in their personal and professional finances, for a better understanding.

Therefore, we hope that the topic will also be relevant to other users of the same age group who are always present here following our content weekly.

In this guide, you’ll learn exactly how to build wealth after 40, why starting late has hidden advantages, realistic wealth targets by age, aggressive saving strategies that work, investment approaches for late starters, how to catch up on retirement, and most importantly—how to build significant wealth in 15-25 years even starting from zero today.

By the end, you’ll have a complete action plan to build wealth after 40 and retire comfortably.

Let’s build your wealth, starting now.

Why Building Wealth After 40 Is Different (But Not Impossible)

Understanding the unique challenge to build wealth after 40.

The Math Problem

Starting at 25 vs. 40:

Person A (starts at 25):

- Invest $500/month

- 40 years to age 65

- 8% return

- Result: $1,745,000

Person B (starts at 40):

- Invest $500/month

- 25 years to age 65

- 8% return

- Result: $438,000

15-year head start = $1,307,000 more wealth

This is why starting early matters. But it doesn’t mean building wealth after 40 is impossible.

Why It’s Harder to Build Wealth After 40

Challenge 1: Less time for compound growth

- 25 years vs. 40 years

- Compound interest needs time

- Later years create most wealth

- Starting late misses peak growth years

Challenge 2: Competing priorities

- Kids in college (tuition)

- Aging parents (care costs)

- Mortgage remaining

- Life expenses higher

Challenge 3: Lifestyle inflation

- Accustomed to current lifestyle

- Harder to drastically cut spending

- Expectations established

- Big house, nice car = expensive

Challenge 4: Less margin for error

- Market crash at 25: Recover in 5 years

- Market crash at 55: Retiring soon

- Less time to bounce back from mistakes

These challenges are real. But so are solutions.

Why It’s Still Achievable to Build Wealth After 40

Advantage 1: Higher income

- 40s-50s = peak earning years

- 2-3X income vs. 20s

- More money to save

- Can invest larger amounts

Advantage 2: Fewer expenses (often)

- Kids becoming independent

- Paid off some debts

- No longer “starting out”

- Can redirect money to wealth

Advantage 3: Wisdom and focus

- Know what matters

- Less tempted by waste

- Focused on goals

- Fewer frivolous purchases

Advantage 4: Urgency creates action

- Deadline focuses mind

- No time to procrastinate

- Serious about wealth building

- More disciplined

You can absolutely build wealth after 40. Just requires different approach.

The Hidden Advantages of Building Wealth After 40

Why starting late has surprising benefits when you build wealth after 40

Advantage 1: Peak Earning Power

Income by age (typical):

- Age 25: $40,000/year

- Age 30: $55,000/year

- Age 40: $75,000/year

- Age 50: $90,000/year

- 40s-50s = Highest income years

What this means when you build wealth after 40:

- Can save $1,500-3,000/month (vs. $300 at 25)

- Larger contributions compensate for less time

- One year at 40 = Multiple years at 25

Example:

- $500/month at 25 for 15 years = $175,000

- $2,000/month at 40 for 15 years = $700,000

- Higher income makes up for late start

Advantage 2: Life Experience and Wisdom

At 40, you’ve learned:

- What spending brings happiness (what doesn’t)

- How to avoid scams and get-rich-quick schemes

- The difference between needs and wants

- How to make decisions without peer pressure

At 25:

- Still figuring out life

- Easily influenced

- Trying to impress others

- Wasting money on status

Wisdom accelerates wealth when you build wealth after 40.

Advantage 3: Established Career

At 40:

- Proven track record

- Valuable skills

- Professional network

- Easier to increase income (promotions, consulting, side work)

At 25:

- Entry level

- Proving yourself

- Limited network

- Lower earning potential

Your career foundation helps build wealth after 40.

Advantage 4: Fewer Competing Life Goals

At 25-35:

- Building career

- Finding partner

- Having children

- Buying first home

- Establishing life

- Wealth competes with everything

At 40+:

- Career established

- Family situation stable

- Home purchased

- Life foundation built

- Can focus intensely on wealth

Focus is powerful when you build wealth after 40.

Advantage 5: Urgency Creates Discipline

Starting at 25:

- “Plenty of time”

- Can skip months

- Not urgent

- Easy to procrastinate

Starting at 40:

- “Limited time”

- Every year counts

- Very urgent

- Extreme discipline

Deadline focuses action to build wealth after 40.

For more on investing strategies, see what are index funds.

Realistic Wealth Targets When You Build Wealth After 40

Setting achievable goals to build wealth after 40.

Age 40 Starting Point

If starting from zero at 40:

Conservative scenario ($1,000/month saved):

- Age 50: $183,000

- Age 55: $358,000

- Age 60: $587,000

- Age 65: $880,000

Moderate scenario ($2,000/month saved):

- Age 50: $366,000

- Age 55: $716,000

- Age 60: $1,174,000

- Age 65: $1,760,000

Aggressive scenario ($3,000/month saved):

- Age 50: $549,000

- Age 55: $1,074,000

- Age 60: $1,761,000

- Age 65: $2,640,000

All at 8% return. You CAN build wealth after 40 to retire comfortably.

Age 45 Starting Point

If starting from zero at 45:

Conservative ($1,000/month):

- Age 55: $183,000

- Age 60: $358,000

- Age 65: $587,000

- Age 70: $880,000

Moderate ($2,000/month):

- Age 55: $366,000

- Age 60: $716,000

- Age 65: $1,174,000

- Age 70: $1,760,000

Starting at 45 means work 5 years longer OR save more aggressively.

Still achievable to build wealth after 40.

Age 50 Starting Point

If starting from zero at 50:

Aggressive required ($2,500/month):

- Age 60: $458,000

- Age 65: $893,000

- Age 70: $1,468,000

Very aggressive ($4,000/month):

- Age 60: $733,000

- Age 65: $1,429,000

- Age 70: $2,349,000

Starting at 50 requires very aggressive saving. But still possible to build wealth after 40.

How Much Is “Enough”?

Retirement need calculation:

4% withdrawal rule:

- Need $40,000/year → Need $1,000,000

- Need $60,000/year → Need $1,500,000

- Need $80,000/year → Need $2,000,000

Most people need $1,000,000-1,500,000 to retire comfortably.

All scenarios above show this IS achievable when you build wealth after 40 with discipline.

Step 1: Face Your Current Reality (The Honest Assessment)

First step to build wealth after 40: Know where you stand.

Calculate Your Current Net Worth

Assets:

- Savings accounts: $______

- Retirement accounts (401k, IRA): $______

- Investment accounts: $______

- Home equity: $______

- Other assets: $______

- Total Assets: $______

Liabilities:

- Mortgage: $______

- Credit cards: $______

- Student loans: $______

- Car loans: $______

- Other debts: $______

- Total Liabilities: $______

Net Worth = Assets – Liabilities = $______

This is your starting point to build wealth after 40.

Calculate Years Until Retirement

Current age: ___ years

Target retirement age: ___ years (usually 65-70)

Years remaining: ___ years

This is your timeline to build wealth after 40.

Calculate Required Savings Rate

Formula:

Required Monthly Savings = (Target Wealth - Current Wealth) / (Months Until Retirement × Growth Factor)Example:

- Current: $50,000

- Target: $1,000,000

- Age: 45

- Retirement: 65 (20 years)

- Growth factor at 8%: ~1.5

Calculation:

- Need: $950,000 more

- Have: 240 months

- Required: ~$2,600/month

This shows what’s needed to build wealth after 40.

Face the Truth

Three possible realities:

Reality 1: Can hit target

- Income supports required savings

- Achievable with discipline

- Execute the plan

Reality 2: Need to adjust target

- Required savings too high

- Lower target OR work longer

- Still build significant wealth after 40

Reality 3: Need dramatic changes

- Increase income significantly

- Cut expenses drastically

- OR both

- Requires major life changes to build wealth after 40

Honesty now = Better plan = Success to build wealth after 40.

Step 2: Set Aggressive Savings Rate (30-50%)

Critical strategy to build wealth after 40

Why 30-50% Savings Rate?

Normal advice: Save 15%

- Works when starting at 25

- NOT enough when starting at 40

- Need to compensate for lost time

To build wealth after 40: Save 30-50%

- Aggressive but necessary

- Makes up for late start

- Achieves retirement goals

The math:

15% savings rate at 40:

- $75,000 income

- Save $11,250/year ($938/month)

- 25 years to 65

- Result: $365,000

- Insufficient for retirement

40% savings rate at 40:

- $75,000 income

- Save $30,000/year ($2,500/month)

- 25 years to 65

- Result: $973,000

- Comfortable retirement achieved

High savings rate is non-negotiable to build wealth after 40.

How to Achieve 30-50% Savings Rate

Strategy 1: Income split

- Live on one income (if couple)

- Save entire second income

- Instant 50% savings rate

Strategy 2: Lifestyle rollback

- Live like you did at 30

- Bank raises from last 10 years

- Significant savings possible

Strategy 3: Housing reduction

- Downsize home

- Move to lower cost area

- Save $1,000-2,000/month

Strategy 4: Extreme frugality (temporary)

- 5-10 years of sacrifice

- Build foundation

- Then ease up slightly

Strategy 5: Income increase + expense control

- Increase income 30%

- Keep expenses flat

- All increase → savings

Real Example

Age 40, $80,000 income:

Before (10% savings):

- Take-home: $60,000/year

- Save: $6,000/year ($500/month)

- Spend: $54,000/year

After (40% savings):

- Take-home: $60,000/year

- Save: $24,000/year ($2,000/month)

- Spend: $36,000/year

Changes to spend $36k instead of $54k:

- Downsize home: -$800/month

- Sell second car: -$400/month

- Cut dining out: -$300/month

- Cancel subscriptions: -$100/month

- Reduce shopping: -$300/month

- Lower utility/phone: -$100/month

- Total savings: $2,000/month

Painful? Yes. Temporary? Yes. Necessary to build wealth after 40? Absolutely.

For budgeting strategies, see the 50/30/20 budget rule.

Step 3: Maximize Catch-Up Contributions

Special advantage when you build wealth after 40.

What Are Catch-Up Contributions?

IRS allows extra retirement contributions at age 50+:

401(k) catch-up (age 50+):

- Normal limit: $23,000/year (2026)

- Catch-up: +$7,500/year

- Total: $30,500/year

IRA catch-up (age 50+):

- Normal limit: $7,000/year (2026)

- Catch-up: +$1,000/year

- Total: $8,000/year

These are designed specifically to help build wealth after 40.

For the most current catch-up contribution limits and retirement account rules, visit the IRS Retirement Topics page for official guidance on maximizing your retirement savings after 40.

Why Catch-Up Contributions Matter

Without catch-up (age 40-65):

- Max 401(k): $23,000/year × 25 years = $575,000 contributed

- With growth: $1,775,000

With catch-up (age 50-65):

- Age 40-49: $23,000/year × 10 years = $230,000

- Age 50-65: $30,500/year × 15 years = $457,500

- Total contributed: $687,500

- With growth: $2,120,000

Catch-up contributions add $345,000 extra wealth when you build wealth after 40.

How to Max Catch-Up Contributions

Strategy 1: Automate increases at 50

- Set calendar reminder

- Increase 401(k) contribution automatically

- From 15% to 20%+ at age 50

Strategy 2: Bonus redirects

- All bonuses to retirement

- Tax refunds to IRA

- Windfalls to catch-up

Strategy 3: Side hustle dedicated

- Side income specifically for catch-up

- $625/month side hustle = $7,500/year catch-up funded

- Main income for living, side income for catch-up

Tax Benefits

Catch-up contributions are pre-tax:

$7,500 catch-up contribution:

- At 24% tax bracket

- Saves $1,800 in taxes

- Real cost: $5,700

- Government subsidizing your wealth building after 40

Maximize this advantage.

Step 4: Invest Aggressively (You Have Time)

Investment strategy to build wealth after 40.

The “You’re Too Old for Stocks” Myth

Traditional advice:

- “Your bond allocation should equal your age”

- At 40: 40% bonds, 60% stocks

- At 50: 50% bonds, 50% stocks

- Too conservative for late starters

To build wealth after 40, this doesn’t work:

- Bonds return 3-4%

- Not enough growth

- Won’t reach retirement goals

Aggressive Allocation for Building Wealth After 40

Recommended:

Age 40-50:

- 90-100% stocks

- 0-10% bonds

- Aggressive growth needed

Age 50-55:

- 80-90% stocks

- 10-20% bonds

- Still aggressive

Age 55-60:

- 70-80% stocks

- 20-30% bonds

- Starting to protect gains

Age 60-65:

- 60-70% stocks

- 30-40% bonds

- Transitioning to retirement

More aggressive than traditional because you NEED growth to build wealth after 40.

Why This Works

You have 15-25 years:

- Long enough to recover from crashes

- Market crashes last 1-3 years

- Have 22 years minimum to age 65

- Time for volatility

Example:

- Age 40, invest $2,000/month

- 100% stocks (10% return) for 25 years

- Result: $2,657,000

- Age 40, invest $2,000/month

- 60% stocks/40% bonds (6% return) for 25 years

- Result: $1,395,000

Conservative approach costs $1,262,000 when building wealth after 40.

What to Invest In

Simple, low-cost approach:

Core holding: S&P 500 Index Fund

- VOO, FXAIX, SPY

- 0.03% fee

- Tracks 500 largest US companies

- Historically 10% return

Or: Total Stock Market Index

- VTI, FSKAX

- Even broader diversification

- Similar returns

Small International allocation (optional):

- 10-20% international stocks

- VXUS, FTIHX

- Geographic diversification

Avoid:To open a brokerage account and start investing in low-cost index funds for wealth building after 40, Vanguard offers some of the lowest-cost options with excellent long-term performance.

- ❌ Individual stocks (too risky)

- ❌ Crypto (too volatile)

- ❌ Actively managed funds (high fees)

- ❌ Complex strategies

Simple, aggressive, low-cost = Best to build wealth after 40.

Step 5: Eliminate Debt Fast (Priority #1)

Critical foundation to build wealth after 40

Why Debt Stops Wealth After 40

Debt = Negative wealth:

- $300/month car payment = $300 NOT invested

- $300 invested at 40 for 25 years = $262,000

- Car payment costs $262,000 in wealth

Interest = Money to banks, not you:

- Credit card at 20% = Losing 20%

- Investment at 8% = Gaining 8%

- 28% opportunity cost

Debt = Psychological burden:

- Stress

- Limits flexibility

- Prevents aggressive investing

To build wealth after 40: Eliminate debt FIRST, then invest aggressively.

Debt Elimination Priority

Pay off in this order:

1. Credit cards (20% interest)

- Highest interest

- Most expensive

- Eliminate first

- Minimum on others, avalanche on credit cards

2. Personal loans (10-15% interest)

- High interest

- Significant cost

- Second priority

3. Car loans (5-8% interest)

- Moderate interest

- Consider paying off vs. investing

4. Student loans (4-7% interest)

- Lower interest

- May continue paying minimums

- While investing simultaneously

5. Mortgage (3-5% interest)

- Lowest interest

- Often keep and invest instead

- Unless 10 years or less remaining

Aggressive Debt Payoff

Example:

Age 40, $30,000 credit card debt:

Minimum payments:

- $600/month

- 12 years to pay off

- $56,000 total paid

- Cannot build wealth during this time

Aggressive payoff:

- $2,000/month

- 18 months to pay off

- $32,000 total paid

- Debt-free by 42, can invest aggressively for 23 years

Result by 65:

- Aggressive: Debt gone early, invested $2,000/month for 23 years = $1,499,000

- Minimum: Debt lingers, invested $2,000/month for 13 years = $548,000

- $951,000 difference

Fast debt payoff enables building wealth after 40.

Strategies to Eliminate Debt Fast

Strategy 1: Debt snowball/avalanche

- List all debts

- Pay minimum on all except one

- Attack highest interest with intensity

- When paid, roll to next

- Momentum builds

Strategy 2: Balance transfer (if good credit)

- 0% APR for 12-18 months

- Pay off during 0% period

- Save interest

Strategy 3: Sell assets to pay debt

- Second car → $10,000 → Eliminate debt

- Declutter home → $2,000 → Pay debt

- Short-term sacrifice, long-term wealth

Strategy 4: Side hustle dedicated to debt

- $1,000/month side income

- 100% to debt

- Debt gone in months, not years

Debt elimination = Foundation to build wealth after 40.

For more on debt elimination, see how to get out of debt when broke.

Step 6: Increase Income Dramatically

Essential strategy to build wealth after 40.

Why Income Increase Matters More After 40

Expense cutting has limits:

- Can only cut to necessities

- Quality of life suffers

- Burnout risk

- Limited ceiling

Income increase has no ceiling:

- Can earn unlimited extra

- Doesn’t require sacrifice

- Improves quality of life

- Accelerates wealth building after 40

$500/month expense cuts vs. $2,000/month income increase:

- Cuts save $500

- Income adds $2,000

- 4X the impact

Career Income Strategies

Strategy 1: Negotiate major raise

- At 40+, have leverage

- Proven track record

- Market rate research

- Ask for 15-25% raise

- OR threaten to leave

Example:

- $75,000 current

- 20% raise = $90,000

- Extra $15,000/year = $1,250/month

- Invested for 20 years = $744,000 extra wealth

Strategy 2: Job hopping

- Change companies for 20-40% raise

- Loyalty doesn’t pay anymore

- Every 2-3 years = 20%+ increase

- Accelerated path to build wealth after 40

Example:

- Age 40: $70,000

- Age 42: Switch to $85,000 (+21%)

- Age 45: Switch to $105,000 (+24%)

- Age 48: Switch to $130,000 (+24%)

- 8 years, nearly doubled income

Strategy 3: Consulting/freelancing

- Leverage expertise

- Charge $100-200/hour

- 10 hours/week = $4,000-8,000/month

- While keeping day job

Strategy 4: Management promotion

- Seek leadership roles

- Manager salaries 30-50% higher

- Career acceleration

- More wealth building capacity after 40

Side Income Strategies

High-value side hustles:

Consulting in your field:

- $100-300/hour

- 5-10 hours/week

- $2,000-6,000/month additional

- Expertise-based, no startup cost

Online course creation:

- Create once, sell repeatedly

- $500-5,000/month passive

- Scales without time

Real estate side income:

- Rent spare room: $500-1,500/month

- House hack

- Immediate cash flow

Contract work:

- Short-term projects

- Higher hourly rate

- Flexible schedule

Goal: Add $1,000-3,000/month to accelerate building wealth after 40.

For more income ideas, see how to make money from home.

Step 7: Build Multiple Income Streams

Advanced strategy to build wealth after 40.

Why Multiple Income Streams Matter

Single income:

- Risky (job loss = $0)

- Limited growth potential

- One ceiling

- Resilient (one drops, others continue)

- Unlimited growth

- Multiple paths to build wealth after 40

The 3-Income Strategy

Income Stream 1: Primary job

- Main income

- Stable, predictable

- $75,000/year example

Income Stream 2: Side business/consulting

- Expertise-based

- Flexible hours

- $20,000/year example

Income Stream 3: Investment income

- Dividend stocks

- Rental property

- Growing over time

- $5,000/year initially, growing

Total: $100,000/year (vs. $75,000 single income)

Extra $25,000/year = $2,083/month to build wealth after 40.

Building Streams Progressively

Year 1-2 (Age 40-42):

- Focus on primary job + debt elimination

- Single income, aggressive debt payoff

Year 3-5 (Age 43-45):

- Debt eliminated

- Start side income ($500-1,000/month)

- Begin building Stream 2

Year 6-10 (Age 46-50):

- Side income mature ($1,500-2,000/month)

- Investment income starting ($200-500/month)

- Three streams flowing

Year 11-20 (Age 51-60):

- All three streams significant

- Primary: $90,000

- Side: $30,000

- Investment: $20,000

- Total: $140,000/year

- Can save $4,000-6,000/month to build wealth after 40

Investment Income Stream

Building passive income:

Dividend stocks:

- $100,000 invested in dividend stocks

- 3-4% dividend yield

- $3,000-4,000/year passive

- Reinvested initially, income later

Rental property:

- $300,000 property

- $1,500/month cash flow after expenses

- $18,000/year passive income

- Builds equity + income

Investment income compounds:

- Year 1: $3,000

- Year 5: $8,000

- Year 10: $20,000

- Year 20: $60,000

- Significant by retirement

Multiple streams = Stable path to build wealth after 40.

Real Examples: People Who Built Wealth After 40

Proof it’s possible to build wealth after 40.

Example 1: The Late Bloomer

Profile:

- Age 42 starting

- $15,000 in savings (minimal)

- $60,000/year income

- No retirement accounts

Strategy:

- Maximized 401(k): $1,500/month

- Side consulting: $800/month

- Total: $2,300/month invested

- 23 years to age 65

Result:

- Age 65: $1,782,000

- Started with almost nothing at 42

- Retired comfortably by building wealth after 40

Example 2: The Career Switcher

Profile:

- Age 45 starting

- Career change (higher income)

- $30,000 existing

- $0 debt

Strategy:

- New income: $95,000/year

- Lived on $50,000, saved $45,000/year ($3,750/month)

- 50% savings rate

- 20 years to age 65

Result:

- Age 65: $2,900,000 (including initial $30k)

- Aggressive savings + time

- Wealthy retirement by building wealth after 40

Example 3: The Downsizer

Profile:

- Age 48 starting

- $50,000 existing

- $80,000 income

- Expensive lifestyle

Strategy:

- Sold large house, bought smaller

- Eliminated car payment

- Reduced lifestyle

- Saved $3,000/month freed from cuts

- 17 years to age 65

Result:

- Age 65: $1,250,000

- Lifestyle changes enabled wealth

- Comfortable retirement by building wealth after 40

Common Themes

All three:

- ✅ Started with little

- ✅ High savings rate (30-50%)

- ✅ Consistent investing

- ✅ Sacrificed lifestyle temporarily

- ✅ Never gave up

- ✅ Successfully built wealth after 40

You can too.

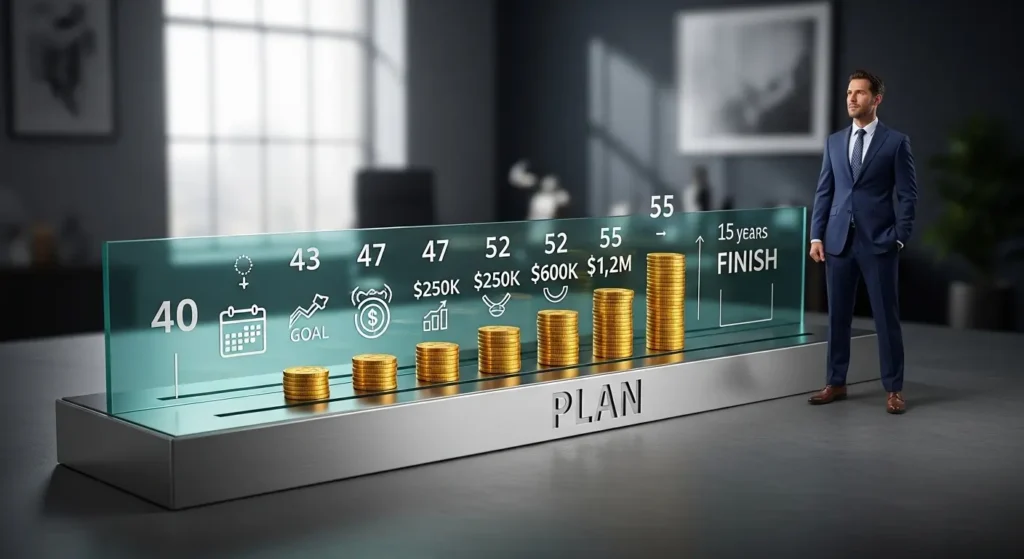

The 15-Year Wealth Building Plan (Ages 40-55)

Detailed roadmap to build wealth after 40

Years 1-3 (Ages 40-43): Foundation

Focus: Eliminate debt + Build habits

Actions:

- Pay off all credit cards (aggressive)

- Pay off car loans

- Eliminate personal loans

- Start investing minimum 15% (even while paying debt)

- Build $5,000 emergency fund

Target by 43:

- Zero high-interest debt

- $50,000 invested

- Saving 25% income

Years 4-7 (Ages 44-47): Acceleration

Focus: Aggressive wealth accumulation

Actions:

- Increase savings to 35-40%

- Max 401(k) contributions

- Open Roth IRA, max it

- Start side income stream

- Invest every raise

Target by 47:

- $250,000 invested

- Side income: $800/month

- Saving 40% income

Years 8-12 (Ages 48-52): Momentum

Focus: Multiple income streams + Max retirement

Actions:

- Catch-up contributions (age 50+)

- Side income mature: $1,500-2,000/month

- Consider investment property

- Negotiate major raise or switch jobs

- Keep lifestyle flat despite income growth

Target by 52:

- $600,000 invested

- 3 income streams active

- Saving 45-50% income

Years 13-15 (Ages 53-55): Final Push

Focus: Maximize every dollar

Actions:

- Max everything (401k + catch-up, IRA + catch-up)

- All bonuses to investments

- Consider working extra years (power of 2-3 more years)

- Evaluate early retirement possibility

Target by 55:

- $1,000,000-1,200,000 invested

- Options: Retire early, coast, or keep building

- Wealthy by building consistently after 40

Years 16-20 (Optional: Ages 56-60)

If continue working:

- $1,500,000-2,000,000 by 60

- Extremely comfortable retirement

- Financial independence achieved

- Success building wealth after 40 complete

What If You’re Starting at 50? (The 10-Year Plan)

Aggressive plan to build wealth after 40 starting late.

The Reality Check

Starting at 50 = 10-15 years to retirement:

- Less time than starting at 40

- Requires even more aggressive approach

- BUT still achievable to build wealth after 40

Required savings rate: 40-60%

- Higher than starting at 40

- Necessary to hit goals

- Temporary sacrifice

The 10-Year Blitz (50-60)

Year 1 (Age 50): Setup

- Eliminate all debt immediately

- Set up retirement accounts

- Max contributions + catch-up

- Start investing $3,000-4,000/month minimum

Years 2-5 (Ages 51-55): Accumulation

- 50%+ savings rate

- Side income: $1,000-2,000/month

- All extra income to investments

- Live extremely frugally

Target by 55: $450,000 invested (from $0 at 50)

Years 6-10 (Ages 56-60): Final Sprint

- Maintain intensity

- Don’t ease up

- Consider working past 60

- Every year adds significantly

Target by 60: $900,000 invested

Years 11-15 (Ages 61-65): Coast or Continue

- Option A: Retire at 65 with $1,400,000

- Option B: Work to 67, retire with $1,800,000

Starting at 50, you CAN build wealth after 40 to retire comfortably.

Requires extreme focus.

Strategies for 50+ Starters

1. Work longer

- Retire at 67-70 instead of 65

- 2-5 extra years = 30-50% more wealth

- Social Security benefits increase

- Gives more time to build wealth after 40

2. Extreme income boost

- Consulting at $150/hour

- 10 hours/week = $6,000/month

- Career change to higher paying

- Everything toward wealth

3. Lifestyle downsizing

- Sell house, move to apartment

- Eliminate car

- Reduce expenses 50%

- Save difference

4. Part-time retirement

- “Retire” at 62

- Work part-time (lower stress)

- Let investments grow

- Supplement with part-time income

Starting at 50 is harder but not impossible to build wealth after 40.

Common Mistakes When Building Wealth After 40

Errors that derail plans to build wealth after 40.

Mistake 1: Believing It’s Too Late

The error:

- “I’m 45, too late to save for retirement”

- Give up without trying

- Continue bad habits

- Ensure failure

The reality:

- 20 years is PLENTY of time

- Can build $1,000,000+ wealth

- Others have done it

The solution:

- Start TODAY

- 20 years of action beats 40 years of nothing

- Never too late to build wealth after 40

Mistake 2: Not Being Aggressive Enough

The error:

- Save 10-15% (normal advice)

- “I’m doing something”

- Insufficient for late start

- Won’t hit retirement goals

The reality:

- 10-15% works when starting at 25

- At 40+, need 30-50%

- Math requires aggression

The solution:

- Calculate required savings

- Hit the number

- Temporary sacrifice

- Aggressive necessary to build wealth after 40

Mistake 3: Keeping Lifestyle Inflation

The error:

- Income increases

- Lifestyle increases equally

- Never increase savings rate

- Perpetually behind

The solution:

- Lock lifestyle at current level

- Bank all raises and bonuses

- Income growth = Wealth growth

- Lifestyle discipline crucial to build wealth after 40

Mistake 4: Not Increasing Income

The error:

- Focus only on cutting expenses

- Hit spending floor

- Can’t save more

- Stagnant wealth building

The solution:

- Increase income 20-50%

- Career moves, side hustles

- No ceiling on income

- Income growth accelerates building wealth after 40

Mistake 5: Being Too Conservative

The error:

- “I’m 45, can’t handle risk”

- 50% bonds

- 4% returns

- Insufficient growth

The reality:

- Have 20+ years

- Need 8-10% returns

- Stocks necessary

- Time for volatility

The solution:

- 80-90% stocks

- Low-cost index funds

- Ride the volatility

- Growth needed to build wealth after 40

Frequently Asked Questions – FAQ 👈

Q: Can I really build wealth after 40 starting from zero?

A: Yes. With 30-50% savings rate, absolutely achievable.

Real numbers:

Age 40, $0 current, $75,000 income:

- Save 40% = $30,000/year ($2,500/month)

- 25 years to age 65

- 8% return

- Result: $2,433,000

Age 45, $0 current, $80,000 income:

- Save 45% = $36,000/year ($3,000/month)

- 20 years to age 65

- 8% return

- Result: $1,761,000

Both achieve comfortable retirement by building wealth after 40.

Q: Should I pay off my mortgage early or invest?

A: Depends on interest rate and timeline.

Mortgage under 4%:

- Keep mortgage

- Invest extra money (8% return beats 4% interest)

- Better wealth building after 40

Mortgage over 5%:

- Consider paying off

- Guaranteed 5% “return”

- Then invest mortgage payment amount

Close to retirement (5 years):

- Pay off mortgage

- Peace of mind

- Lower retirement income needed

10+ years to retirement:

- Keep mortgage, invest

- Better to build wealth after 40**

Q: What if I lose my job in my 50s?

A: Having built wealth helps, plus backup plans.

If building wealth after 40:

- Have emergency fund (6-12 months)

- Can survive unemployment

- Resume wealth building when employed

Without wealth:

- No buffer

- Devastating

- Hard to recover

Also:

- Multiple income streams protect

- Consulting skills valuable

- Can find work at any age

Building wealth after 40 provides resilience.

Q: Should I help my kids with college or save for retirement?

A: Secure your retirement FIRST.

Hard truth:

- Can’t borrow for retirement

- CAN borrow for college

- Your financial security matters

Strategy:

- Prioritize retirement savings

- Help with college if surplus

- Kids benefit more from stable parents than debt-free degree + broke parents

When building wealth after 40, retirement must be priority #1.

Q: Is it worth working past 65 to build more wealth?

A: Often yes, especially if starting late.

Working 65-70 (5 extra years):

- Wealth continues growing

- Social Security benefit increases (8%/year)

- Don’t draw from savings yet

- Can increase retirement wealth 40-50%

Example:

- Retire at 65: $1,000,000

- Work to 70: $1,500,000

- $500,000 difference for 5 years

If enjoy work and healthy, working longer supercharges building wealth after 40.

Your Wealth After 40 Action Plan

Step-by-step plan to build wealth after 40 starting this week.

Week 1: Assessment

Day 1-2: Calculate reality

- Net worth: $______

- Years to retirement: ___

- Required savings: $______/month

Day 3-4: Set targets

- Target net worth at retirement: $______

- Monthly savings goal: $______

- Savings rate: ____%

Day 5-7: Create budget

- Current expenses: $______

- Reduced expenses: $______

- Savings freed: $______

Month 1-3: Foundation

Actions:

- Open retirement accounts (401k, IRA)

- Start automatic contributions

- List all debts

- Create debt payoff plan

- Build $1,000 emergency fund

Goals:

- Investing minimum 20%

- Debt payoff plan active

- Baseline established

Month 4-12: Acceleration

Actions:

- Increase savings to 30-35%

- Pay off first high-interest debt

- Start side income research

- Negotiate raise

- Increase emergency fund to $5,000

Goals:

- $10,000-30,000 invested (depending on income)

- One debt eliminated

- Income increased

Year 2-3: Intensity

Actions:

- 35-40% savings rate

- Major debts eliminated

- Side income: $500-1,000/month

- Max 401(k) contributions

- Stay focused

Goals:

- $50,000-150,000 invested

- Most debt gone

- Multiple income streams starting

Year 4-10: Momentum

Actions:

- 40-50% savings rate (at age 50+)

- Catch-up contributions (age 50+)

- Side income: $1,000-2,000/month

- Max everything

- Never ease up

Goals:

- $300,000-700,000 invested

- Debt-free

- Wealth building automatic

Year 11-20: Victory

Actions:

- Maintain intensity

- Watch wealth compound

- Evaluate early retirement

- Plan retirement lifestyle

Goals:

- $1,000,000-2,000,000 invested

- Financial independence achieved

- Successfully built wealth after 40

🎥 BONUS

Want to see real people who built wealth starting after 40?

This video shows their exact strategies:

FINAL THOUGHTS: Starting Late Doesn’t Mean Finishing Last

Here’s what most people don’t understand about building wealth after 40:

They think it’s impossible.

“I’m 45 with nothing saved. I’ll never retire.”

So they give up before starting.

Continue bad habits. Don’t save. Ensure poverty in old age.

Here’s the truth:

Building wealth after 40 IS harder than starting at 25.

But “harder” doesn’t mean “impossible.”

It means:

- More aggressive savings (30-50% vs. 15%)

- More focused strategy (no wasted effort)

- More intense discipline (deadline approaching)

- More income required (career + side hustles)

But all of this is DOABLE.

After following this plan:

Year 1 (Age 40):

- Eliminated $20,000 debt

- Started investing $2,000/month

- Built $5,000 emergency fund

- “This is hard but possible”

Year 5 (Age 45):

- Debt-free

- $150,000 invested

- Side income: $800/month

- “Momentum building”

Year 10 (Age 50):

- $450,000 invested

- Saving 45% income

- Catch-up contributions maxed

- “Going to make it”

Year 15 (Age 55):

- $950,000 invested

- Multiple income streams

- Could retire early if wanted

- “Actually built wealth after 40”

Year 20 (Age 60):

- $1,600,000 invested

- Financial independence achieved

- Comfortable retirement secured

- Started at 40 with nothing, retiring wealthy

All from starting at 40 and executing aggressively.

The question isn’t “Can I build wealth after 40?”

The question is: “Will I do what it takes?”

Aggressive savings. Debt elimination. Income increase. Discipline. Consistency.

Do these for 15-25 years?

Then yes, you WILL build wealth after 40.

Others say it’s too late and give up.

You’ll start today and succeed.

That’s the difference between poor retirement and wealthy retirement.

Your wealth after 40 starts now.

Not tomorrow. Not next month. NOW.

Open retirement account. Set up automatic contribution. TODAY.

Then increase it monthly. For 20 years.

You WILL build wealth after 40.

Others doubted themselves.

You committed and executed.

See you at retirement. Wealthy.

INTERESTING TOPICS

Want to learn about what are index funds for your wealth after 40 investing?

Ready to understand the 50/30/20 budget rule for aggressive savings?

Need strategies for making money from home to boost income after 40?

Want more financial insights delivered to you? Subscribe to our newsletter

and get weekly articles with practical strategies to grow your wealth sent straight to your inbox.

Obs: Sign up for our newsletter and receive a free Finance For Beginner eBook.

Disclaimer: This article is for educational purposes only and should not be considered financial advice. Budgeting approaches should be tailored to individual circumstances, income levels, and financial goals. The examples provided are for illustrative purposes and may not reflect your specific situation. The 50/30/20 rule is a guideline and may need adjustment based on your cost of living, debt obligations, and personal priorities. Consider consulting with a financial advisor for personalized guidance on managing your finances and creating a budget that works for your unique situation.

—— End of Article ——